- Current bankruptcy rates are in line with what is considered normal

- The high equity in the home ensures that most homeowners remain in a strong financial position

- None of the data points to a major wave of distressed sales that will crash the market

The number of bankruptcy filings has increased by 32%, but that does not mean the market is in trouble

When you really peel back the layers, what everyone is really concerned about is that we’re heading for a repeat of what happened in 2008. At the time, riskier lending practices and an oversupply of homes for sale caused a decline in home prices, leading to a significant increase in foreclosures. Many people felt the impact. But this is not the same situation.

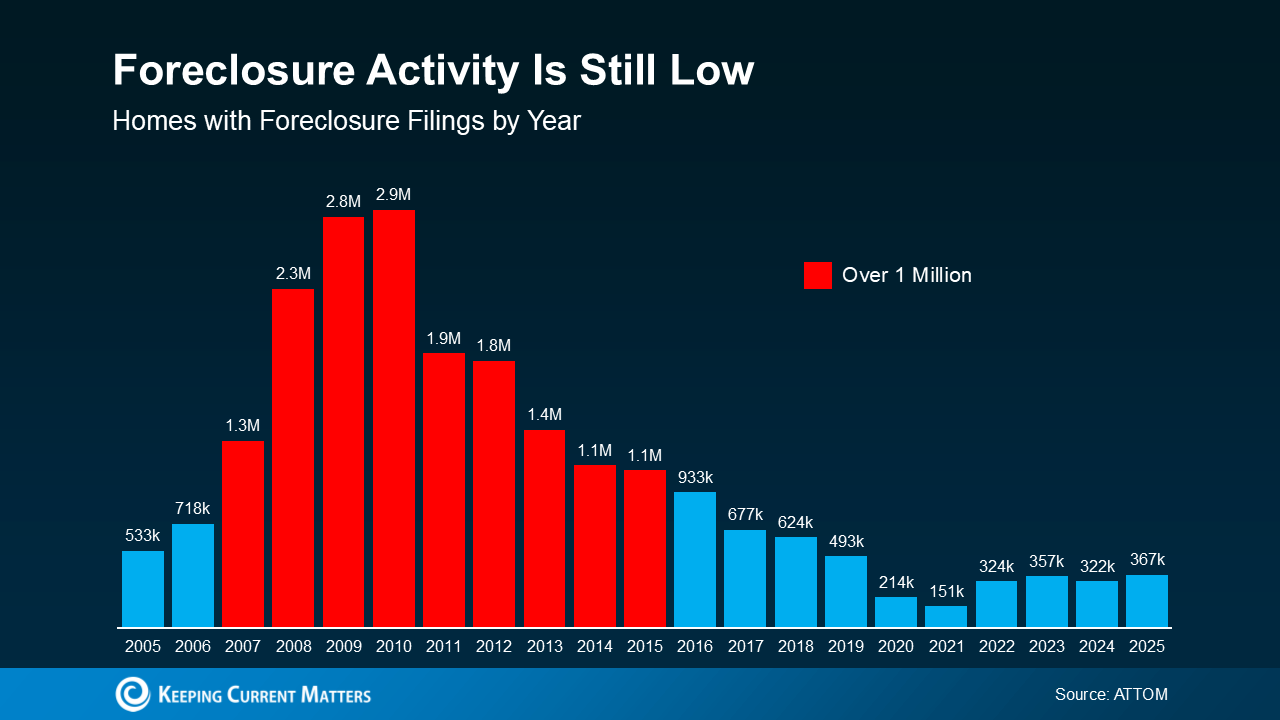

Yes, ATTOM data shows The number of bankruptcy filings has increased by 32% year-on-year. And that increase will sound dramatic. But context matters, and that doesn’t mean we’re headed for another crash. And the numbers prove it. Look where we were during the last crash (the red in the graph below). And where we are now (the blue):

Even with the upswing of late, we are nowhere near crash levels – far from it. This is not a return to crisis levels. What it is is a return to normal.

The chart below shows bankruptcy filings going all the way back to early 2005. The lead-up to and aftermath of the crash are shown in red. These are the years in which the number of bankruptcy filings exceeded the 1 million mark each year.

Now look at the right side and scan back to the period 2017-2019 (the last truly normal years for housing). You’ll see that we’re actually just starting to fall back in line with what’s typical for the market, even with the rise lately:

Rob Barber, CEO of ATTOM, explains the good:

Rob Barber, CEO of ATTOM, explains the good:

“Foreclosure activity increased in 2025 due to continued normalization of the housing market after several years of historically low levels . . . While the number of declarations, starts and seizures all increased compared to 2024, Foreclosure activity remains well below pre-pandemic norms and only a fraction of what we saw during the last housing crisis . . . The current rebound is driven more by market recalibration than widespread homeowner distress, with strong equity positions and more disciplined lending continuing to limit risk.”

The word ‘normalization’ in that quote is extra important. While economic and financial pressures are putting pressure on some homeowners, this is not a tidal wave of distressed homes. Whatever the headlines would have you believe, this is not a large-scale crisis.

Today’s increase is not a sign of trouble. It’s a return to normal.

Why this isn’t a repeat of 2008

Even though the latest housing crisis still shapes how many people interpret today’s news, the reality is that this is a different market:

- Credit standards are stricter

- Borrowers are better qualified

- And homeowners have much more equity

And that equity piece is especially important. House prices have risen significantly over the past five years. For many people, their home is worth much more than they paid for it. This means that most homeowners have a strong financial cushion to fall back on if necessary.

In short, if someone is faced with hardship today, he or she often has the option to sell, and perhaps even walk away with money in their pocket, rather than go through foreclosure. That’s a stark contrast from 2008, when many homeowners had more debt than their home was worth.

In short

Foreclosure activity, while increasing, is still well within normal limits – and nowhere near the danger zones of the past. But the headlines do more to scare than to clarify. And that’s exactly why it’s so important to have a reliable real estate expert you can rely on.

If you hear something in the news or see something on social media about housing that concerns you, contact a local real estate agent. An expert has the context needed to explain what is really happening and how it will affect you (if at all).

#rising #headlines #foreclosures #arent #red #flag #todays #housing #market