The artificial intelligence web of deals

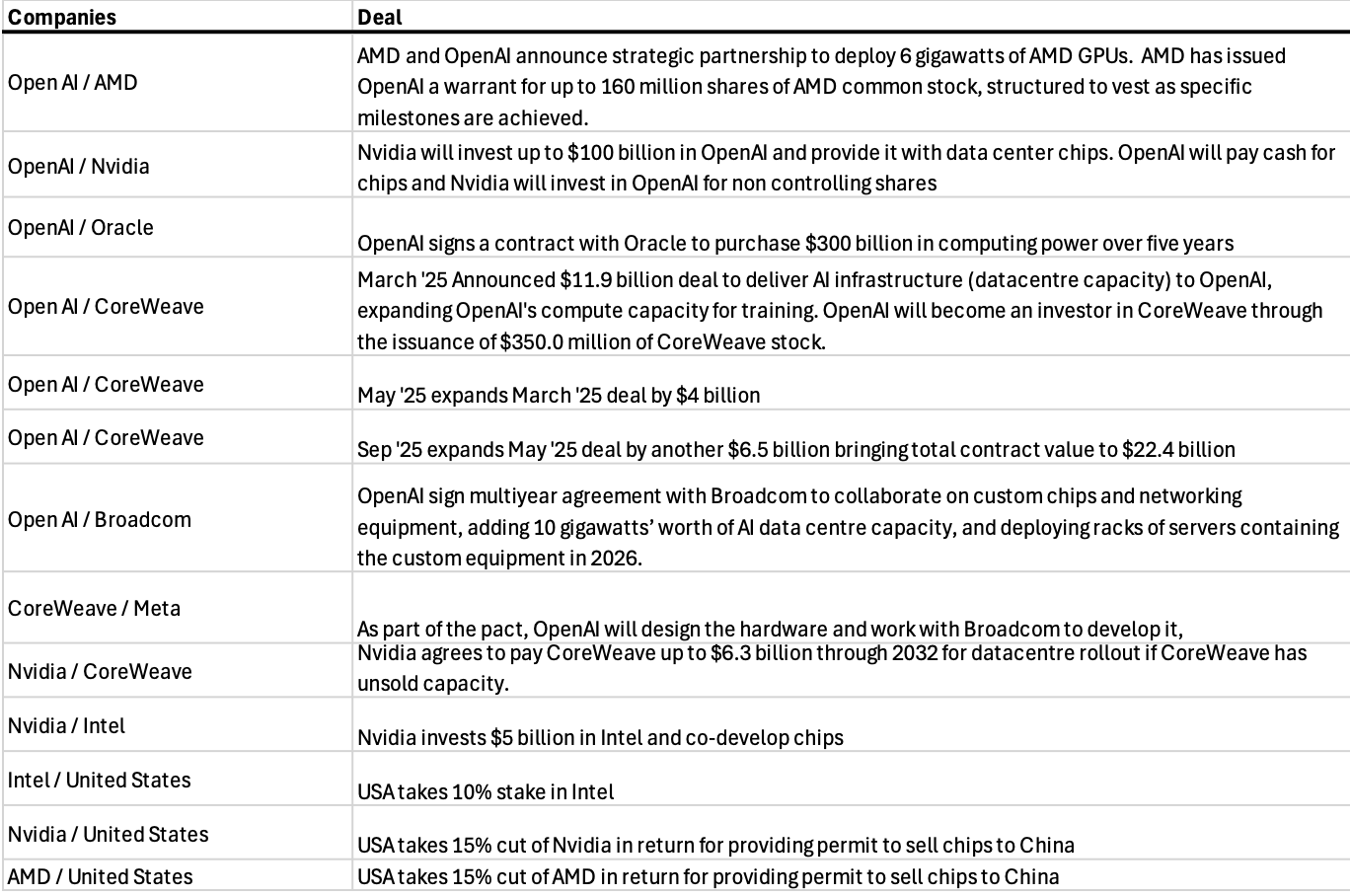

Earlier this month, Nvidia – the company at the center of the artificial intelligence (AI) boom – announced that it had agreed to invest up to $100 billion in OpenAI to help the Large Language Model (LLM) maker finance the buildout of its data center. In turn, OpenAI agreed to fill those data centers with Nvidia chips.

If it sounds strange, it is. That’s because it’s akin to convincing Nick Scali to buy you a house if you agree to fill it with Nick Scali’s furniture.

In fact, the Nvidia/OpenAI deal was immediately criticized for being “circular.”

Not to be deterred, OpenAI then signed a new deal, this time with Advanced Micro Devices (AMD) to deploy 6 gigawatts of AMD Graphic Processing Units (GPUs) in its data centers at a cost of tens of billions of dollars. In return, AMD actually issued shares to OpenAI. AMD then essentially trades stock for a guaranteed customer, allowing its chips to find a home in OpenAI’s data centers.

Within days of the Nvidia deal, OpenAI had also signed a deal with Oracle to buy $300 billion in computing power (data centers) in the US

Table 1 lists a handful of deals that reveal the extent of AI-related companies’ spending on, well, each other.

Perhaps the pace and scale of investment by AI companies has confused analysts who now worry that the web of deals being undertaken to support a boom that will make the underlying technology’s ability to generate sufficient revenue to generate a satisfactory return on investment (ROI) largely speculative and potentially elusive.

The looming problem for me is the concept of ‘one in – all in’. If sentiment turns, they will all perish together. They probably would anyway.

And it’s not like there’s no debt involved. While the AI build – major tech companies promised a record $320 billion in capital expenditures by 2025 – has been largely self-financed to date, Morgan Stanley estimates that capital expenditures (capex) are expected to reach $2 trillion by 2028 and that $1.5 trillion of that may need to be financed with debt.

Major tech companies have committed a record $320 billion in capital expenditures by 2025, Fortune writes. That number is growing so much that according to Morgan Stanley, as much as $1.5 trillion of that will come from various forms of debt.

Debt is fine if a company can finance it, but as Forbes recently noted, Oracle is already losing $100 million per quarter on leasing its data centers to OpenAI, despite signing a five-year, $300 billion deal with them.

Table 1. AI Deal-a-Thon

Source: Montgomery Investment Management

Not to be outdone, and perhaps out of fear of missing out (FOMO), Elon Musk recently announced a $20 billion equity and debt increase. Elon Musk’s company XAI, which operates the Grok LLM, will buy Nvidia processors and then rent them out. Nvidia, for its part, will commit up to $2 billion to Musk’s raise.

It sounds a bit like you give me a billion to buy your stock and then you use that money to buy my stock and then I use it to buy your stock… and so on and so forth.

In fact, Goldman Sachs analyst James Schneider pointed out in a research note that “NVIDIA’s investments flow as funding, returns are realized through GPU sales, inflating reported growth.”

In other words, while every trade promises to fuel the next technological revolution, beneath the hype lies a pattern of interconnected, self-reinforcing trades – known as the Shell Game – that some say reflect troubling chapters in stock market history. (Shell Game – an anecdote used in business to describe the act of using psychological tricks to convince ‘potential players’ of the legitimacy of ‘the game’.)

I don’t know anyone who has added up all the expenses and then estimated what the total addressable market size needs to be to generate an appropriate ROI, and then figured out if this is possible. And what if the downstream buyers of AI tools decide it’s not worth the effort? According to MIT, earlier this year 95 percent of AI pilot projects did not deliver sufficient returns and many internal AI projects were halted.

While no aggregated figures exist, some individual estimates do exist. According to Reuters, OpenAI needs to generate $125 billion in revenue to break even, and is not expected to do so for at least four years. Until then, OpenAI must finance its losses by issuing shares.

Nevertheless, most investors believe the AI boom will continue, that downstream users will discover creative new applications for AI and LLMs, that revenue growth will accelerate, and that current investments will become profitable.

Another possible scenario, albeit one with lower probability, is the one my twenty-year-old son suggested. His idea is that LLMs have already leveraged their capabilities. ChatGPT 6, 7 and 8 will not deliver the improvements we saw in the early versions. He thinks the money flows will shift from LLMs to robotics. Initially, both will receive funding as investors confuse the two, but eventually one must slow down so the other can grow.

The most pessimistic scenario involves OpenAI being unable to finance its $14 billion annual loss. The problems revealed in Table 1 would result in CoreWeave losing 60 percent of its revenues, in turn becoming unable to pay the interest on its $14.5 billion debt, and filing for bankruptcy. The fear of contagion would then have the effect of curtailing further growth, calling into question the validity of the stretched price-earnings ratios (P/E). Although this scenario is currently considered the lowest probability scenario of an event, the probability is not zero.

What should you pay attention to?

The first thing is to remember that when stock prices become exponential, profits become unsustainable. Rarely do vertical rises end with prices going sideways. Normally they return quickly.

Figure 1. Global venture capital transaction activity

Source: Pitchbook

It’s also worth taking a look at OpenAI’s quarterly announcements and comparing its cash burn rate to revenue growth. Market analysts will also monitor customer acquisition and churn. Ultimately, companies reach a glass ceiling in terms of total customers, and are forced to spend more to acquire new customers as old customers leave. That’s churn.

CoreWeave’s debt mountain requires $250 million in interest payments per quarter. Operating income in the last quarter was only $19 million. Keep an eye on that and at the same time check out the pace of VC deals on data provider Pitchbook. According to Pichbook, venture capital firms have injected $192.7 billion into artificial intelligence startups so far this year. That’s more than half of the $366 billion total in venture capital deals worldwide.

However, if the flow of venture capital deals into AI companies starts to slow, it could signal a waning appetite and a recalibration of risks. Given the long-term nature of venture capital commitments, investors may be forced to liquidate publicly traded equities to generate cash as their risk perceptions change.

Lessons from the past

History is littered with precedents of similar circular business models inflating bubbles, only to lead to sharp market corrections.

The most obvious parallel is the Internet bubble of the late 1990s, when technology companies engaged in cross-advertising and cross-selling to artificially increase revenues.

At the time, companies like WorldCom and Global Crossing traded network capacity in circular swaps, inflating reported growth and valuations until the house of cards collapsed in 2000-2002, wiping out trillions in market value.

Vendor financing was also widespread then: Cisco, like Nvidia now, lent money to startups who then bought their routers, creating an illusory demand that evaporated when the bubble burst.

The stock market crash of 1929 involved leverage spirals in which banks and brokers extended credit in circular loops, and in the 2008 financial crisis, collateralized debt obligations (CDOs), created by banks that packaged and resold subprime mortgages, led to a global collapse as the underlying assets soured.

There are of course differences. We don’t have the IPO mania of the 2000s tech boom, systemically important banks don’t have AI securities on their balance sheets like CDOs did in 2007, and investors are probably much more sophisticated than those of 1929.

But investor behavior remains unchanged and the immediate market reaction to recent AI deals has been euphoric. AMD’s shares rose 24 percent after the OpenAI announcement, while Oracle rose 43 percent after the acquisition, making billions for insiders like CTO Larry Ellison. Nvidia’s market capitalization has risen to $4.5 trillion, making it the most valuable company in the world.

If AI revenues lag — OpenAI admits cash flow won’t be positive until the end of this decade — valuations could quickly deflate, as previous hype-fueled tech booms have done. And given the interconnectedness of the AI ecosystem, we could all catch a cold if someone sneezes.

Roger Montgomery is the founder and chairman of Montgomery Investment Management. Roger has more than three decades of experience in fund management and related activities, including equity analysis, equity and derivatives strategy, trading and securities brokerage. Before founding Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also the author of the best-selling investing guide to the stock market, Value.able – how to value and buy the best stocks for less than they are worth.

Roger regularly appears on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The main purpose of this message is to provide factual information and not advice about financial products. Furthermore, the information provided is not intended as a recommendation or opinion about any financial product. However, any comments and statements of opinion should contain general advice only, prepared without taking into account your personal objectives, financial circumstances or needs. Therefore, before acting on any information provided, you should always consider its suitability in the light of your personal objectives, financial circumstances and needs and, if necessary, seek independent advice from a financial advisor before making any decision. Personal advice is expressly excluded in this message.

#artificial #intelligence #web #deals