A reader asks:

Can you share how to use momentum indicators and stop losses to profit from an AI bubble? Having been an investor in the 1990s, this feels like the beginning of a bubble, if this is one. I think there is a way to make profits with relatively little risk without picking individual winners or timing the top, by using momentum indicators and trailing stop loss orders on broad, passively managed ETFs.

In the spring of 2006, Meb Faber published a research article entitled A quantitative approach to tactical asset allocation.

The idea was to use a ten-month moving average to determine your allocation between risky assets (stocks) and cash (T-bills).

The rules were simple. At the end of the month:

- If the current price is higher than the 10-month moving average, stay invested in stocks.

- If the current price is lower than the 10-month moving average, invest in cash.

If you are in an uptrend, buy or stay invested. If you are in a downtrend, sell or stay cash.

The idea behind the strategy is to dampen volatility and the risk of severe market downturns in risky assets.

The timing of the paper couldn’t have been better. Just over a year later, the stock market peaked with the outbreak of the Great Financial Crisis. The S&P 500 fell almost 60%.

How did Faber’s rules work? Incredibly good.

Meb updated his article a few years later to show how the backtest performed in the real world:

The strategy didn’t exactly hit the top because you have to wait for a downtrend to hold before getting a signal, but the strategy missed most of the carnage.1

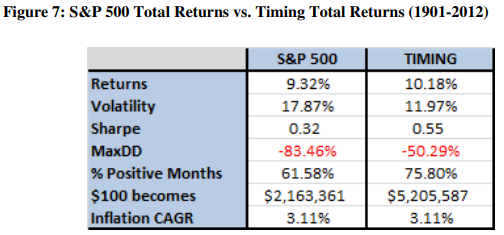

These were the long-term return profiles for trend following versus buy and hold:

Trend following hasn’t completely wiped out the declines, but it has significantly dampened the volatility in these more than 110 years of data.

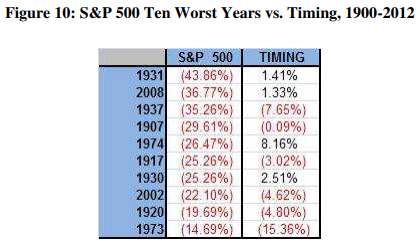

Now take a look at the performance of the stock market’s worst years versus the trend strategy:

This type of strategy is designed to shine in the worst stock market conditions.

There’s nothing magical about 10 months or a monthly indicator for these things, but the point is that you want to have a time frame that allows you to better define upward and downward trends.

Bad things happen more often in down markets because investors tend to panic more freely when they lose money. This is why both are the best And the worst days occur during bear markets.

Downward trends pave the way for a broader range of possible outcomes, and not always in a good way.

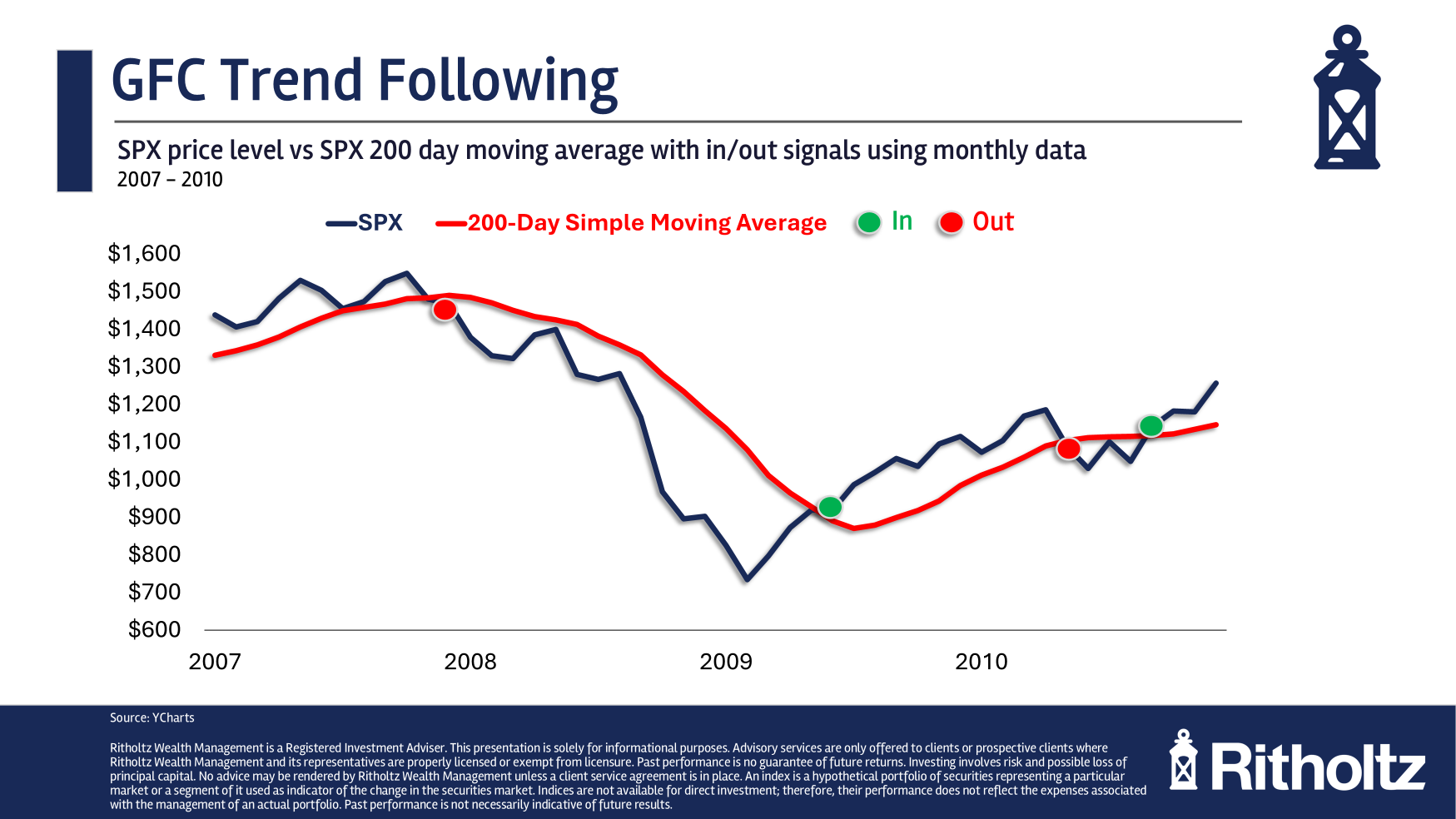

Here’s a look at the use of a simple 200-day moving average on a month-end basis during the 2008 financial crisis:

The sell signal was triggered about 6% below the peak, which was very good timing. Then you came back in about 20% off the lows. That’s pretty good considering the size and duration of the 2007-2009 crash.

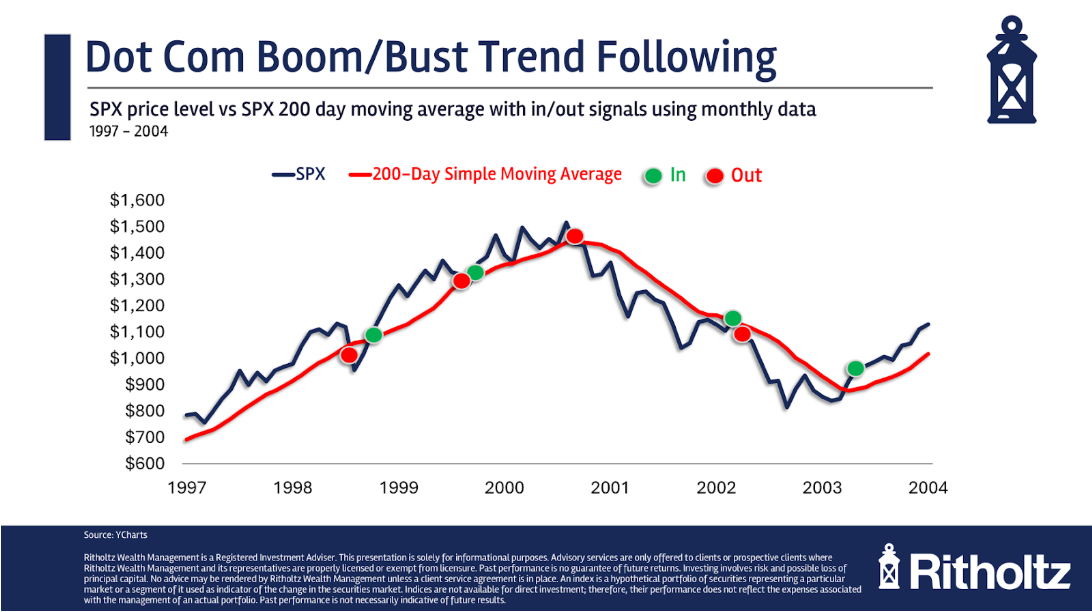

Here are the signs during the dotcom bubble:

You can see that there were some false positives on the way to the top of the dotcom bubble. You sold and got right back in during the volatility of 1998. In 1999 there was another swing when the moving average produced a sell signal, followed shortly after by a buy signal.

But then there was a sell signal at the end of the month that was just 6% below the 2000 peak, keeping you out of most of the 50% crash. Another quick swing in 2002, but once again a trend-following system helped you survive a severe recession.

So why would you ever invest in anything else?

Well, following trends is a wonderful hedge against serious market downturns. But serious market downturns are not that common. Crashes are rare.

Drawdowns don’t always happen in waterfall fashion. If there is a flash crash situation, a trend following strategy will not save you. And in turbulent markets you can be whipped.

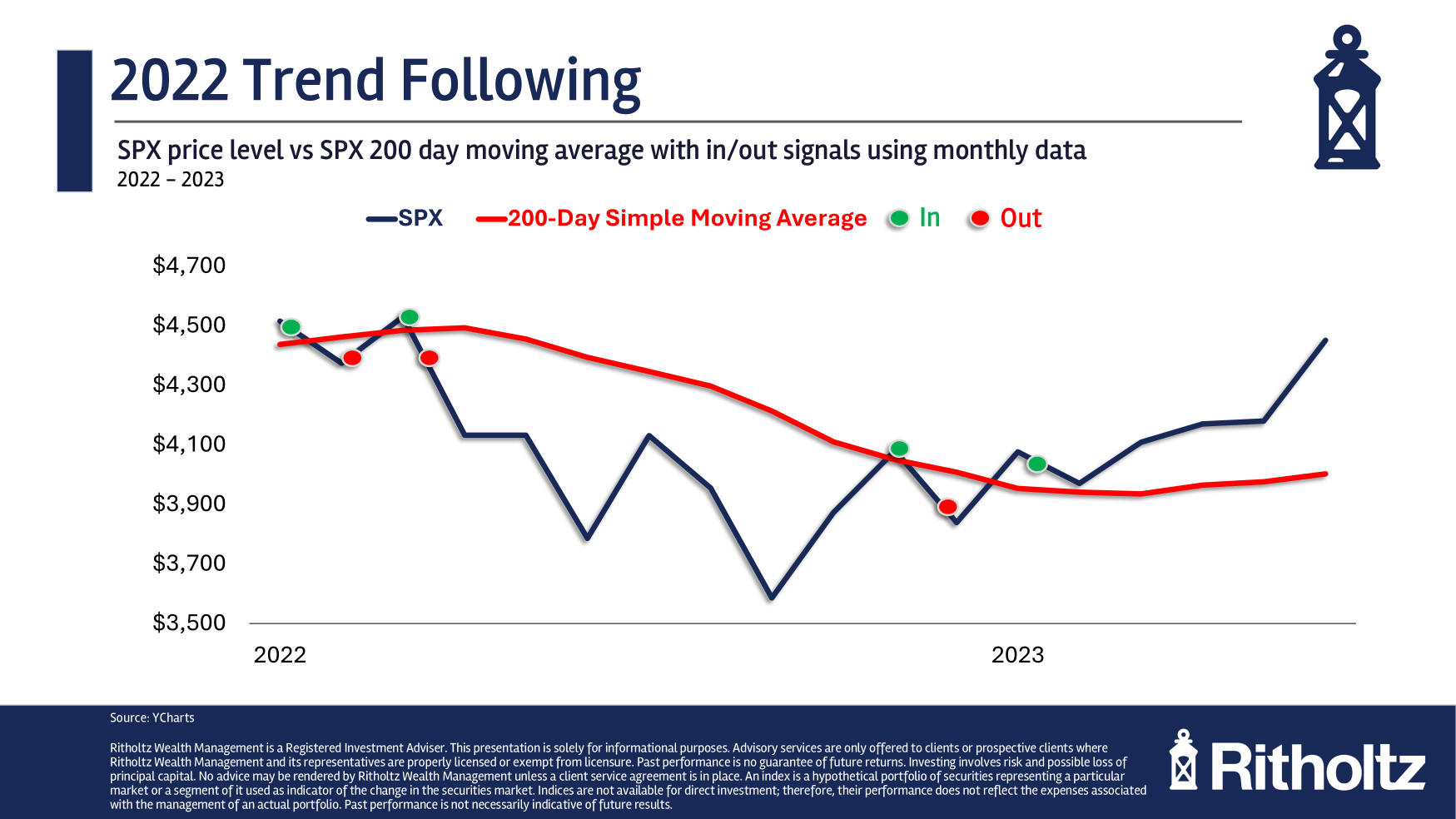

Look at the 2022 bear market:

You bought high, sold low, bought higher and then sold low again. You still missed a fair amount of the shot, but those whipsaws can test your patience.

You might see a 10% down month, sell and see that, followed by a 10% up month where you buy after the gain. Now you’ve just eaten all the losses and missed all the gains in a short period of time.

Here’s the thing about a trend strategy: you have to follow the rules for it to work. No hesitation. No emotions involved. You can’t buy and sell whenever you feel like it because no one knows if a 15% correction will turn into a 50% drop or not. Usually 20% down doesn’t turn into 40% down, but no one knows that at the moment.

Trend following is an insurance strategy that sometimes forces you to pay the premium without the protection. When you trigger a sale, the stock market usually won’t fall completely out of bed, but you don’t buy insurance on your house hoping it burns down.

Sometimes the stock market burns down, but that rarely happens.

You also have to take taxes into account. When you trigger a sell signal, you may be forced to pay short-term capital gains. Or you may be forced to pay long-term capital gains after a long bull market. This is at the expense of your returns. Trend following works much better in a tax-deferred account than in a taxable brokerage.

Bull markets are another positive for this strategy.

Most hedging strategies provide protection against downside volatility without upside potential. The great thing about following trends is that you stay invested as long as the stock market remains in an uptrend. And when the uptrend breaks, there is an off-ramp.

This type of strategy is not for everyone. I’ve had many conversations over the years with people who simply don’t want or need a volatility/behavior relief valve.

Others desire something that will help them stick to the rest of their long-term plan. That’s why I think following trends is a nice addition to a longer-term asset allocation, ‘buy-hold-and-rebalance’.

These strategies may work differently in different environments and at different points in the cycle.

The potential for reduced volatility is nice, but it’s the diversification benefits that helped me understand the point of trend following in a portfolio.

I don’t know if following trends will protect you when the next big recession hits.

But this is the kind of strategy where you need to understand the tradeoffs before investing.

If you would like to know more about how we do this for customers, please contact us here.

I delved deeply into this question in this week’s Ask the Compound:

Bill Sweet also joined me to discuss questions about Roth IRAs before retirement, buying your dream home, capital loss carryforwards, 529 plans, and buying a vacation home for estate planning reasons.

Further reading:

My evolution in asset allocation

1It’s also worth noting that the trend strategy underperformed by quite a large margin in the 1990s bull market. You can expect that with a strategy like this.

#Trend #bubble #wealth #common #sense