I need help with something this morning, if you’re willing to help me.

Let’s say there is an epic snowstorm in January that produces over two feet of snow.

Now let’s say you’re shoveling piles of snow from your driveway to your front yard, in a pointless task that feels like “five steps forward, four steps back.” Meanwhile, your children are pushing through the snow back into the driveway and beg you to use the snow blower so they can block the flying snow with their sleds, aka their “shields,” doubling your workload.

Do you consider this as:

a) Exceptionally cute, a moment of bonding between parents and children, and the exact reason why we have children.

b) Incredibly frustrating, annoying, useless and the reason why we reminisce about our lack of responsibilities when we were younger.

Go ahead. I promise I won’t get hurt…

We may say this every year, but I think this was the snowiest January we’ve had in a long time.

During that snowstorm on January 25, I couldn’t help but feel terrible for my colleagues who were hosting open houses for their “hot listings,” especially those who had strategically listed their properties with offer data on the Monday evening after the weekend open days.

Plan for the best, or plan for the worst? Now there is a strategy!

On the other hand, for every piece of bad luck there is also a corresponding piece of luck, right?

Colleagues of mine had a popular listing in the East End at the end of January, ultimately booking over 100 shows!

They had a listing date scheduled for Monday afternoon after the weekend, where they would presumably have two open houses, Saturday and Sunday, and a whole series of those 100 showings would take place.

But Friday evening they received an exceptional bully offer and ultimately sold the real estate company.

What happened next?

A huge snowstorm.

I have no doubt that the property would still have sold with multiple offers and for a great price if they had waited until Monday, but there would have been fewer showings, less interest, and fewer offers as a result of that snowstorm. School was canceled on Monday, so think of all those parents who were focused on their kids at home, who might not have offered on the house.

I saw quite a few impressive sales in January, but most of them were in the same market segment:

Ownership of single-family homes in family-oriented neighborhoods, between $1.4 million and $1.6 million.

Areas like Riverdale, The Pocket, Roncesvalles and Greenwood Park, if we’re more specific.

But my biggest takeaway from the month of January was that there was a shortage of quality inventory, as we complain about every year at this point.

On Monday, January 5, I got on the phone to try to find a home for my Leaside buyer clients.

They were looking for something “more” than your typical 30′ x 100′ new construction home, which costs between $2.8 million and $3.2 million. I had to find something for them on a plot of more than 10 meters, with more square footage, more features and finishes and a better backyard.

I called about eight brokers I know, and as is the case when you trade outside the market, I got a call from someone who had heard from someone that I was looking.

I took my clients to see this house, which was listed at $4,200,000, but it wasn’t right for us.

Would you believe it was sold privately to someone the next day? otherwise?

That product simply doesn’t exist right now, and it’s not something you can wait to see on MLS.

Regardless of what January’s TRREB stats look like in terms of prices, sales, new listings, and absorption rate, I’ll keep this up until I’m blue in the face:

There is currently a severe lack of quality inventory in the home ownership market.

So let me walk you through January’s TRREB numbers as I see them, and I promise to (try?) to be unbiased.

I say that of course because I opened today’s blog post by talking about a “lack of quality inventory” and being optimistic in some ways, and yet for those of you who have already seen the TRREB numbers, you’re going to argue, “the sky is falling.”

I’m glad to hear you about that, but first hear me out: one of my trusted colleagues just said, “It’s damn Januaryman. It was a month long goddamn blizzard. Do you want to evaluate the market? Wait until March.”

Fair point. And like I said, I’m glad to hear yours.

So let’s start with the average GTA home price:

“David, how @#%& are you going to pretend the sky isn’t falling! The median home price just fell below $1,000,000 for the first time since 2021!”

Yes, just as I said it would happen

Are January.

We have been on a downward trajectory since the fall and we are in the middle of winter.

Sorry, but I have to agree with my trusted colleague on this point and suggest that maybe, just maybe, January will go ahead.

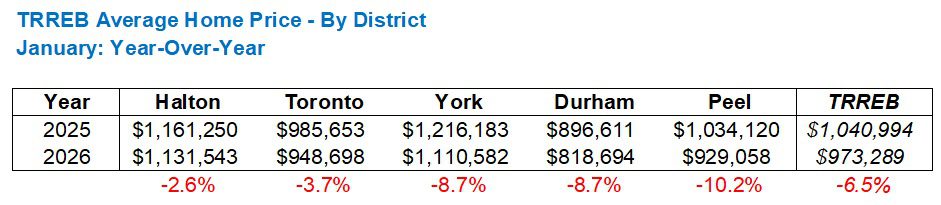

If we compare January 2026 with January 2025, we see a 6.5% reject in the average house price, which is significant.

But how is this broken down by geographic location

Like this:

Every average is made up of several or many smaller averages, and TRREB’s average home price is no different.

Peel Region has seen a whopping 10.2% drop in average house prices in January compared to January, while Halton is down just 2.6% and Toronto is down just 3.7% respectively.

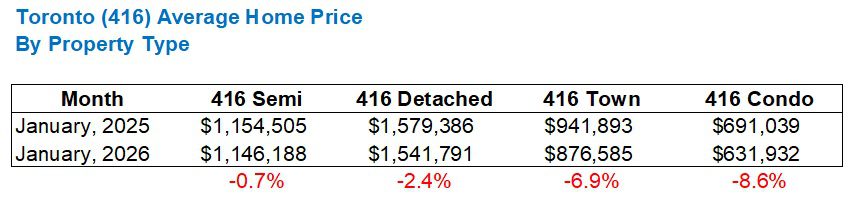

If we wanted to look deeper at the 416 (Toronto), I would break down the year-over-year price change by property type as follows:

This makes sense, right?

I mean, “What is a mansion?” would be a good question at this point. To be clear, this includes both detached townhouses And condominium townhouses, which makes absolutely no sense to me as I would prefer to include condo townhouses in ‘Condos’ and detached townhouses in a category with ‘Semi-detached’, but I digress.

Either way, seeing a 416 semi priced just 0.7% lower than last year makes perfect sense and is consistent with what I’m seeing now.

Again, at the risk of being too bullish, I would argue that some semi-detached houses in Riverdale, Leslieville, Roncesvalles, Greenwood Park, et al. have sold better in January 2026 than they did in January 2025, but if you don’t want to hear any bullish nonsense from me, let me solve this for you…

…WOW LOOK AT AN 8.6% DECREASE IN CONDO PRICES!

There! Now we both win.

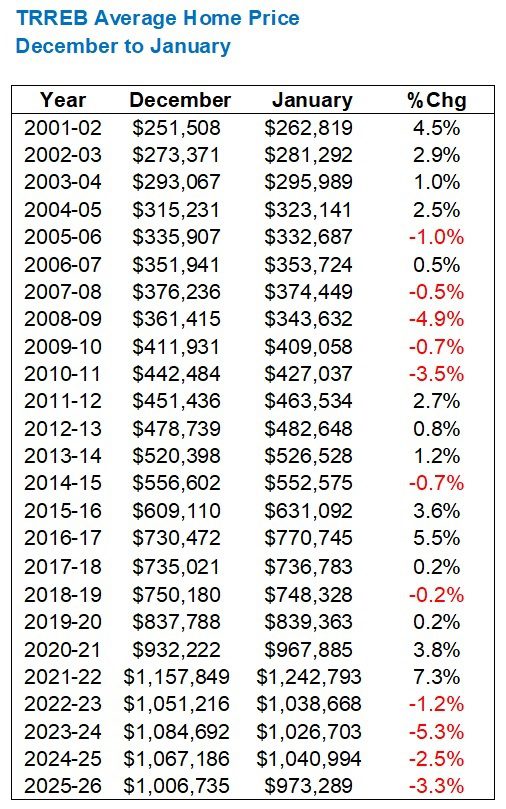

If we look at what ‘typically’ happens to the average house price from December to January, consider that between 2001-2002 and 2021-2022 we saw a increase in house prices in 14/21 years. Since then it’s all been red data…

This is the fourth year in a row that we have seen a decline between December and January, something we have not experienced since 2007-2010.

However, remember that the average house price increased in February compared to January all of these years, so it’s not like we’re seeing a bear market that’s going down every month.

There is no doubt about it: February, March and April prices will be higher. How a lot of the question is higher…

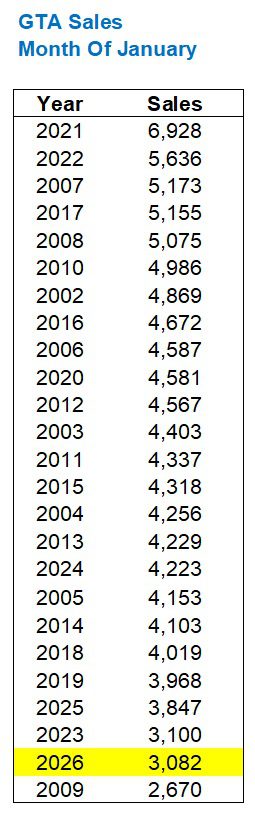

As for sales, the following graph surprises absolutely no one:

I told my team that we might see less than 3,000 sales.

That is how much I felt the market in every ounce of my being last month. There was simply “nothing” and yet when I get to the stats of the mentions, many of you will want to call this “nonsense”.

Remember, TRREB once published a “Re Listing” statistic. They did this for a very short time in 2023 and 2024, before shutting down and deleting the data they had published. From what I saw in January, an overwhelming number of “new listings” were reused listings from last year.

That said, there’s still no denying that sales were low.

Terribly low.

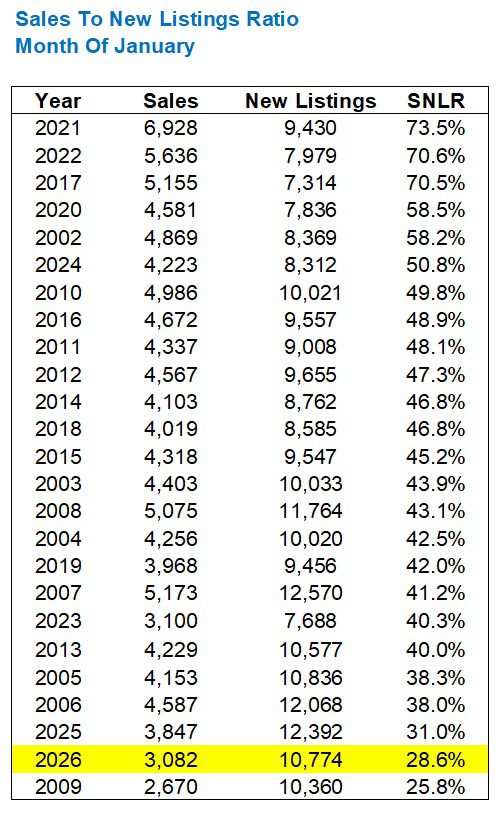

Sales fell from 3,697 in December to 3,082 in January, which is a decrease of 16.6%.

Only once since 2001 we have seen a decline this large or greater:

The crazy thing about selling from December to January is that you would think they should be rising, but have actually fallen in twelve of the previous twenty-four years.

Not only that, if you want to look more recently, sales dropped from December to January seven of the foregoing nine year

Again, I think this speaks to the absurd number of relistings we’ve seen in recent years, but before I go on that rant again, let’s take a look at the new listing numbers.

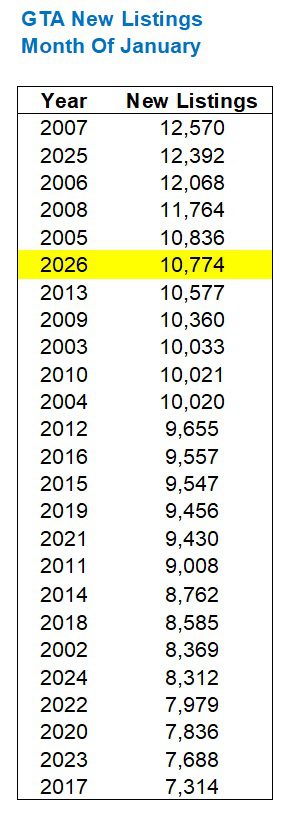

Last month we saw 10,774 new listings.

This was it down 13.1% as of January 2025; however, it still ranks sixth on the following list going back to 2002:

Hardly the “lack of inventory” I’m ranting about, right?

You’ll just have to trust me on the quality of that inventory, plus the fact that much of the inventory is made up of overpriced micro-apartments that no one wants.

Tell me you want a 3 bedroom, 2 bathroom semi-detached house in a family setting, and I will tell you that the options are limited and you will find yourself in multiple offers if you want to bid.

Anyway, I still need one figure on the relationship between sales and new listings, which was rotten last month.

These 3,082 sales, versus 10,774 new listings, resulted in an absorption rate of 28.6%.

This is the lowest we’ve seen in January since 2009, which happens to be the year that corresponds to the only January, where we saw fewer sales than last month’s 3,082:

Guys, maybe my memory is not what it used to be, but I don’t remember the January 2009 market.

Be that as it may, January’s absorption rate of 28.6% is slightly lower than the 31.0% recorded in January 2025.

Not only that, it was only two years ago, in 2024, that the January absorption rate was 50.8%. My, how things have changed!

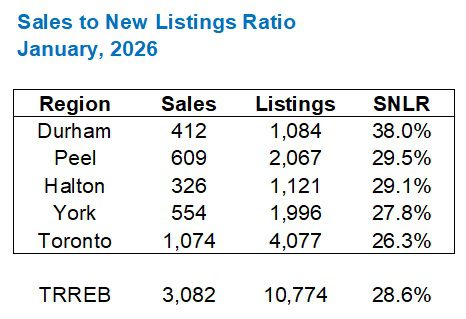

Here is an overview of the top five TRREB regions by absorption rate:

Who saw That coming?

Toronto at the bottom?

I suspect this is because Toronto has a much higher share of apartments, and the absorption rate in the 416-apartment market was 22.5% in January. Maybe this just moves the needle slightlybut enough that Toronto might not otherwise be at the bottom of the pack.

Okay, these are all the stats I wanted to share today.

Let me sum it up with three points:

1) The market is still in a downturn.

2) January was unusual, terrible and difficult to use as a benchmark.

3) Some parts of the market are truly “piping hot,” while others are warm, lukewarm, cool, or ice cold.

Now it’s your turn…

#January #TRREB #Stats #Freeze #Thaw #Toronto #Realty #Blog