In a rare fit of generosity, the Monetary Policy Committee (MPC) decided in its June meeting to lower the Repo rate with 50 basic points and to beat the Cash Reserve Ratio (CRR) for banks with 100 basic points. The CRR section will be phased out from September to November over four tranches.

Both REPO rate and CRR reduction will, as everyone knows, lower the interest rates on loans and deposits, because banks and NBFCs pass on their cost savings to their customers.

This is the reason why many investors commanded that the market revenues on bonds actually enriched after the MPC announcement. For example, between June 5 (the day prior to the MPC meeting) and June 12, the marketing on the five-year Indian government bond increased from 5.78 percent to 5.98 percent and that the 10-year bond rose from 6.18 percent to 6.35 percent.

Why market rates rose

There is a good explanation why the interest rates of the market have risen and have not fallen after the policy evaluation on 6 June. Bond markets, such as stock markets, are future -oriented and try to invoice events before they unfold. With the MPC that indicates its intention to lower the rates from the beginning of 2025, bond markets for the MPC are sustained. Consequently, the bond returns in the rental points have fallen for 18 months or more.

The corresponding table shows us that the proceeds on government effects (G-SECs) have been taken from the beginning of October 2023. From January 1, 2025, the proceeds on G-SECs have fallen between 43 and 123 basic points, depending on the tenor.

After the expectation that the MPC would continue for many months with the interest rate rate, the market was unexpectedly caught on 6 June by the signal that the MPC can now pause and make the balance before the rates are trimmed further. The statement by the Governor on 6 June said that after rapid reduction of the Repo rate with 100 basic points, the monetary policy remains with “very little room” to further support growth. That is why the MPC would “carefully assess” incoming data for future tariff actions. The MPC that turns its policy position from “accommodation” into “neutral” also underlined this message.

These are strong hints that further rates actions of the MPC will now be during break, unless there are surprises from incoming GDP or inflation data. It is this signal that the bond markets have encouraged to be at the back of track after the policy. Before they mark the rates further, they will now be looking for instructions of monthly inflation numbers, quarterly GDP prints and future MPC meetings to get a solution at interest rates from here.

These mixed signals from the latest MPC meeting request a pivot point in your strategy for debt investment. Here are the changes that you must make to your debt portfolio.

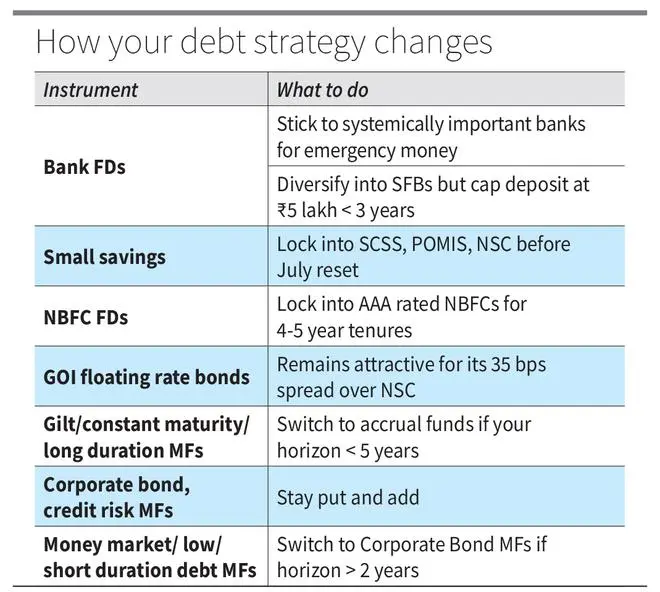

Closing the FD window

Although the MPC has so far reduced policy percentages with 100 basic points in 2025, banks and NBFCs have not reduced their fixed deposit rates. This is because intense competition to forced deposits to hold on to their FD rates to use deposits. But this situation has changed in recent months. With the RBI that makes sufficient liquidity available for banks via Open Market Operations (Omos) and other roads, the Scramble For Deposits is reduced for the large banks. Systemically important banks have therefore struck their FD rates sharply. As the CRR -Cut yields more easily in the hands of banks from September, further reduction of the FD rates in the bank are ahead.

Systematically important banks, the go-to banks for large deposits, are usually the first to send tariff reductions because they find it easiest to collect deposits. That is why the interest rate rates of Post-Policy, HDFC Bank on an FDs of one year, three years and five years have fallen to 6.25 percent, 6.40 percent and 6.15 percent respectively. Even before the HDFC Bank policy had trimmed its savings bank rate to 2.75 per CET. SBI’s rates are now at 6.5 percent, 6.55 percent and 6.30 percent. Other banks in the public sector will probably see fast FD rate reductions.

What to do

Although systemically important banks are usually the first to scrap rates, private banks with weaker financial data such as Indusind Bank (6.85-7.35 percent on one of the three years FDs), RBL Bank (7.1-7.5 percent) and small financial banks such as Equitas (7.6-7.8 percent) and AU SFBB (7.1-7.8 percent) bid. This is because these banks usually have it more difficult to collect deposits. (The rates mentioned are at the time of writing this article and can change).

FDs with smaller private banks and small financial banks clearly have higher risks than systemically important banks or PSU banks. Savers can get a selective benefit of their higher rates by covering their FDs in them at £ 5 Lakh per bank. This is because account balance (deposits plus savings balance balance) of a maximum of £ 5 with planned banks are protected by deposit insurance. However, these banks offer their best rates for up to three years of the term of office. It would be best for deposits to stick to these shorter maturities with these FDs. Among these choices, small financial banks currently seem to offer a better reward for risks.

Because NBFCs depend on banks and markets for their funds, FD rate rates in NBFCs usually fall in after banks have reduced FD rates in a falling tariff cycle. This time, however, NBFCs have already started reducing the rates.

AAA assessed NBFCs such as Sundaram Finance (7.5 percent for three years), Sundaram Home Finance (7.65 percent for three five years) still offers a lot. Although NBFC deposits do not wear deposit insurance, the pedigree and long track of these NBFCs makes good bets when taking care of and deposit distance. With NBFCs, investors must use the current opportunity window to maintain four years in current rates.

Post office or small savings schemes, where the central government reset the rates at the end of each quarter, are usually the last to adapt to a falling tariff cycle. Despite the reduction of the 50-base point in repo rates, schemes such as the Senior Citizens Savings Scheme (8.2 percent), the post office-monthly income schedule (7.4 percent) and national savings certificates (7.7 percent) still offer healthy rates. Investors and seniors must take the opportunity to hold on to such instruments before the rates are reset from 1 July. The combination of the sovereign warranty and high rates are currently making these instruments better than bank or NBFC deposits on the risk agreement.

Permanent US floating

Theoretically, investors in a falling speed cycle should prefer instruments with a fixed rate to a floating rate. That is why the time seems to be ripe for bond investors to now prefer fixed rate instruments above a floating rate. However, the actual decision today is not that easy.

With gilded yields in the market for the bucket percentages (as the table shows), bonds of floating speed (which are linked to G-EC yields) already have in a large part of the fall in interest rates. There can therefore be a limited logic to leave bonds of the variable rate now, after the announcement of 6 June. Many best performing debt funds are invested in the bonds of the government of India’s floating rate. Their return would have been moderated to a certain extent. Because fund managers will in any case accept active calls to the fixed versus floating question, it is not necessary for investors in debt funds to take some action.

However, the rate reductions have implications for existing and potential investors in the Goi Floating Rate Savings -bonds sold by the RBI (and leading banks). This bond, with a lock-in period of seven years, reset its interest rate every six months. However, it is necessary to note that the reset takes place with a delay. In addition, the interest rate on the bond is set at a 35-based point spread over the prevailing rate on the NSC. That is why the interest on this bond, currently at 8.05 percent, is probably only reset after NSC rates have changed. The NSC already offers a 25-30 basic point spread over the deposit rates. That is why the Goi Floating Rate Savings -Bonds will probably remain an attractive instrument for debt investors who can close their money and liquidity of liquidity for seven years.

Expensive versus structure

Investment funds invest in market instruments. As we saw, market instruments for MPC actions have carried out. That is why the critical piece of information for investors in the investment fund of this MPC meeting was the signal that the rates here will not fall much more.

This can ask for a shift in their debt strategy. With the market yields that fall sharply, debt funds that focus on long-term instruments (gilded funds with 10-year-old constant duration, long duration funds) to the top of the table with a year return of more than 11 percent. However, the introduction of these funds that are now in the hope of repeating performance is very risky, because much of the bonds is done and dusted. Long endurance connections can now see more two -way movements, because the speed direction has become unclear.

Investors who had a minimal five -year horizon, while betting on gilded funds, constant adulthood funds and long duration funds, can hold, because the speed cycle will eventually run. But those who cannot hold their money for five years now have to switch to corporate bonding funds or PSU and bank funds. These funds offer higher yields than Gilts and therefore offer potential for slightly better returns today. The liquidity that is released due to CRR debitings will probably also temper the short-term interest rate on the market in the coming months. In short, investors in debt funds across the board must brace themselves for a lower return with the possibility of higher volatility, because the easy money seems to be over.

Published on June 14, 2025

#RBI #rate #CRR #reduction #FDs #small #savings #debt #funds