TUAS: Board Vooruit with strategic acquisition and growth potential

As we have reported earlier, TUAS LTD (ASX: TUA) is a rising star in the telecommunications sector. The company remains its position as a formidable player in the competitive telecom market of Singapore. Broker Peloton Capital has also followed the company closely and recently reported on a large takeover.

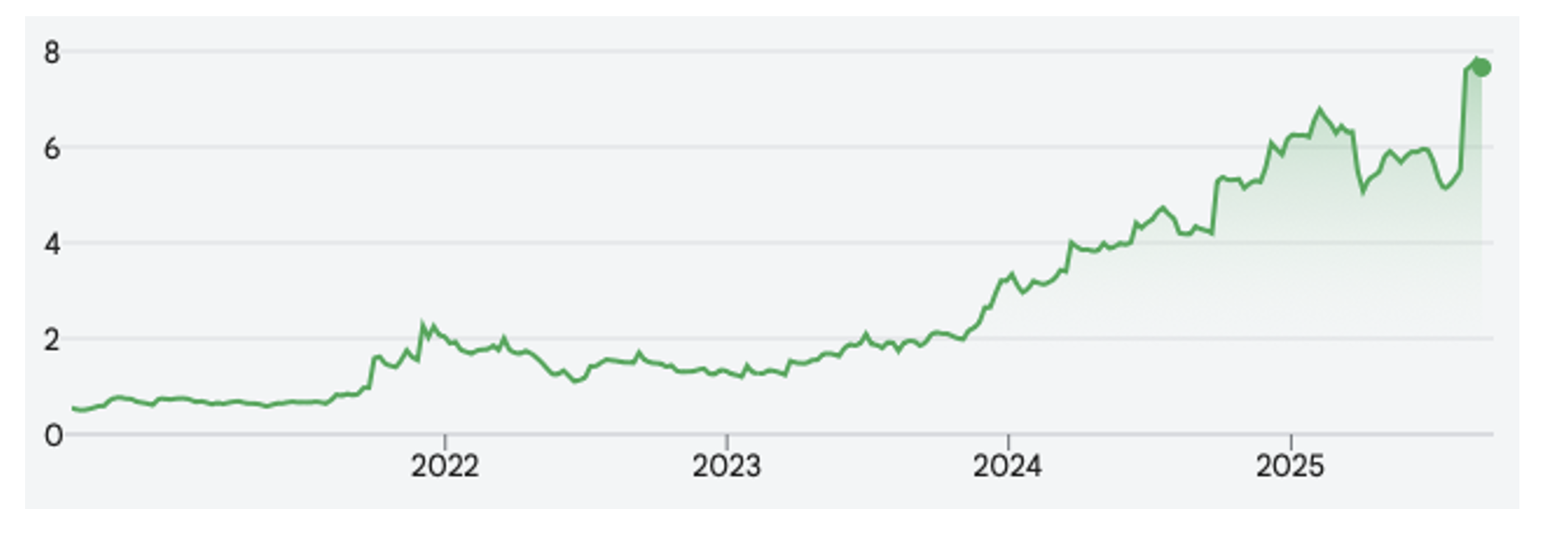

Figures 1. Tuas (ASX: your) stock price

Strategic acquisition of M1

On August 11, 2025, Tuas announced the acquisition of M1 for Van Keppel for S $ 1.43 billion (S $ 1.1 billion in debts and S $ 330 million in cash), pending the approval of the regulations expected in November 2025. These transformative deal positions TUAS to become a full-service telecom provider. Within the first 100 days after the approval, management plans to implement cost-saving measures and to set ambitious goals, with synergy benefits that are expected to occur in the second half of 2026. Estimates project pro-forma income of S $ 949 million and income (eBitda) of $ 3rd, depreciation and amortization.

S&P/ASX 200 Inclusion

An important motivation in the short term for the share price of TUAS is the potential admission to the S&P/ASX 200 index, with the following index changes announced on 5 September 2025. Inclusion can considerably increase the valuation of the shares and attract a larger investor’s interest, making it a pivotaal moment for the company. Of course, if it is not included this time, it won’t be long before it is, all things that are the same.

Beyond synergies

Although synergies of the M1 acquisition are considerable – possibly reach S $ 100 million annually (with a conservative estimate by Peloton of S $ 50 million) – the growth test of TUAS is much further than the cost efficiency. The company is well positioned to make substantial opportunities in:

- Broadband of the consumer: With a combined market share of only 16 percent, there is sufficient growth room by offering the best value plans to consumers.

- Business market: TUAS wants to replicate its success of the consumer market by focusing companies on competitive plans. The Enterprise market in Singapore is described as “increasing”, with a considerable potential, although its size is a challenge to quantify.

- Emerging opportunities: Additional growth roads include Goose Esim and Machine-to-Machine (M2M) services that offer valuable optionality. The Broker Note also projects the mobile market share of TUAS in the course of time to rise to around 40 percent.

Operational efficiency and cost optimization

TUAS is expected to stimulate the capital expenditure (Capex) considerably among the historical levels of M1, with estimates of approximately S $ 80 million a year, including spectrum payments for the next three years. Both TUAS and M1 use Huawei equipment, so that network optimization on software content may be able to further reduce costs. This focus on efficiency is expected to strengthen the competitive advantage and the prospects of TUAS.

Investment

As a defensive stock with strong growth prospects, Tuas is seen by platoon and investors as well positioned to deliver value. The combination of his M1 acquisition, potential index recording and various growth opportunities in consumer and company markets makes it a compelling candidate for further research. Peloton remains Bullish, convinced that the TUAS journey will be very profitable for shareholders in the coming years.

Tuas is not only a story driven by synergy, but a dynamic telecom player with a considerable growth potential in Singapore’s consumer and company markets, and perhaps beyond. With a strategic acquisition, cost optimization and a clear path to market leadership, TUAS is one to look at. The upcoming S&P/ASX 200 index decision could serve as a catalyst in the short term, while in the long term investors can look forward to persistent growth and profitability.

You can read earlier articles about Tuas:

Roger Montgomery is the founder and chairman of Montgomery Investment Management. Roger has more than three decades of experience in fund management and related activities, including stock analysis, stock and derivative strategy, trade and effects. Prior to the establishment of Montgomery, Roger positions in Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also the author of the best -selling investment guide for the stock market, value. Aabel-Hoe to appreciate the best shares and buy them for less than they are worth.

Roger regularly appears on television and radio, and in the press, including ABC Radio and TV, the Australian and Ausbiz. View upcoming media performances.

This message was contributed by a representative of Montgomery Investment Management PTY Limited (AFL No. 354564). The main purpose of this message is to provide factual information and not to provide financial product advice. Moreover, the information provided is not intended to give a recommendation or opinion about a financial product. However, each comments and opinion of opinion can only contain general advice that has been drawn up without taking into account your personal objectives, financial circumstances or needs. Therefore, before acting on the basis of one of the information provided, you must consider the suitability in the light of your personal objectives, financial circumstances and needs and you must consider requesting independent advice from a financial adviser if necessary before you make decisions. This message excludes specific personal advice.

#TUAS #Board #Vooruit #strategic #acquisition #growth #potential