Want more stories from the housing market of Lance Lambert’sLubIn your inbox?Subscribeto the resic clubnewsletter.

This week the Federal Reserve Bank of New York published her DiMACIOUS DOUNTIONAL DESIGN AND CREATMENT REPORT. It shows that, although still low, need crawls back to the housing market.

This is how the American preventments in the first quarter of 2025 relate to previous years:

Q1 2014: 144,500

Q1 2015: 111,820

Q1 2016: 96,680

Q1 2017: 90.460

Q1 2018: 76,360

Q1 2019: 71.040

Q1 2020: 74,720

Q1 2021: 11,400

Q1 2022: 24,220

Q1 2023: 35,640

Q1 2024: 44,180

Q1 2025: 61,660

When COVID-19 started Lockdowns, the federal government implemented a national executionoratorium to protect homeowners against the economic fall-out. These protection – including prohibition programs – were expanded several times. At the same time, a historical increase in housing demand pushed house prices to new highlights during the flourishing of Pandemic Housing, which increases the equity of homeowners and keep the shielding activity unusually low.

But in the past quarters, fortresses have returned steadily, closer to pre-Pandemic levels of 2019. That shielding rebound up the pace in the first quarter of 2025, after the Course of the moratorium on Prohibitions of housing credits supported by the US Department of Veteran Affairs.

The question to the fore: will the preventments of the home continue to rise due to the rest of 2025 and in 2026? Let’s take a closer look at the leading indicators.

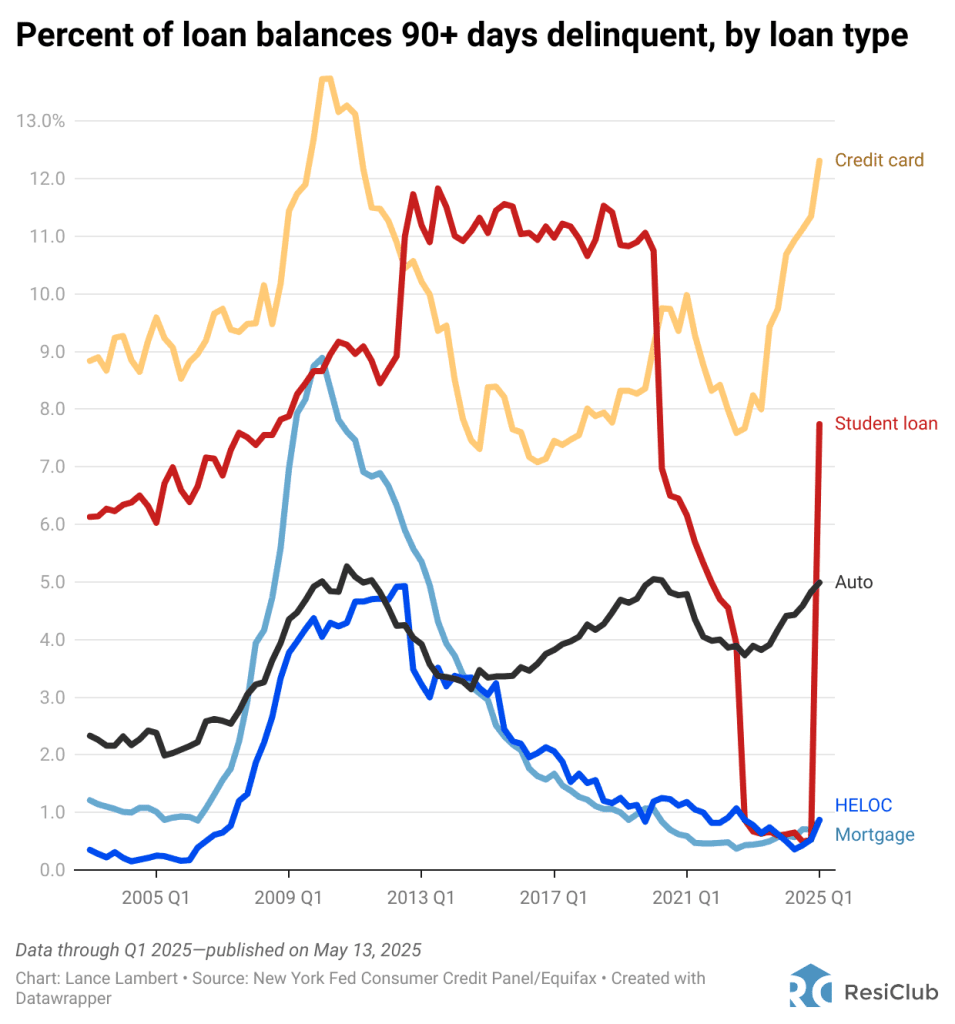

Before the reasons for American housing rise, the backs of more than 90 days usually increase. Although the credit card and automatic overdue delinquencies have risen from 90 days or more in the past quarters, arrears of 90-plus days on household mortgages remain far below pre-Pandemic 2019 levels.

This is how the recent share of household mortgage balance that is 90-plus days delinquent compares with previous years:

Q1 2014: 3.72%

Q1 2015: 2.95%

Q1 2016: 2.08%

Q1 2017: 1.67%

Q1 2018: 1.22%

Q1 2019: 1.00%

Q1 2020: 1.06%

Q1 2021: 0.59%

Q1 2022: 0.47%

Q1 2023: 0.44%

Q1 2024: 0.60%

Q1 2025: 0.86%

In the field of delinquency, the most striking development this quarter is that the loan of student loans has risen to a five -year high at the beginning of 2025. While the leap was expected after years of artificially low student loans for student loans, FED researchers warned serious consequences for back students.

According to the New York FedSuperprime US borrowers – who wear credit scores above 760 – who wear unpaid balances of student loans, it is expected that their credit scores will fall by an average of 171 points this spring. That is because delinquencies for student loans, which had not been reported to credit agencies since the start of the pandemic, are now being reported again. This sudden credit hit could temporarily push some borrowers out of the housing market in 2025 and 2026.

The treasury has also resumed the collection tactics on student loans, including wage determination and tax payments, the raising of questions about potential overflow to other areas of consumer credit.

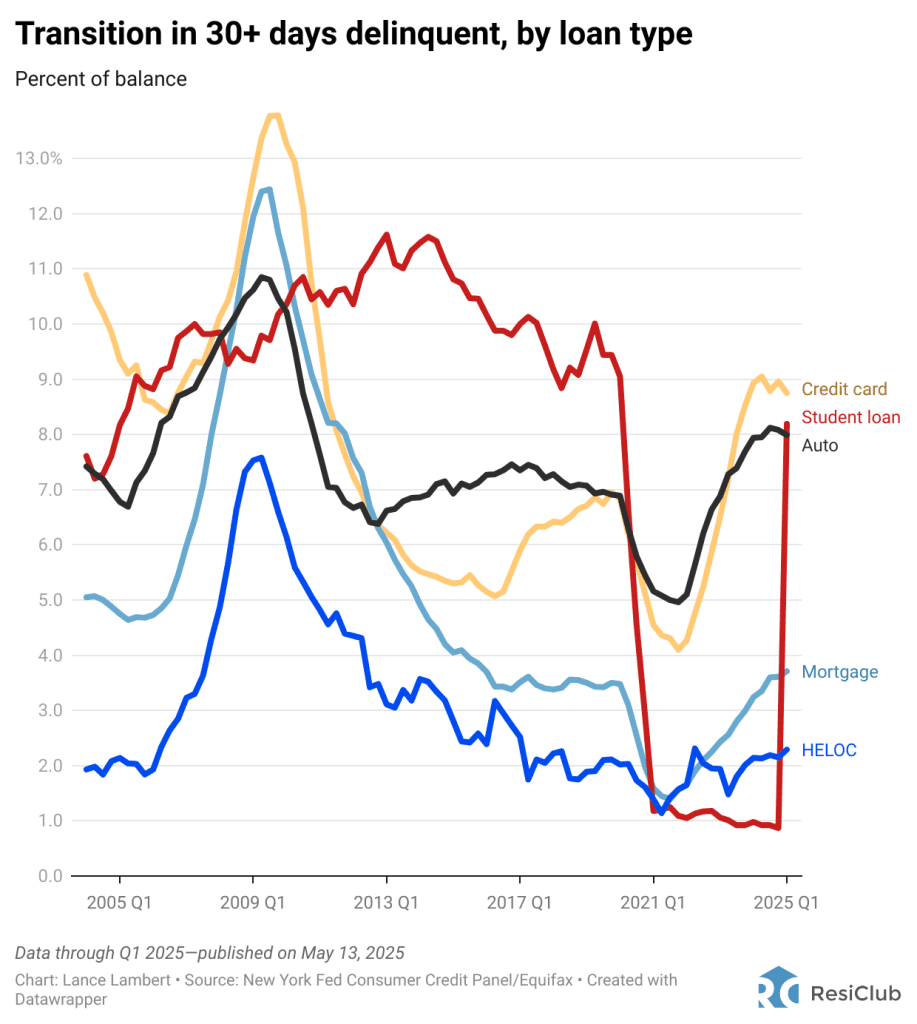

And before 90-plus day delinquencies usually increase, 30 delinquencies usually rise first. Indeed, more than 30 delinquencies of the day have returned to the levels of Pre-Pandemisch 2019.

This is how the part of household mortgages that turn into more than 30 days compares delinquent with historical data.

Q1 2014: 4.92%

Q1 2015: 4.05%

Q1 2016: 3.70%

Q1 2017: 3.51%

Q1 2018: 3.38%

Q1 2019: 3.50%

Q1 2020: 3.48%

Q1 2021: 1.59%

Q1 2022: 1.66%

Q1 2023: 2.43%

Q1 2024: 3.24%

Q1 2025: 3.71%

Big Picture: While the impediments of the American housing remain low and under pre-Pandemic 2019 levels, the 30-plus days delinquency data suggest that preventments can gradually the pre-Pandemic 2019 by the end of 2025 in the vicinity of pre-Pandemisch 2019.

#Housing #market #shift #Obesolations #crawl