Are you familiar with Greek mythology?

That was me for a while.

It was ninth grade, in 1994. I was taking a high school course called “Classical,” and we studied Greek mythology, ancient Roman culture, and Homer’s “The Odyssey” and “The Iliad.”

My teacher was Nancy Karrandjas, probably the most passionate teacher I have ever met in all my years at school.

She made me want to learn.

I was definitely more enthusiastic in ninth grade. I’m tempted to say I was a nerd, but I played every sport there was, so I didn’t fit the “mold” of the classic movie nerd.

The jump from eighth grade to ninth grade was enormous in every way. I think we can all agree it was a leap sociallybut in terms of course content and the way we learned it was huge.

Classics was a wonderful course, and it led students like me to take it Latin in class ten. The people who said, “Latin is a dead language, there is no reason to study it,” were completely missing the point. Most words in the English language are derived from Latin, so anyone interested in literature, writing, media literacy and the like would benefit from the research.

What I liked about Classics were the stories! Fables. Stories. Myths.

They serve as metaphors that still apply to life today, and I find that so incredibly powerful.

Are you familiar with Sisyphus?

Maybe not the name, but you’ve definitely seen this before:

Sisyphus is a famous character (or real person?) from Greek mythology who was punished in a way that was at once cruel and tragically ironic.

He was sent to the underworld and forced by Hades to push a huge boulder to the top of a hill. But as soon as he reached the top of the hill, the boulder rolled back to the bottom.

Sisyphus’ punishment was to repeat this exercise forever.

For all eternity.

Some would describe the exercise as ‘pointless’, while others would call it ‘pointless’.

I see this as a metaphor for many things in life where a difficult, arduous task is made frustrating by the realization that you will eventually have to do it all over again.

Take the real estate market for example.

Every January we start pushing a proverbial boulder up a hill.

We start slowly and methodically. We look at the horizon and plan accordingly.

We gain some momentum as we move into February, start looking forward to the busy spring market, push hard into March, April and May, and then catch our breath as we move through June, July and August. Then our final push to the top takes place in September, October and November, before reaching the summit in December.

We stand at the top of the hill and look down where we started.

But Than what’s happening?

Well, the boulder rolls back to the bottom of the hill, and we start it all again in January.

If you were really sadistic, you could apply this metaphor to every year of your life, but we’re not going there today.

However, when it comes to real estate and the market itself, I have always felt that there is a seriously Sisyphean element to what we do. My colleagues certainly don’t want to hear this from me, but it doesn’t stop me from mentioning it at least five, six or eighty times a year…

With the holidays just around the corner, the real estate market is entering that strange time of year when market participants begin to behave erratically.

Just last night, Matthew made an offer on a house priced at $1,100,000 that had been on the market for a month. He and the buyers submitted an offer of $1,070,000. The seller signed it back for $1,250,000.

That made absolutely no sense.

But maybe this isn’t so just now a December thing. Maybe this is the story of 2025? We will discuss this in our end of year posts in the coming weeks.

Many of the buyers out there now are looking for deals, and many of the sellers are trying to decide if they want to get a discount to move their property before the end of the year, or if they want to “try again” in 2026.

The fall was a lot slower than people thought it would be, although, in retrospect, I think there are dozens of people ready to say a massive “I told you so.”

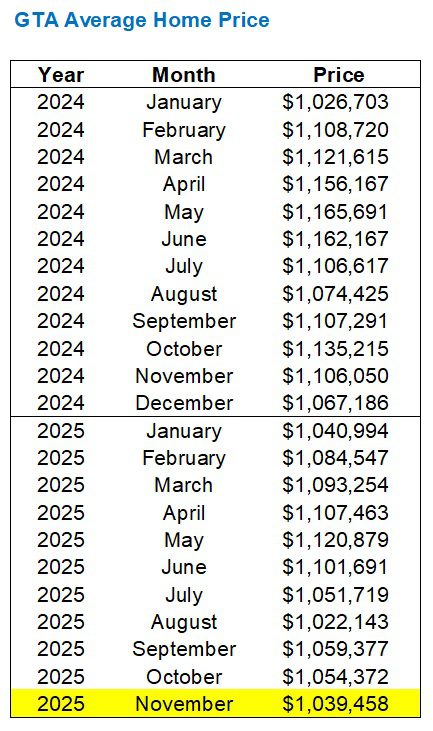

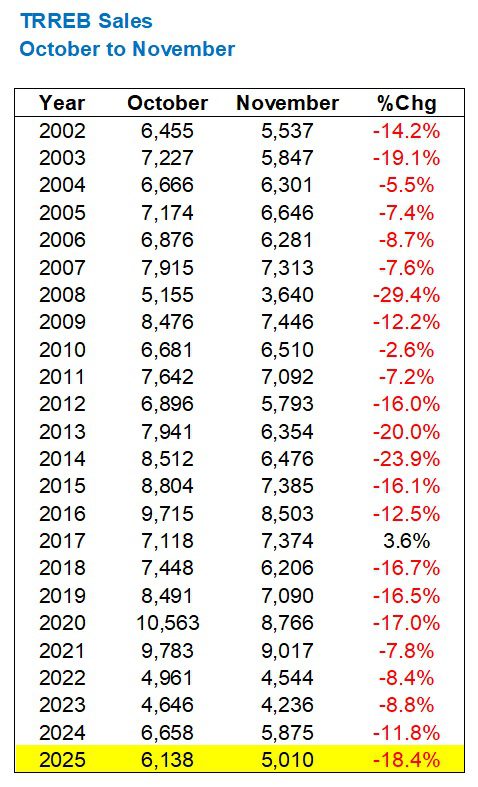

The November TRREB stats were released on Wednesday and they lined up exactly as I thought they would.

The average home price in the GTA rejected from October to November, now checking in for a modest $1,039,458:

That is low. Really low. Lower than I thought possible when we started the year in January with $1,040,994.

January!

The beginning of the year! The boulder at the bottom of the mountain, just beginning its journey to the top!

Obviously this is one average of many different property types, in different price ranges and in different geographical locations.

We will shortly look at how prices have developed in different TRREB districts.

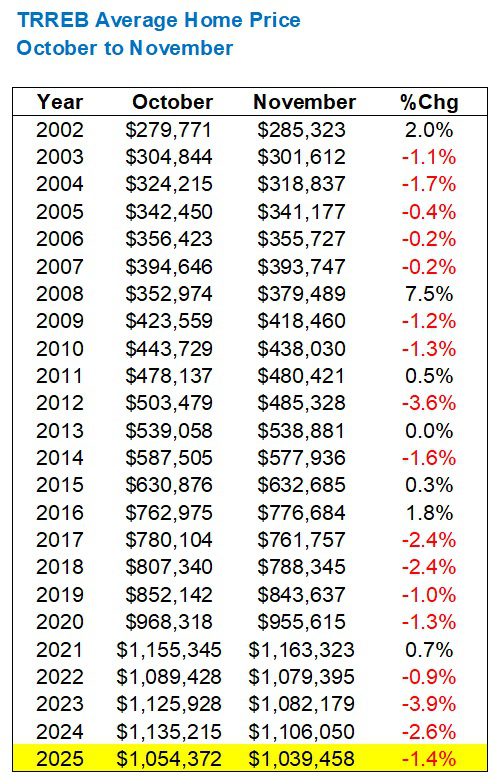

But for now, let’s take a look at that 1.4% month-on-month drop and see if it’s representative of what “usually” happens at this time of year, or if it’s ahead or behind…

The trend certainly shows us that the average house price is currently falling every year.

In fact, in the last twenty-three years we have only seen an increase from October to November six times.

Compared to 2023 and 2024, the decline was not as steep, but looking from 2017, where the average movement is -1.7%, it seems that the past month is completely in line with the movement of the past eight years.

On an annual basis, the average house price has fallen by 6.0%, which is significant!

Not as significant as the whopping 7.1% we saw in October, but more than the trend of the previous six months, which was around 4.6%:

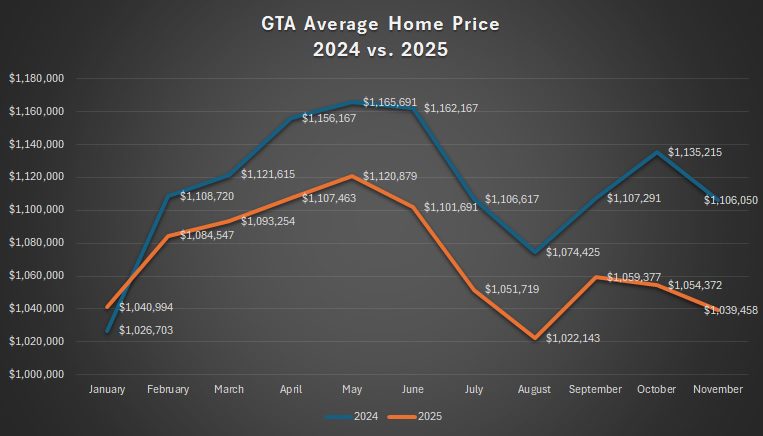

From the graph below we can see how the year started in January, with a year-over-year increase, and how the gap between 2024 and 2025 really started to widen this fall:

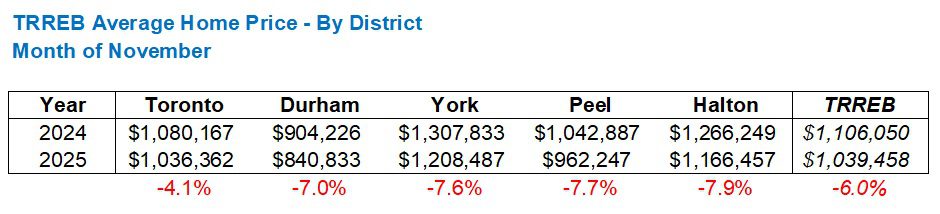

As noted above, averages are made up of other averages!

So let’s see how the average annualized TRREB decline of 6.0% summarizes when divided into the five largest TRREB districts:

This is kind of as expected, right?

The 416 will lead the 905 in a period of decline, especially after the 905’s gains during the 2020 pandemic were so pronounced.

In terms of salewe reached a period in the spring when every month the lowest turnover ever in that month, but that changed in the fall.

We saw the fourth-the lowest sales this millennium in September and the fourth lowest in October.

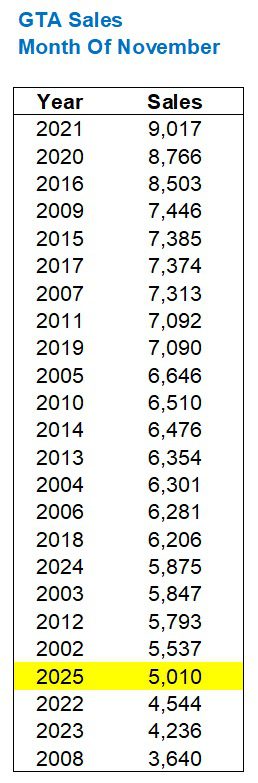

November did not break the trend:

In fourth place, again.

But this is after seeing the lowest in February, March, April and May (eliminating the 2020 pandemic market), and the second lowest in June.

Sales fell by 18.4% from October to November.

That’s the largest decline over that period since 2014, as shown in the following graph:

Maybe we are splitting hairs. Maybe we want to be bearish.

Suffice to say, sales are down each October to November without exception. Well, except for 2017, which is…

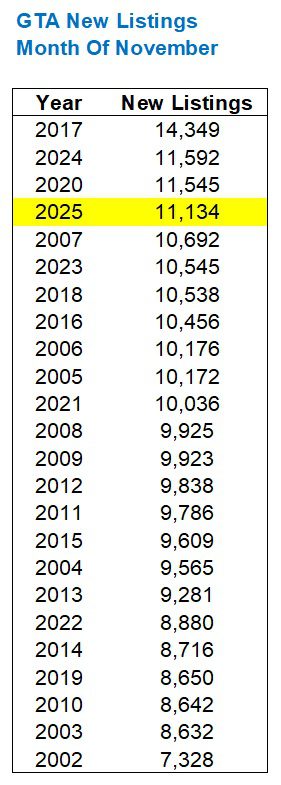

The number of new listings fell from 19,260 in September to 16,069 in October and to 11,134 in November.

These 11,134 new listings are still the fourth highest in any month of November:

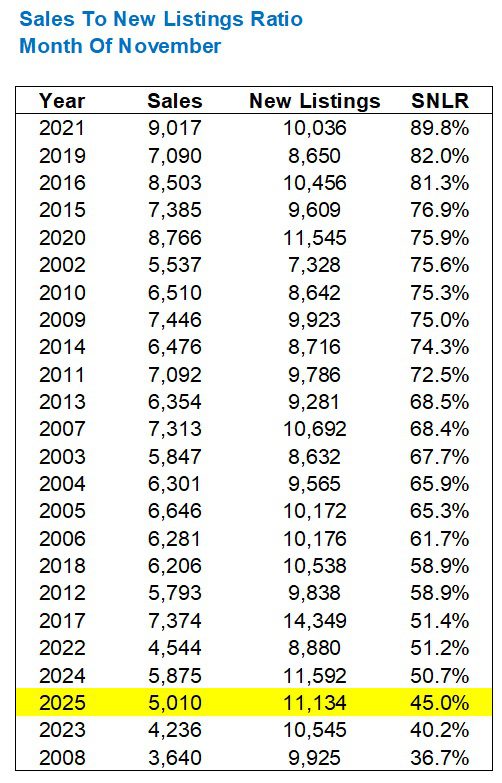

The number of listings has declined year over year, but so have the sales.

However, revenue fell 14.7% year over year, and new listings fell only 4.0%.

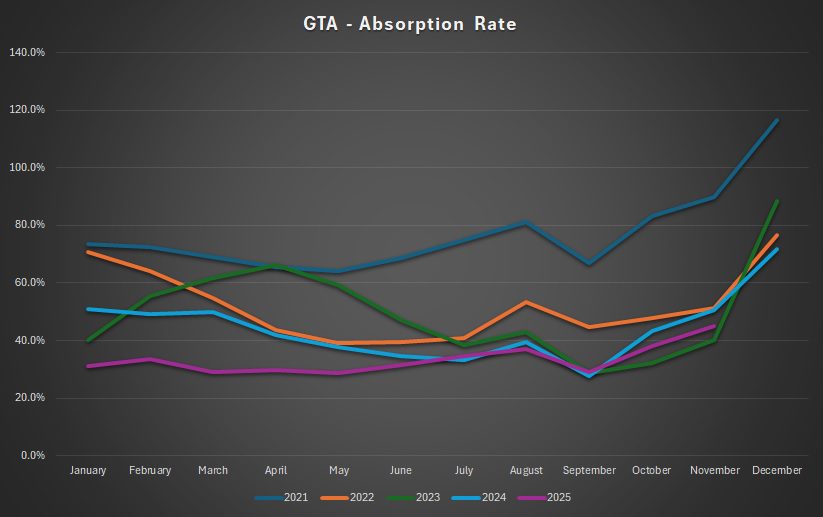

This means that the absorption rate in 2025 will be lower than in 2024, which the following graph confirms:

It’s pretty wild to think of a time when the absorption rate was 89.8%, right?

That was the market in the autumn of 2020.

Demand was at an all-time high, and supply wasn’t quite at an all-time low, but there wasn’t exactly a glut.

Looking at the bottom from this graph we can see 2008, 2017, 2022, 2023, 2024 and 2025.

2008: Global financial crisis.

2017: reaching the twenty-year peak.

From 2022 onwards: the post-COVID peak disappears.

Regarding the absorption rate in 2025, November’s 45.0% represents the annual peak:

Reason for optimism, right?

Except that, as the following chart shows, the absorption rate is currently increasing every year:

You may wonder why the absorption rate peaks in November and December each year, but it is a function of how the number of new listings drops significantly. Sales are also declining, but not nearly at the same rate as the number of new listings, which is why we’re seeing the ratio spike.

Back to sales for a moment.

Throughout 2025, I predicted that this year would be “the lowest sales ever.”

We reached a record with a record number of 122,133 sales in 2021low with 66,315 in 2023.

2024 was not much better at 67,984.

However, we are now on track to set a new record low in 2025:

That estimate is based on the turnover ratio from January to November.

However, we only saw 3,444 sales in December 2023 and 3,359 in December 2024. If we were to take the higher of these numbers and add it to the 59,034 sales so far in 2025, we would end the year with just 62,478.

Either way, we’re going to hit that record low.

And then, when the year is over, we’ll watch our boulder roll all the way back to the bottom of the hill, and we’ll push it up again in January.

Is it just me or was this the most this year tiring years since the pandemic?

Have a nice weekend, folks!

#November #TRREB #Stats #Fight #Toronto #Realty #Blog