January 17, 2026

An often misunderstood aspect of mutual fund investing is net asset value (NAV).

There is a belief that ‘if funds have a lower net asset value, it is cheaper.’ There are also people who hesitate to invest in a fund because the intrinsic value is ‘a bit too high’. Then there is panic relief due to sudden drops in the net asset value of funds during times of volatile markets.

It’s ironic that NAV has little impact on the success or failure of your mutual fund investment. To truly understand NAV, one must go beyond definitions and look at what NAV represents in practice – and what it does not.

NAV is a result, not a starting point

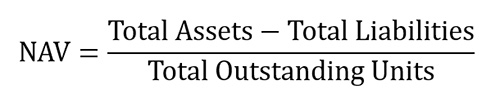

NAV reflects the per unit value of a mutual fund portfolio, net of fees. It is calculated at the end of each trading day based on the closing prices of the securities held by the fund.

The formula is simple:

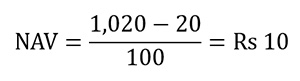

Suppose a mutual fund holds shares and cash worth Rs 1,020 crore. The cost and liabilities are Rs 20 crore. If the fund has issued 100 crore units, the NAV is:

This calculation highlights an important truth: NAV is an accounting outcome and not a price that, like stocks, is determined by supply and demand. Investors trade at the NAV, but have no influence on it.

Why a high NAV is not a sign of duration

One of the most persistent myths when investing in mutual funds is that funds with lower net asset values offer more upside potential. This belief largely stems from the way stocks are perceived, but the comparison is misplaced.

Consider two equity funds with identical portfolios and performance:

- Fund A was launched in 2004 with an initial net asset value of Rs 10

- Fund B was launched in 2019 with an initial net asset value of Rs 100

If both funds produce an annual return of 12%, the net asset value of fund A will obviously be much higher today because it has been built up over a longer period of time. This does not make fund A ‘expensive’ or fund B ‘cheap’. Both investors achieve the same percentage return on their invested capital.

How NAV moves on a daily basis

NAV changes every day and these movements are often misinterpreted. In reality, NAV fluctuations are caused by three key factors.

- Market value of underlying securities

When stock or bond prices in the fund’s portfolio increase, the fund’s total assets increase, causing its net asset value to increase. Likewise, market corrections reduce NAV. If a fund’s equity portfolio rises by 1% in a day and costs remain unchanged, the net asset value will also rise by about 1%. - Costs and fees

Investment fund costs are not deducted in one go each year. They are adjusted daily.For example, if a fund has an expense ratio of 1.5% per year:

This small daily deduction quietly reduces NAV over time. Therefore, expense ratios have a meaningful impact on returns in the longer term.

- Dividends and distributions

When a fund pays a dividend, the NAV decreases to the extent of the payout.

If a fund with a NAV of Rs 60 declares a dividend of Rs 4 per unit, the NAV will fall to around Rs 56 after the payout. This fall is often mistaken as a loss even though the investor has received Rs 4 in cash.

NAV and SIPs: Where Volatility Helps You

For SIP investors, NAV volatility is not something to fear; it is something to embrace.

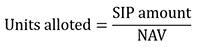

The number of units you receive in an SIP depends on the net asset value on the investment date:

If you invest Rs 10,000 monthly:

- At NAV Rs 50 → 200 units

- At NAV Rs 40 → 250 units

When the markets correct and the net asset value falls, SIP investors accumulate more units. Over time, this averaging effect improves return potential when markets recover. This is why experienced investors focus more on staying invested than on short-term NAV movements.

NAV during market corrections: a behavioral test

Sharp declines in NAV often lead to emotional decisions. Investors see the value of their portfolio falling and assume there is something fundamentally wrong with the fund.

However, NAV reflects current market prices, not long-term intrinsic value. A decline in net asset value during a broader market correction does not automatically mean the fund has failed. In many cases, it simply reflects temporary market sentiment.

Investors who redeem based solely on declining intrinsic value often lock in losses, while those who remain invested benefit from an eventual recovery.

When NAV really matters

Although the NAV should not be a guideline for fund selection, it does play a role in certain aspects of investing.

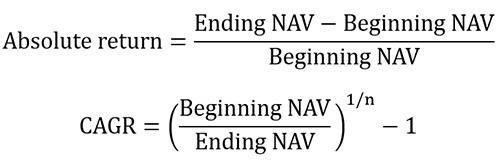

- Calculate returns

All mutual fund returns (absolute, CAGR or continuous) are derived from NAV changes. - Taxation on repayment

Capital gains tax is calculated based on the purchase NAV and the redemption NAV. The difference determines your taxable profit.

- Exit Loading

Exit fees, if applicable, will be charged on the redemption value calculated based on NAV.

What investors should focus on instead of NAV

Instead of asking whether a fund’s net asset value is high or low, investors should ask themselves:

- How consistent has the fund been through market cycles?

- Does the portfolio match current economic conditions?

- How has the fund dealt with downside volatility?

- Do the returns justify the expense ratio?

The bottom line

NAV is an essential metric, but it is often given more importance than it deserves. It tells you what a fund is worth today, not whether it is a good or bad investment.

A high intrinsic value does not limit future returns, and a low intrinsic value does not guarantee growth. What really matters is the quality of the underlying portfolio, the discipline of the fund manager and the ability of the investor to stay invested through market cycles.

When investing in mutual funds, the NAV is a mirror that reflects value. It is not a compass that guides the return.

Invest wisely.

Have fun investing.

Disclaimer: This article is for information purposes only and does not constitute any investment advice or recommendation to buy/hold/sell any fund. The returns mentioned herein are in no way a guarantee or promise of future returns. As an investor, you must choose the right fund to achieve your financial goals. If you are unsure about your risk tolerance, please consult your investment advisor/adviser. Investments in mutual funds are subject to market risks; read all fund-related documents carefully. Registration granted by SEBI, registration as RA and IA with Exchange and certification by NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

Mitali Dhoke has an MBA in Finance and a Masters Degree in Commerce (M.Com). He is Sr. Research Analyst at PersonalFN and has almost five years of experience in financial services. At PersonalFN, Mitali focuses mainly on research into investment funds and is recognized as an NFO specialist (New Fund Offer).

#NAV #mutual #funds #Opinions #Equitymaster #news