Financial planning and investing can become complex. That’s why communities like WCI exist: to demystify the choices and pitfalls doctors face at every stage. It is reasonable to assume that more complexity justifies a higher price for expertise. But does that mean costs should rise as your assets grow, even if your complexity level remains the same?

Most WCI readers are familiar with the industry standard compensation model: Assets Under Management (AUM) compensation. Here, financial professionals continually charge a percentage of your portfolio. This structure means your costs can increase over time as your savings and the market grow.

Suppose a disciplined doctor in his early 40s has amassed $1 million in investable assets (a plausible milestone for many). If they continue to save aggressively and take advantage of even modest market growth, it wouldn’t be unreasonable for that portfolio to reach $3 million or more by age 50.

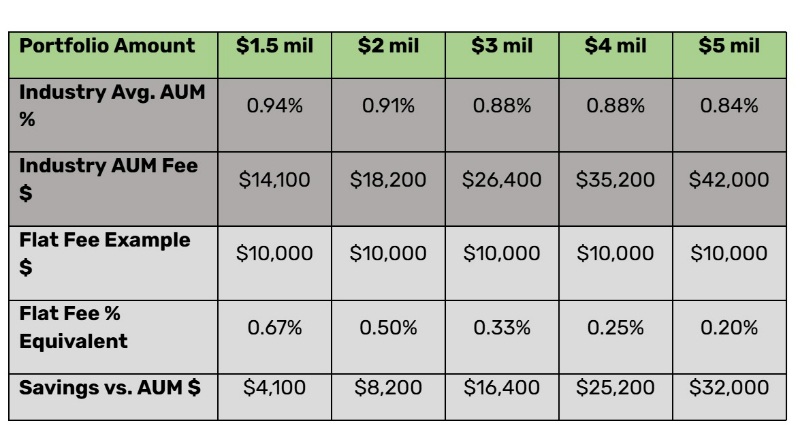

Under a typical industry blended AUM rate, annual advisory fees look like this: via AdviceHQ:

Data on average industry advisory costs, sourced from AdvisoryHQ. Refunds and returns are for illustrative purposes only; actual consultant costs and results will vary.

That’s more than double the annual cost, even if nothing else about your financial life has changed.

But there is another way. It is becoming increasingly known among informed investors, although still rare in the sector: the flat-fee model.

Only 8% of advisors operate without any AUM-based fees, making fixed-fee firms the exception and not the rule. A flat-fee structure charges a fixed, transparent dollar amount for services, regardless of portfolio size. Many flat rate companies also offer the option of standing orders, single project orders or hourly orders depending on your needs.

To see the contrast, we extrapolate from the earlier example:

Data on average industry advisory costs sourced from AdvisoryHQ. Refunds and returns are for illustrative purposes only; actual consultant costs and results will vary.

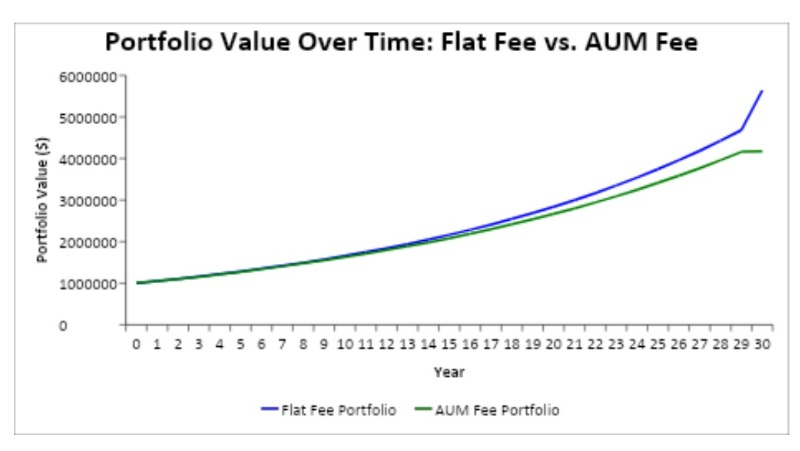

With a fixed fee structure, your compensation is predictable and does not function as a wealth tax simply because you have saved more or the market has risen. The difference becomes even more striking when you look at the compounding effect of investing a larger portion of your wealth.

For simplicity, the following example assumes no additional contributions, but a one-time investment that grows over time. The result: a portfolio that grows more than $580,000 in size under the flat-fee model compared to the industry average AUM fee.

Assumptions: $1 million starting balance, 6% annual return, $10,000 annual fixed fee, industry average AUM cost per AdvisoryHQ. The costs are deducted annually. No additional contributions or withdrawals. Educational illustration only, not financial advice. Actual costs and results may vary.

But costs and prices are only one aspect of the story. Most physicians have seen how incentives shape behavior in healthcare. The same is true in the financial world: the way your advisor is paid will inevitably influence his recommendations, even if everyone means well.

How incentives shape advice

Most advisors, whether fiduciary CFPs or fee-only RIAs, sincerely want to do right by their clients, and many do. But the reward structure is always important. Even with the best intentions, AUM incentives can silently (even unknowingly) influence recommendations.

Consider this scenario: you inherit a significant amount of money and want to buy a house in the mountains, both as a family getaway and as a rental property. Naturally, you’re wondering, “How much should I put aside? Should I use some of my portfolio, or should I leave the investments untouched and take out a larger mortgage?” On paper, this is just a matter of financial planning. But for an advisor who gets paid for assets under management, every dollar out of the portfolio means a direct reduction in ongoing costs. Even if the advisor fully discloses this and tries to remain objective, there is subtle friction. It can present itself as a gentle nudge to leave more invested, a suggestion to make a smaller down payment, or a focus on the opportunity cost of taking money out of the market.

This same AUM-driven tension can influence advice around:

- Using investment assets for a practice buy-in or business opportunity.

- Pay off student loans or wipe out a mortgage with portfolio withdrawals.

- Purchase of a second home, holiday property or rental property.

- Building a larger cash reserve for career flexibility, self-insurance or peace of mind.

The good advisors make these conflicts public and clearly explain the options and consequences. But disclosure alone cannot eliminate the underlying structural problem. This isn’t about bad actors. It is about the way in which incentives shape advice, often beneath the surface.

When you consider both the composite costs of AUM fees and the subtle ways they can shape your advisor’s recommendations, you have to wonder why the industry hasn’t changed. The reason AUM still dominates doesn’t have to do with logic or customer outcomes. It comes down to the business realities and incentives that keep the model firmly in place.

More information here:

What would your ideal financial advisory firm look like?

Why fixed fees are rare and assets under management continue to exist

Allow me to digress for a moment. Today, low-cost, broadly diversified investing is common sense, but we almost forget how radical this was decades after Mac McQuown. launched the first (non-retail) index fund in 1971. Indexing didn’t spread like wildfire; it spread like molasses. The financial sector is slow to change, especially when the status quo is profitable.

In the 1990s, you could find a fiduciary financial advisor, but it wasn’t easy. Almost everything was commission-driven and transactional: upfront investment funds, commissions and insurance products. The conflicts were obvious, but it took time (and many disappointed investors) before consumers started demanding something better.

When real financial planning finally came into the spotlight, the AUM model was an advancement. It brought advisor incentives more closely in line with clients. It provided ongoing service. And it was more extensive. But as technology advanced and companies were able to serve more customers at scale, the AUM fee structure did not change. It became increasingly entrenched, more lucrative and harder to pivot away from.

Today, the vast majority of the asset management industry is built around AUM. Major national asset management companies rely on this model to fund advisor salaries and parent company profits. In independent businesses, it guarantees staffing, operations and owner compensation. Moving to a flat-fee model isn’t just a price change; it is a complete reset of the business model.

If you need proof that AUM is the golden goose of the industry, just look at private equity. PE firms are not acquiring asset management practices at a record pace because of their transparency or customer-oriented values. They buy revenue streams that automatically scale and grow as markets rise. There is little reason to change course if the model works.

Changes in financial services have never come from the top down. It took decades for indexing to become mainstream, and fixed cost planning will follow the same path. The catalyst is always the same: informed investors asking better questions, comparing their options and demanding something better.

More information here:

How to get real financial advice when you need it

Delegator, validator or do-it-yourselfer? Take this quiz to find out what you are

Second Opinions are important, especially when it comes to AUM costs

Every doctor knows that when the stakes are high, a second opinion is not only smart; it is standard practice. That same habit of skepticism is just as valuable when it comes to evaluating financial advice.

If you’re already working with an advisor or are considering hiring one, don’t assume that the industry’s standard model is automatically the best fit for you. Ask the questions that matter:

- How exactly do I pay for advice? Will my fee grow as my assets grow, even if my complexity remains the same?

- What services do I actually receive for what I pay? Is it comprehensive planning or just investment management?

- If I make big decisions in my life (pay off a loan, buy a practice, buy a second home), will my advisor’s compensation change?

- Do I need ongoing services? Can I get a schedule per hour or per project? How are these costs structured and what is included?

- Can I compare a fixed amount to what I would pay under an AUM model? Are there situations in which a fixed amount can be higher?

- If my needs or circumstances change, is the model flexible or am I locked into a single benefit plan?

Lump sum planning isn’t for everyone, but clarity and coordination should be non-negotiable. In a world where fees are quietly constructed and business models shape advice, it’s worth asking what industry practice has become.

If you want to compare advisor models, organizations like I’m dying you can search for financial planners based on a fixed amount, per hour or on a project basis.

The best results come from an informed, proactive participant. Providing a second opinion on the AUM model may not lead to changes in the industry, but it will ensure that you get the right advice, for the right reasons, at the right price.

[Founder’s Note: It’s important to recognize that any time money changes hands, there is a conflict of interest. While an AUM model has its conflicts, so does a flat fee model. For instance, an AUM model incentivizes an investment manager to get higher returns. The flat fee model does not. That said, I still prefer the flat fee model simply because most using an AUM model do not adequately adjust the percentage for the wealthiest clients. (The clients usually don’t do the math to determine the fee either.) Most AUM-charging advisors think they’re doing you a favor when the second million fee decreases from 1% to 0.9%. It would be much fairer if it decreased to 0.25%.]

What do you think? If you have a financial advisor, do you pay an AUM fee or a flat fee? Does one save you money over the other?

This article is for educational purposes only and does not constitute individualized financial, tax or investment advice.

#FlatFee #Scheduling #Physicians #AUM #Model #Deserves #Opinion #White #coat #investor