From January to December 2022, the Vanguard Balanced ETF portfolio (VBal), which has a 60/40 mix, lost 15.04%, almost as much as the decrease of 16.88%posted by the 100%-Stocks VANGUARD EQUIDITY ETF Portfolio (VEQT). The problem was not the shares; Investors must expect volatility with them. They were the bonds.

As the interest rates enriched to combat inflation, the bond component of Vbal was hit hard. The higher than average intervening duration (a measure of speed sensitivity) meant that prices fell sharper than the bond companies could be of a shorter term. This caught many conservative investors overwhelmed, in particular those who believed that fixed income in a recession would offer ballast.

In response, many portfolio strategists started to present a new model: the 40/30/30. These are 40% shares, 30% bonds and 30% alternatives.

Although institutions and advisers have access to advanced private alternatives to make this work, the question is whether Canadian retail investors can replicate a similar structure with the help of listed ETFs. Here is my opinion, and some suggested ETFs to obtain exposure to the alternative space.

What is the 40/30/30 portfolio?

The 40/30/30 portfolio is a conceptual framework that changes the traditional balanced portfolio by making room for alternative assets. The idea is to introduce a third asset class that behaves differently than the other two.

In periods and 2022, when both shares and bonds fell together due to rising inflation and interest rates, traditional diversification strategies failed. The extra alternative sleeve is designed to maintain capital in times when the other two pillars of a portfolio move together.

It is not a one-size-fits-all recipe. The 30% allocated to alternatives can vary greatly, depending on the preferences of the portfolio manager. In most institutional and advisor-guided implementations, that can be part:

- Hedge fund -like strategies Such as long-term equity, managed futures, long volatility and market-neutral approaches that depend on quantitative models and exposure to Multi-ASET to generate absolute efficiency.

- Hard assets or digital stores of value Such as gold, raw materials or cryptocurrencies such as Bitcoin, usually used as static allocations to compensate for traditional financial assets volatility.

- Private market investments Such as private equity, private credit and direct property property, which in the long term offer return potential in exchange for liquidity risks and limited price transparency.

Moneysense’s ETF Screener Tool

Does the 40/30/30 portfolio work?

It is difficult to draw strong conclusions, because two factors limit the usefulness of most data used to support the statement of 40/30/30.

Article continues advertisement

X

The first is surviving bias. It is easy to look back and identify strategies that resulted in low correlation and solid returns, but that is afterwards. Investors did not necessarily have access to these funds or convictions when it mattered the most. The danger is to pick cherry success stories that were not generally known or available at that time.

Secondly, the results are highly dependent on the time period. The performance of each diversified strategy can vary meaningfully, depending on the start and end dates. A few good or bad years in alternatives can drastically skew the overall return and the risk profile of a portfolio.

That said, there is a relatively robust benchmark with more than two decades of data that helps to assess the viability of the concept: the MLM index. This benchmark follows a systematic trend-following strategy on 11 raw materials, six currencies and five global Borgfutures markets. It weighs each category based on historical volatility and individual contracts in the same weight within each basket. Although it is not a perfect proxy for all alternatives, it offers rare long-term, transparent and rules-based data in a room that is often lacking.

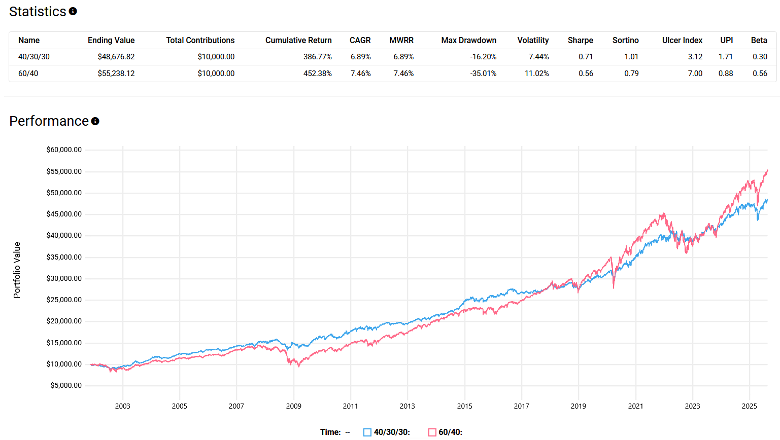

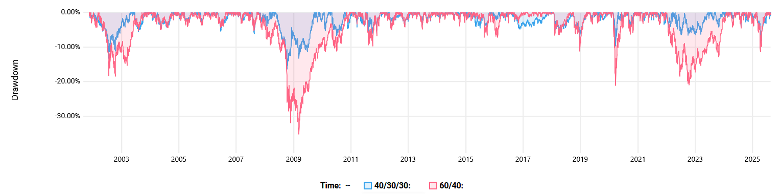

With the help of data from 12 November 2001 to 19 August 2025, a 40/30/30 portfolio under performance built with the S&P 500, Bloomberg US Aggregate Bond Index and KFA MLM index (rebalanced three -monthly) A traditional 60/40 mix on the total return (Cagrend) with a 6.89% compoundd. However, it exceeded considerably on a risk-corrected basis, with a Sharpe ratio of 0.71 versus 0.56.

What is even more important, the advantage of the diversification appeared when it mattered. The 40/30/30 portfolio showed better downward protection during important stress events, such as the bursting of the DOT-Com Bubble, the financial crisis of 2008, the COVID-19 crash in 2020 and the Berenmarkt of 2022.

Investors have access to the KFA MLM index via a US-listed ETF: the Kraneshares Mount Lucas Managed Futures Index Strategy ETF (KMLM). It immediately follows the benchmark and offers exposure to trend-following futures strategies in raw materials, currencies and fixed-income values.

The catch? Since KMLM is noted, Canadians are confronted with a few obstacles: currency conconer version, a high management ratio of 0.90% and a 15% foreign withholding tax on benefits unless it is held in a registered pension savings plan (RRSP).

#build #portfolio #ETFs #Moneysense