Markets at a crossroads

Goldman Sachs Research represents one of the largest brokerage firms in the world. So it should come as no surprise that the investment bank recently released its stock market outlook for the next decade, predicting average annual returns of almost eight percent.

But if you’ve become accustomed to smooth and steady profits, you may need to adjust your expectations, despite reassurances from Goldman Sachs.

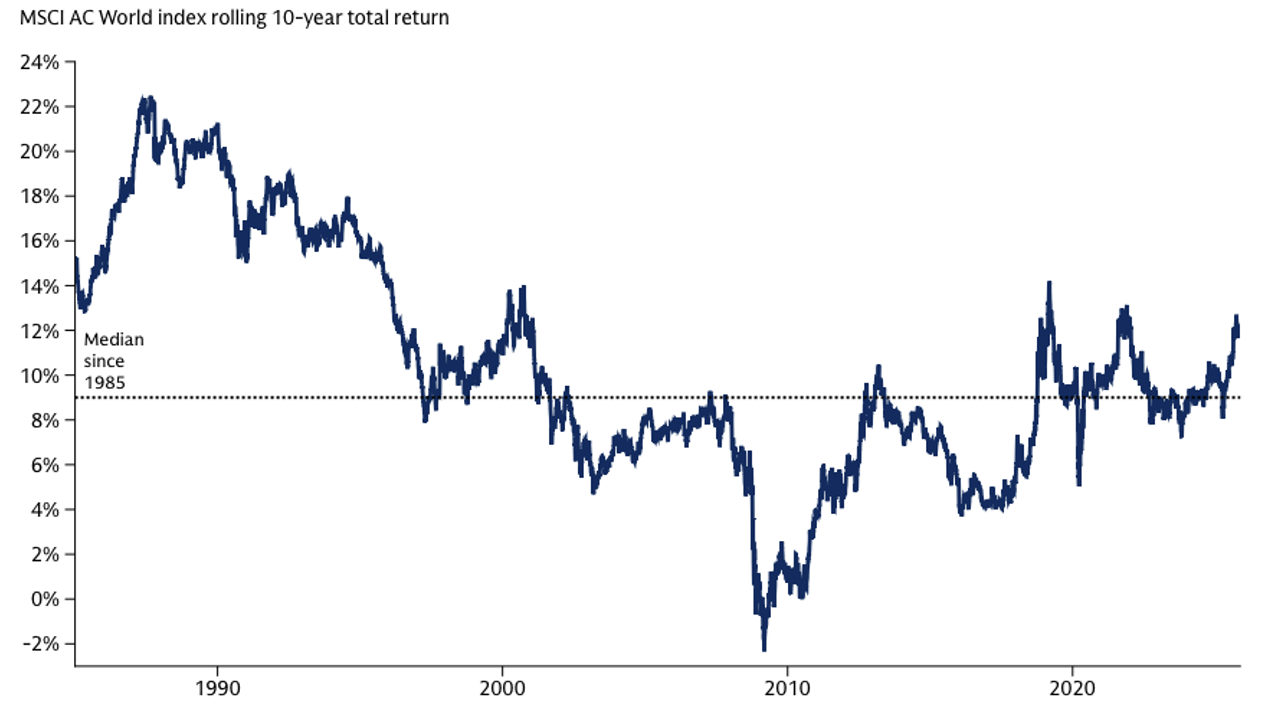

In its November report, Goldman Sachs paints a picture of a “new normal” for global equities, predicting annualized returns of 7.7 percent over the next decade. The estimate roughly matches the average return since the turn of the century, but Goldmans claims this represents a marked decline from the “heady” long-term average of 9.3 percent since 1985.

Figure 1. Recent returns have been high compared to the historical median

Source: Datastream, Goldman Sachs Research as of November 18

The core of Goldman Sachs’ thesis is that the era of valuation expansion is over. For years, falling interest rates and rising optimism meant investors paid more for every dollar of profit.

With global stock valuations at about 19 times forward earnings (our estimate for the US S&P 500 is almost 22 times), the price-to-earnings ratio tailwind is turning into a headwind.

The bank expects valuation ratios to contract slightly over the next decade, which will negatively impact performance. Consequently, the heavy lifting is expected to be done by the fundamentals: earnings growth and dividends. The report forecasts earnings to be around 6 percent annually, with dividends bridging the gap to reach the 7.7 percent target.

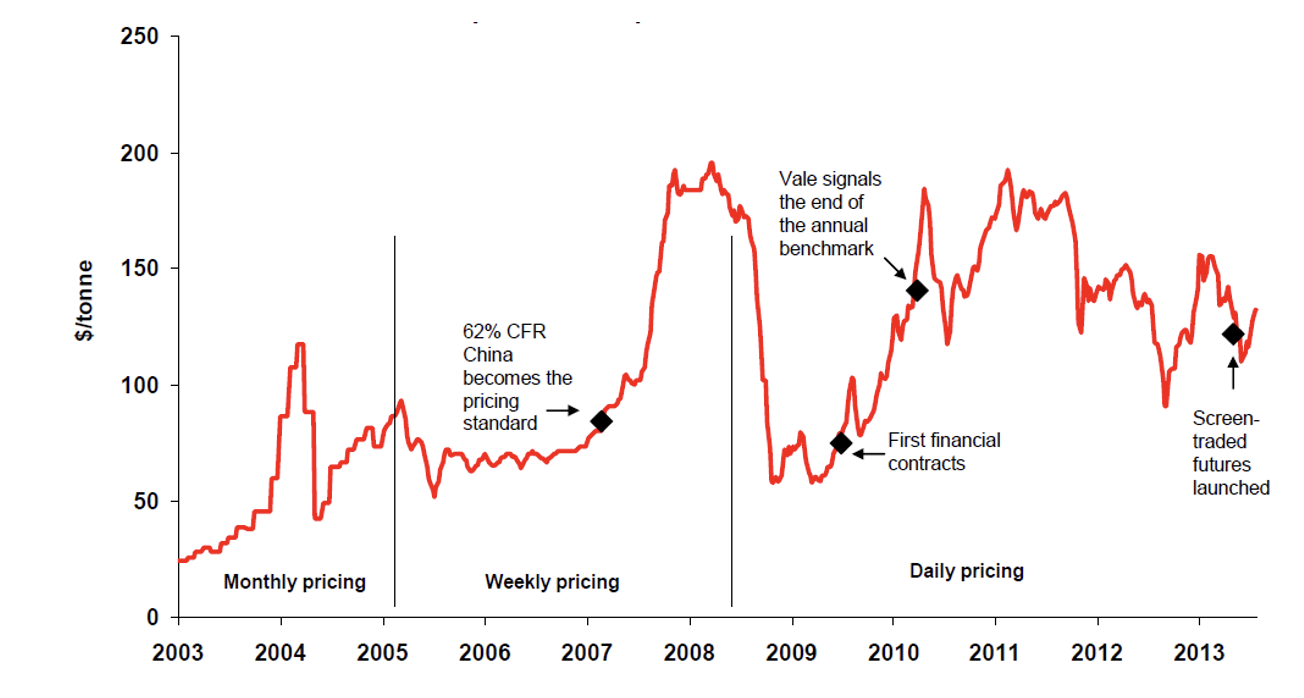

One observation about major investment banks’ forecasts is that they tend to subscribe to the idea that sentiment changes slowly and smoothly. Consequently, their price predictions tend to be smooth and gradual. By way of example, in 2011, amid oversupply forecasts, major investment banks predicted a slow, steady decline in iron ore prices. However, as Figure 2 shows, the spot price for iron ore has fallen by more than 50 percent in less than two years. Price movements, and especially declines, are more violent than smooth.

Figure 2. Iron ore spot prices – 62 percent cost and freight (CFR) China

Source: CRU, Platts, Macquarie Research August 2013

The idea that price-to-earnings ratios, which are a measure of the stock market’s popularity, will shrink slowly and smoothly over time does not come from experience.

Figure 3. One-year forward price-to-earnings ratio, S&P 500 (weekly).

As Figure 3 shows, price-to-earnings (P/E) ratios can fluctuate wildly in a relatively short period of time.

Goldman Sachs’ dependence on earnings growth is putting heavy pressure on corporate profitability, and widely accepted market valuation models, such as Robert Shiller’s Cyclically Adjusted Price-to-Earnings (CAPE) ratio, suggest annual returns could fall below 5 percent over the next decade.

This time it’s different (oh-oh)

However, Goldman Sachs states that these models are ‘incomplete’. Instead, in an observation reminiscent of Irving Fisher’s October 1929 statement that the stock market had reached a “permanently high plateau” just days before the Black Tuesday crash that ushered in the Great Depression, Goldman Sachs claims that the structure of the modern market has changed, with technology-driven efficiency gains and higher-margin companies justifying permanently higher valuations.

Perhaps the most useful advice is that, after years of American exceptionalism, the next decade will promote broad diversification into emerging markets. This vision relies on two crucial levers: faster economic growth in developing countries and a weakening US dollar. The bank’s currency team predicts a depreciation of the dollar over the next 12 months, which would mathematically increase the return on foreign assets when converted back into dollars.

The second observation about Goldman’s forecast for stock market returns is that it may underestimate the impact of the S&P 500 on the rest of the world’s markets. And the S&P 500 is expensive.

Figure 4. Forward price-to-earnings ratio of the S&P 500 versus subsequent 10-year annualized returns.

Source: Bloomberg, Apollo’s chief economist

Figure 4. establishes a relationship that we all know intrinsically; the higher the price you pay, the lower your return. As price-to-earnings ratios rise (right, along the X-axis), annual returns over the subsequent decade (Y-axis) fall.

According to Torsten Slock of Apollo Global Management, the current P/E ratio of around 22.25 in the S&P 500 predicts an average annual return of the S&P 500 over the next ten years of less than zero (red dot in Figure 4).

And since shifts in sentiment are rarely smooth, investors should expect periods of severe volatility and sell-offs that will contribute to that “average” negative return over the next decade. Even Goldman Sachs predicts lower price-earnings ratios.

Ultimately, Goldman Sachs predicts a “soft landing” on the stock markets. They ignore the repeatedly violent shifts in past sentiment and reject the bearish view that high prices will end in a crash. Instead, they propose that the smoothly eroding sentiment will be evenly and equally smoothly offset by earnings growth.

Whatever path sentiment, and therefore markets, take, the era of ‘free money’ of growing multiples is likely behind us.

Check out our previous blog posts with suggestions for rebalancing portfolios here: From Bullish to Cautious – Why 2026 May Bring Lower Returns and Higher Volatility, and here: Digital Income Class – October 2025 Performance Update.

He is also the author of the best-selling investing guide to the stock market, Value.able – how to value and buy the best stocks for less than they are worth.

Roger regularly appears on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The main purpose of this message is to provide factual information and not advice about financial products. Furthermore, the information provided is not intended as a recommendation or opinion about any financial product. However, any comments and statements of opinion should contain general advice only, prepared without taking into account your personal objectives, financial circumstances or needs. Therefore, before acting on any information provided, you should always consider its suitability in the light of your personal objectives, financial circumstances and needs and, if necessary, seek independent advice from a financial advisor before making any decision. Personal advice is expressly excluded in this message.

#Markets #crossroads