Want more housing market stories from Lance Lambert’s ResiClubin your inbox?Subscribeto the ResiClubnewsletter.

Back in his 1996 letter to shareholdersWarren Buffett famously said, “If you’re not willing to own a stock for ten years, don’t even think about owning it for ten minutes.”

This statement only makes the recent buying and selling of shares in homebuilders by Berkshire Hathaway – led by Buffett, who will step down as CEO at the end of 2025 – raise even more eyebrows.

Here’s the timeline.

- August 2023: Berkshire Hathaway announced that the company had made a bet on US homebuilders in the second quarter of 2023, buying 5,969,714 shares of DR Horton, 152,572 shares of Lennar and 11,112 shares of NVR.

- February 2024: Berkshire Hathaway announced that the company had sold 5,969,714 shares of DR Horton in the fourth quarter of 2023 – the vast majority of Buffett’s big homebuilder bet he made in early 2023.

- August 2025: Berkshire Hathaway announced that the company had made a bet on US homebuilders during the second quarter of 2025 (the three months ending June 30) by purchasing approximately 1.5 million shares of DR Horton (worth approximately $191.5 million). In the first half of 2025, Berkshire Hathaway acquired just over 7 million shares of Lennar, worth nearly $800 million.

- November 2025: Berkshire Hathaway announced that it has sold its stake in DR Horton of approximately 1.5 million shares.

Although Berkshire Hathaway has sold its shares of DR Horton (No. 123 on the Fortune 500), it still owns approximately 7.2 million shares of Lennar (No. 129 on the Fortune 500) and approximately 11,112 shares of NVR (No. 396 on the Fortune 500), according to ResiClub’s review of Berkshire Hathaway’s latest SEC filings.

Given Buffett’s own advice — “If you’re not willing to own a stock for ten years, don’t even think about owning it for ten minutes” — it’s probably fair not to draw sweeping long-term housing market conclusions from Berkshire Hathaway’s homebuilder trading over the past two years. After all, the company bought them, sold them, bought them again and sold them four times in just over two years.

That said, if you force me to speculate, I think Berkshire Hathaway initially looked at homebuilder stocks in the first half of 2023, following their sharp decline in 2022 as builders adjusted to the interest rate shock. But heading into 2024, Berkshire Hathaway may have long gotten cold feet with homebuilders, as it became clear that the strengthening of the housing market in early 2023 was a bit of a hoax – and that a greater shift in power towards buyers, a further weakening of the housing market and further compression of homebuilder margins were still in the offing.

After that happened earlier this year, Berkshire Hathaway may have concluded that most of that margin compression was already priced in and that the company wanted to get back to taking advantage of the homebuilders.

That speculation still leaves one question open: Why would Berkshire Hathaway now sell DR Horton while still holding Lennar and NVR?

First, DR Horton shares have seen a stronger recovery in recent months, while Lennar and NVR have not. (Perhaps Berkshire Hathaway believes a recovery is still underway.) So it may not be that DR Horton has fallen out of favor with Berkshire Hathaway, but that DR Horton’s shares have already priced in much of their short-term upside potential.

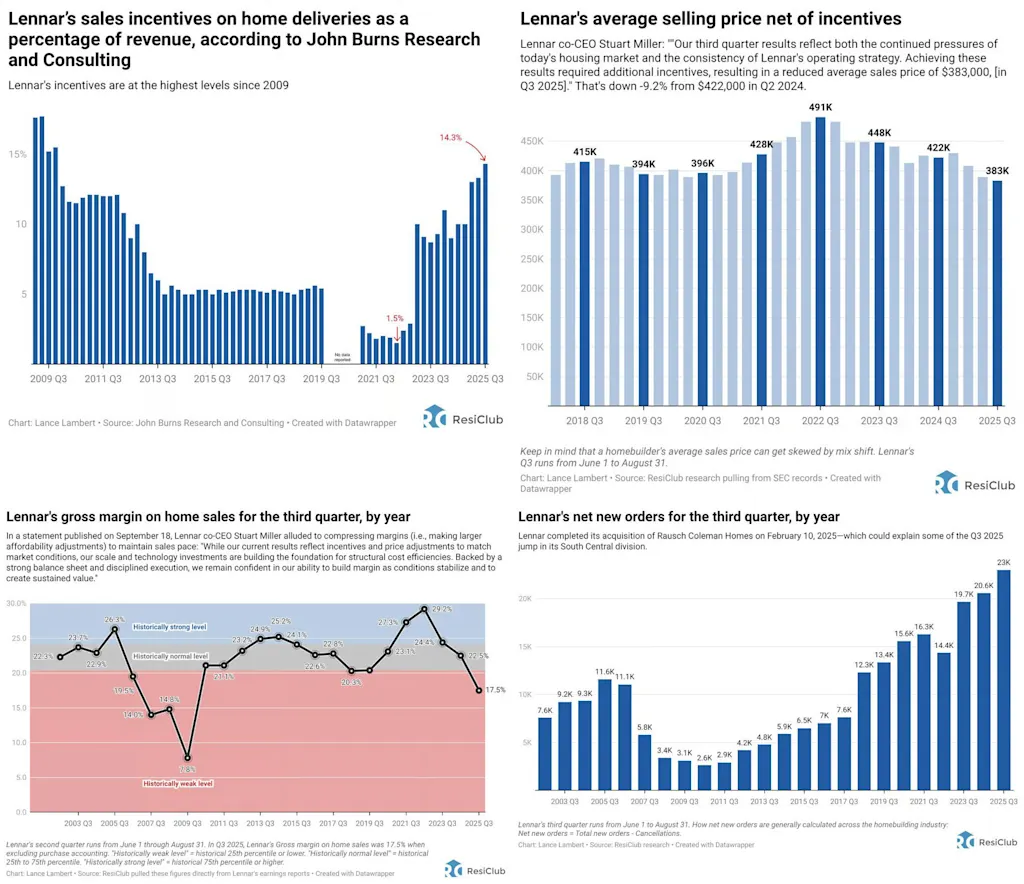

Second, and I’m reading deeply between the lines, Berkshire Hathaway may like the fact that Lennar has been more aggressive in capturing market share during this soft period. While all of the public homebuilders ResiClub tracks have compressed profit margins over the past three years to provide greater incentives and affordability adjustments in an effort to prevent a sharper decline in housing projects, Lennar has been the most aggressive on that front.

In fact, Lennar has slashed its margins to 2009 levels, and is spending the equivalent of roughly 14.3% of final sales on incentives (compared to the typical 5% to 6% in normal times) to grow home sales and capture market share.

In September 2025, Lennar executives recognized that the time had finally come “time to take a break [that strategy] and let the market catch up a bit.” That doesn’t mean they will completely reverse course or lose the market share they recently gained using the strategy. Instead, it means they can’t be as aggressive in pursuing additional market share in early 2026, given the margin compression they’ve already absorbed.

Some investors, including Berkshire Hathaway, might like that Lennar has pursued greater market share during this turbulent stretch and is now starting to defend margins.

Here’s what Stuart Miller, co-CEO of Lennar, said during the company’s earnings call on September 19, 2025:

“For Lennar, this is a good time to pause and let the market catch up a bit. Although mortgage rates began to decline towards the end of the quarter, stronger sales have not yet followed. We have certainly started to see the first signs of increased customer interest and stronger traffic entering the market. With lower mortgage rates, buyers are showing more interest in considering purchasing their home. And this is generally an early signal that stronger sales activity will follow, assuming interest rates are lower stay.

And if interest rates continue to fall, we’re pretty optimistic that this will all happen soon. However, the continued period of higher interest rates that lasted longer than expected forced us to adjust construction costs [lower average sales price] to enable sales in difficult market conditions. Our lower construction cost structure, along with a lower margin [bigger incentives]have allowed us to remain affordable and support the balance between supply and demand.

We have accelerated sales to match production, and we have strengthened our market share and position in each of our strategic markets. We now find ourselves in a position with a lower cost structure, efficient product offering and strong market positions to meet pent-up demand as interest rates fall and confidence eventually returns. As I said before: this is the right time. This is exactly the right time to pull back a little.

We believe we have been one step ahead of current market realities and have built what we believe to be a stronger platform that drives margins over the long term. We know this has taken some time as the market has remained weaker for some time, but we also know that our strategy has helped build a healthier housing market and positioned Lennar for strong cash flow and earnings growth going forward.

Although our completions were just below our target for the quarter, and although we sold more homes than expected during the quarter, this performance came at the cost of a further deterioration in margin, which stood at 17.5%. Accordingly, we will be reducing our delivery expectations for the fourth quarter and full year to alleviate pressure on sales and deliveries and help achieve margin expansion. We are lowering our delivery expectations for the fourth quarter to 22,000 to 23,000 homes and for the full year we are lowering our expectations to 81,500 to 82,500.”

In addition to the homebuilding stocks of Lennar and NVR that Berkshire Hathaway still owns, the company also wholly owns Clayton Homes – the largest U.S. builder of manufactured and modular homes – and HomeServices of America, a Berkshire Hathaway affiliate (under Berkshire Hathaway Energy) that offers a wide range of real estate services, including brokerage, mortgage origination, and title and escrow services.

#housing #market #cycle #unique #Warren #Buffett #broke #rules #money