You spend years helping your children find their way. Then one day you realize they are grown and still leaning on your bank account!

This piece gives you the facts and figures that often surprise people in their fifties.

You learn:

• How each adult child can add $15,000 to $20,000 per year in additional costs to your household

• how that support shapes your pension choices

• ways to help them stand on their own two feet

• simple Irish tax points that matter

Why this is important for people over 50

Your fifties are usually the years when financial pressure decreases. The mortgage can be calmer, the income is more stable and children are usually launched. Then the rent goes up, the study takes longer than expected, or an adult child returns home.

You want to support them. You also want to protect your retirement timeline. When these interests collide, your savings usually take the hit. Even saving two or three years less can delay retirement more than most people expect.

What it really costs to keep children reading books

Typical support areas

Many of the people we support have adult children who are still ‘on the books’. From our experience, parents in Ireland regularly say:

• Rental and study costs

• Car insurance & use of a small car

• Health insurance

• High costs for food and entertainment!

Irish examples

A simple breakdown that many households will recognize:

• Rental subsidy: 500-800/month

• Car insurance: 200/month

• Health coverage: 100/month

• Food/Entertainment/General: 300/month

That amounts to €1,100 – €1,400 per month.

In a year, it’s $17,000 in net income to cover the potential costs of an adult child!

If we add that up over 4 years, we are talking about $60,000-$70,000 in income or assets needed per adult child!

That money supports your children or supports your own freedom.

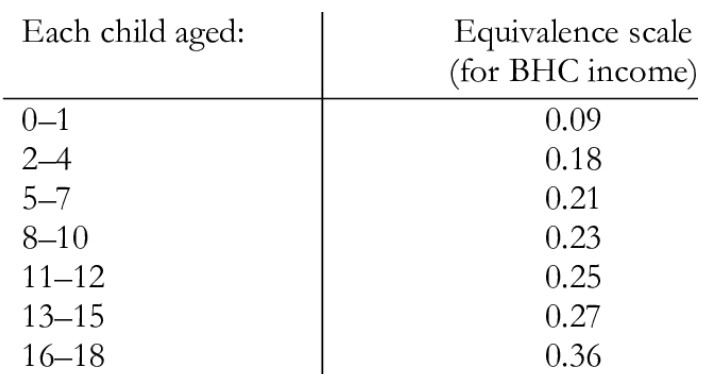

The McClements equivalence scale

The McClements Scale, drawn from British research but fully applicable to Ireland, helps us understand how household costs rise and fall as children grow, leave home or live in.

It turns everyone into “equal adults” and shows the true financial weight each person brings.

To turn this into practical numbers, consider a scenario:

Jane and Jack’s household expenses over time

The total costs of Jane (head of household) are € 50,000 per year

She marries Jack, who brings a lot of fun 😉 but also an extra factor of 0.42, or € 21k

The total to run their household now amounts to €71,000.

They then have 2 children, for this example.

As long as they are under 18 years old, the additional cost of each child varies from a factor of 0.09 to 0.36 (or from €3,600 per year as a baby, to €14,400 if they are 16 to 18 years old!!).

Jane and Jack notice that as the two children grow older, their household expenses steadily increase!

When it was just the two of them, the total household costs were €71,000.

That increases by a factor of 0.27 (from €50,000) per child when the children are 13-15 years old, for a total of €92,000 per year, or €7,700 per month.

As they mature and are STILL on the books, McClements suggests that the additional financial burden on the household

0.42 for the first child (€ 21,000 per year for Jane & Jack) and 0.36 for the 2nd child, or € 18,000 per year.

Although they are grown and on the books, McClements suggests that ‘these 2’ will cost c€40,000 a year!

I hope they appreciate you!

The McClements Scale makes one thing clear: when an adult child moves, your long-term financial capacity increases immediately and meaningfully.

How adult and child support is delaying retirement for some

Impact on pension contributions

The pressure on cash flow often leads to parents reducing their pension contributions for a year or two. Even short breaks can noticeably reduce your long-term fund.

Instead of sending $30,000 a year to support, educate or grow their two children, imagine Jane and Jack putting that into their pension and claiming the higher allowance! Net costs can drop to about $18,000 per year, rising to $150,000 in four years.

Over time, that difference can add quite a six-figure value to their retirement plans!

Reduced savings

Monthly support for children often replaces monthly savings. The more support you give, the slower your own plan will progress for many.

A simple example

One client supported two adult children during the final phase of their studies, for an amount of approximately 12,000 euros per year. When both children started working, they set a clear end date for support. Converting that money into pensions, to maximize tax credits, and cash reserves changed their financial picture within two years. They regained control and came closer to a real choice about work and retirement.

When it’s reasonable to take a step back

What other Irish parents do

Most Irish parents expect or hope to provide some help until their children are in full-time employment. After that, an agreed end date is usual. It prevents confusion and resentment on both sides. Setting clear expectations and timelines is a valuable endeavor. That said, everyone’s situation will of course be different, and some will be ready earlier than others etc.

A transition plan

• agree on an end date

• gradually phase out support

• help them prepare a simple budget

• stop paying surprise bills – let them sort it out!

• encourage them to take responsibility and awareness early

Helping children become financially independent

Starter budgets

Encourage your children to structure their own expenses. Important items include:

• rent

• food

• transportation

• savings

• nice money

Most people in their twenties fall into spending habits. A simple plan might help them find stability and self-control!

Simple Irish Tax Points

Parents can donate up to 3,000 euros per child each year under the small gift exemption, without affecting the child’s lifetime gift or inheritance tax threshold. If you want to provide greater help, take barriers into account.

Protect your own safety in the long term

Are you putting your pension at risk?

Support for children feels generous, and for every parent it’s something they will at least think about! But it often reduces your retirement funding or delays your investment plan. You can give money later. You can’t regain the lost years of compound growth.

Your own freedom number

Your own financial ‘number’ is the desired annual income and the lump sum required for this. Once you know that figure, you can assess how long you need to work and how much you can afford to help.

The turning point in cash flow

Once children leave the books, monthly cash flow often improves by around 15-20% of the total costs for the joint household!

The McClements scale supports this and shows that removing one adult reduces actual household costs in a meaningful way.

Conclusion

Most of us want to be financially independent when children leave home. We could get that freedom based on our own accumulated assets, or that plus a combination of taking kids off the books! When support for children decreases and your own pension and savings increase again.

A small change in the way you support can change your entire retirement timeline. Your next step is simple: check your own grades and agree on an end date with your children!?

If you want clarity about your own financial freedom and when you can choose a life with less pressure, please contact us.

You can also read or listen to our award-winning blog and podcast for (hopefully) fresh ideas, rooted in reality.

I hope this helps.

Paddy Delaney

#financial #freedom #kids #books