You don’t have to look so hard for bad news these days.

Even when the stock market and economy are booming, it’s easy to find negative numbers at any time.

Yes, for example, the stock market is at an all-time high, but this only helps the rich get richer. The top 10% own 87% of the stock market, while the top 1% own half of all stocks. Meanwhile, the bottom 50% own just 1% of the stock market in America.

Find out how easy it was to turn good news into bad news.

You can do the same with the housing market.

Certainly, home values are at record highs and the bottom 90% own almost 60% of the housing stock in this country. But what about all the people who can’t buy a house because prices and mortgage rates are so high?

Good news and bad news are often in the eye of the beholder. These things are rarely black and white, but rather gray.

There’s plenty of negativity out there these days, so let’s look at two positive developments in wealth building that occurred in the 1920s.

The Wall Street Journal has published a new story showing that while the rich are getting richer, more people are now joining in:

Some statistics from the article:

Of Americans with incomes between $30,000 and $80,000, 54% now have taxable investment accounts. Half of these investors entered the market in the last five years.

And nearly 40% of investors new to the market as of January 2020 plan to hold their investments for at least a decade for long-term goals, including retirement.

This is wonderful news!

Just look at the massive increase in the market value of stocks owned by the bottom 50% this decade:

Yes, it’s still a much smaller share than that in the top 10% or top 1%, but the improvement here is worth celebrating.

Robinhood has received a lot of criticism over the years for gamifying investing, but the company has also done a great job of getting new investors to sign up for a brokerage account.

Here’s what Steve Quirk had to say during one corporate event last year:

Half the people at Robinhood, 24 million customers, this is their first time, brokerage. We get to follow their investment path and provide everything they need as they continue to invest.

It’s estimated that nearly half of Robinhood’s users (12 million people) are opening their first investment account with the company.

This also happens at places like JP Morgan Chase:

In May, those with incomes below the median accounted for about a third of Chase customers transferring money to investment accounts, compared to a monthly average of about 20% from 2010 to 2015.

Another story from The Wall Street Journal looks at how high home prices affect the stock market:

Here’s the bad news:

The homeownership rate among Gen Z — people born between 1997 and 2012 — is just 16%, data from the National Association of Realtors shows. Meanwhile, the share of starters on the housing market is at a historic low. All told, this is a headache for homebuilders and those looking to sell their homes.

The monthly mortgage payment for an average $400,000 home is about $2,170, based on current rates and assuming the buyer has a down payment of $60,000, or 15%. This is approximately 36% of the after-tax salary of someone with an average household income.

And here’s the positive unintended consequence of an overpriced housing market:

A report from JPMorgan Chase shows that 37% of 25-year-olds were using investment accounts in 2024, up from 6% of the age group in 2015. A sixfold increase in the number of young people investing in the stock market over the past decade signals a shift in the way they think about building wealth.

Young people take the money they would save for a down payment, closing costs, moving expenses, etc. and put it into the stock market.

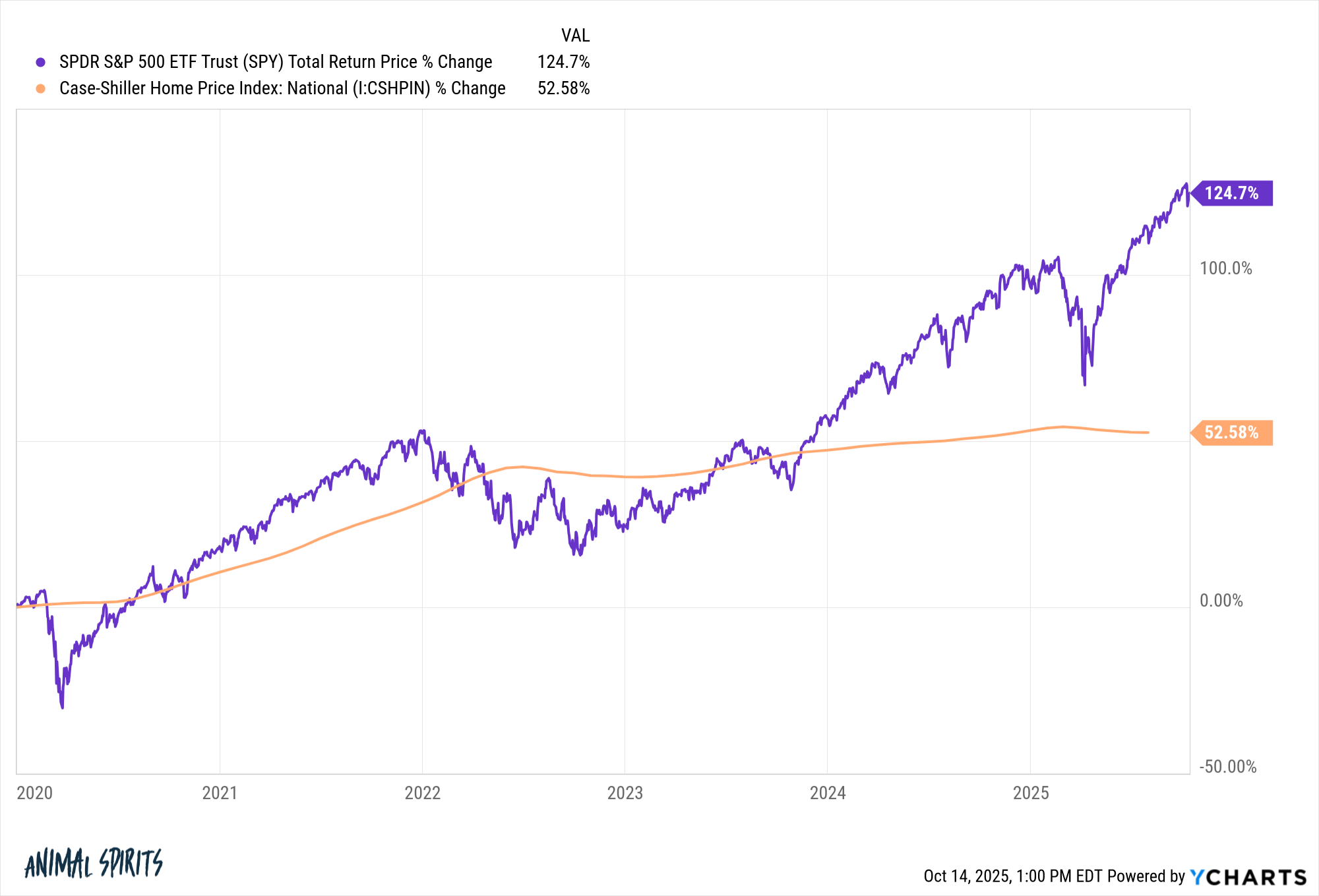

Even with the huge gains in the housing market earlier this decade, the stock market has more than doubled real estate returns.1 in the 2020s:

These young people will be much better off financially by investing in the stock market and renting, rather than tying up their money in an illiquid home.

Of course, you don’t just buy a house for investment purposes. For most people, there is a psychological component that trumps the return calculations.

I sympathize with the people who cannot afford a house in the current market. It doesn’t seem fair.

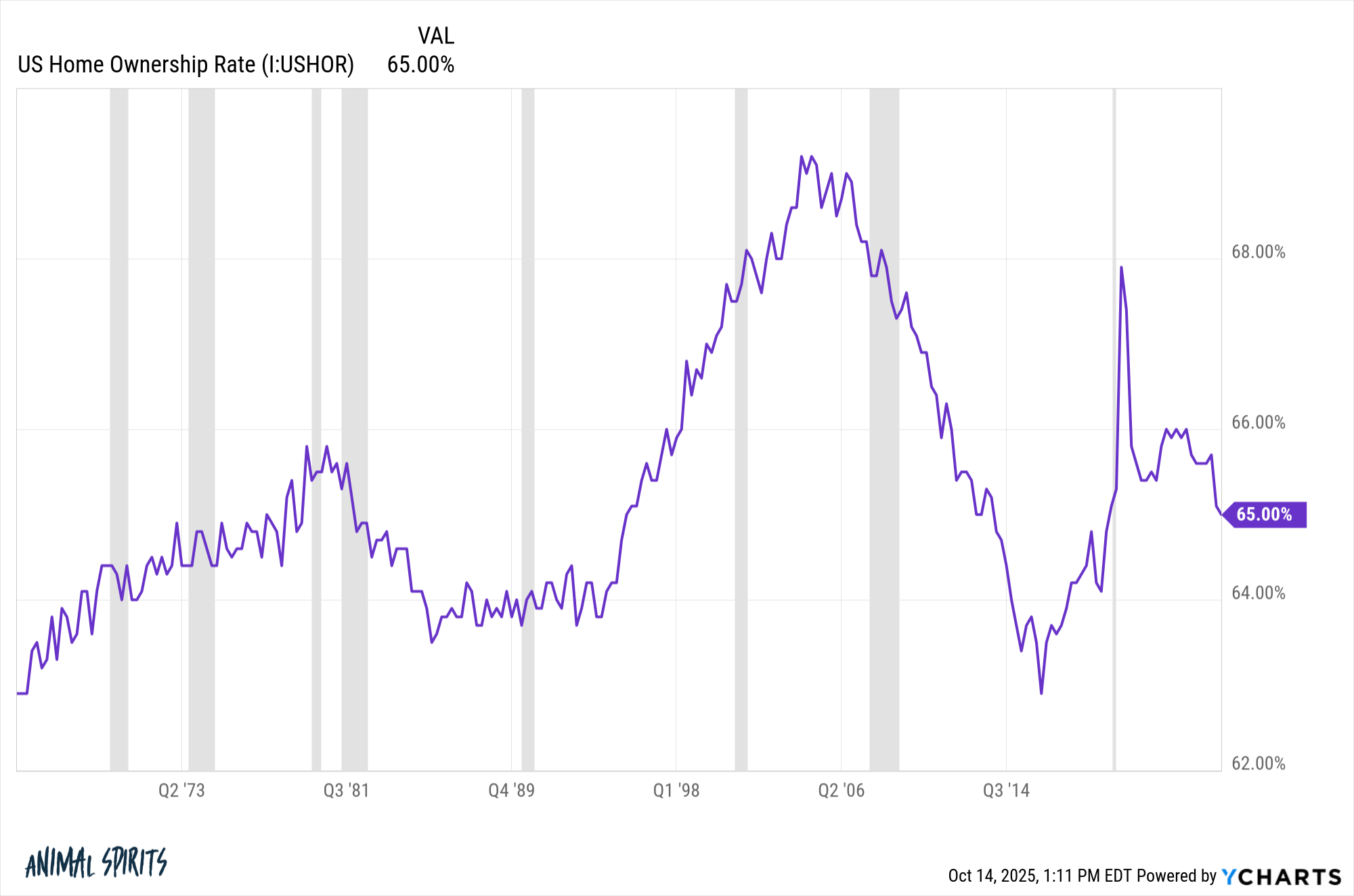

But it’s worth noting that the homeownership rate in America is still 65%:

62% of American households own stockscompared to 52% in 2016.

We still have wealth inequality and high housing costs. I will not dispute those claims.

However, a majority of Americans own financial assets. More low-income households are investing in the stock market than ever before. Young people are widely involved in stocks.

These are positive developments. The stock market is the greatest wealth building machine on planet Earth.

Things can always be better, but this is good news.

Further reading:

Two of the biggest trends of this decade

1Frankly, there is no such thing as an index fund for housing. Calculating the true return on housing, after all the additional costs and leverage, is virtually impossible.

#positive #trends #household #prosperity #wealth #common #sense