International dividend tax for expats refers to the taxes imposed on dividend income earned from foreign investments while living in another country.

It usually includes dividend tax in the source country and possible additional tax in the country of the expat’s tax residence.

This article covers:

- How are foreign dividends taxed?

- Do I have to pay tax on foreign dividends?

- Is there withholding tax on foreign dividends?

- Is there double taxation on dividends?

Key Takeaways:

- Foreign dividends are often taxed at source before you receive them.

- Your tax residence usually determines whether additional tax is due.

- Tax treaties can significantly reduce or eliminate double taxation.

- Good investment and residence planning can legally reduce dividend tax.

My contact details are hello@adamfayed.com and WhatsApp +44-7393-450-837 if you have any questions.

The information in this article is intended as general guidance only. It does not constitute financial, legal or tax advice, and is not a recommendation or invitation to invest. Some facts may have changed since the time of writing.

What exactly is dividend tax?

A dividend tax is a tax on income received when a company distributes profits to its shareholders.

Dividends are commonly paid by publicly traded stocks, exchange-traded funds (ETFs), mutual funds, and real estate investment trusts (REITs).

Dividend tax applies to the cash or equivalent value received by the investor and is calculated separately from capital gains.

The applicable tax rate and treatment will vary based on the tax rules applicable to dividend income in the relevant jurisdiction.

What is a preferential rate?

A preferential rate is a lower tax rate applied to certain types of dividend income instead of the standard ordinary income rate.

Many countries offer preferential rates for qualified dividends or dividends that meet specific criteria, such as paid out by publicly traded companies, held for a minimum period or sourced from certain jurisdictions.

For expats, dividends taxed at a preferential rate can significantly reduce overall tax liability compared to regular income tax.

What is original income?

Ordinary income refers to dividends that are taxed at the same rate as regular income, such as salaries, corporate profits or interest income.

These dividends are not eligible for special reduced rates and are generally subject to the full progressive tax rates of the country of tax residence.

Classifying dividends as ordinary income may result in a higher tax burden compared to preferentially taxed dividends.

Who is exempt from dividend tax?

Investors are exempt from dividend tax if their income, residence status or investment structure falls under specific legal exemptions.

Exemptions from dividend tax may apply to:

- Investors whose income is below taxable thresholds

- Residents of territorial tax countries that do not tax foreign dividends

- Dividends held in qualified retirement or retirement accounts

- Investors protected by favorable provisions in tax treaties

How are international dividends taxed?

International dividends are generally taxed by both the country where the dividend originates and the country where the investor is resident for tax purposes.

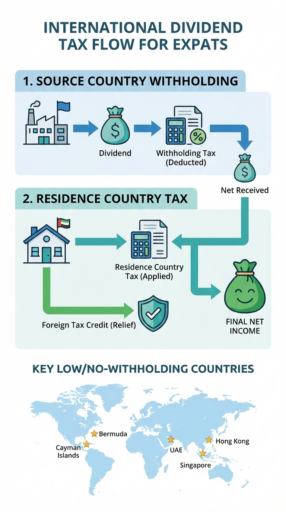

1. Taxation from the source country

The country where the company, fund or ETF is incorporated usually taxes dividends at the time of payment.

This tax is automatically applied as a withholding tax, meaning it is deducted before the dividend reaches the investor.

Withholding tax rates vary widely from country to country and are often reduced if a tax treaty exists between the source country and the investor’s country of residence.

2. Tax in the country of residence

Your country of tax residence may also tax dividend income as part of your worldwide income, even if tax has already been withheld at source.

This second layer of tax depends on local tax laws and how dividends are classified (ordinary income versus preferential rates).

To avoid double taxation, many countries allow foreign tax credits, exemptions or exclusions, provided that dividend income is properly reported.

Most countries rely on double tax treaties to coordinate these two layers of taxation so that dividends are not taxed twice at the full rate, while still preserving each country’s tax rights.

What is the tax rate for foreign dividends?

Withholding tax rates alone can range from 0% to around 44% before the treaty exemption, and even after the treaties are applied many rates are still between roughly 5% and 15%.

The tax on foreign dividends often varies widely.

Examples of withholding taxes in source countries

Different countries impose different standard withholding tax rates on dividends paid to non-residents before any treaty reduction:

- United Kingdom: often 0% (no withholding tax)

- Greece: about 5%

- Ireland: about 25%

- Switzerland: about 35%

- Many legal areas: typically ~10%–20%

- On the high side: in some places the usual range may be exceeded (e.g. up to ~44% in specific jurisdictions) before treaty relief

Tax treaties between countries often reduce these standard rates for residents of treaty partners to lower levels, typically between 5% and 15%, if you submit the appropriate documentation.

Dividend tax and settlements in country of residence

Even after withholding tax, your country of tax residence may tax the same dividend as part of your worldwide income, with rates depending on local law.

Many jurisdictions grant foreign tax credits for withholding taxes paid abroad, which can offset or eliminate the additional occupancy tax liability.

Because both withholding and residence taxes may apply, expats may end up paying only one, the other, or both taxes, reducing the overall burden.

How to legally avoid dividend tax

You can reduce dividend tax by investing in treaty-friendly countries or by using accumulation funds that reinvest dividends instead of paying them out.

Strategies include:

Tax avoidance is illegal, but legally minimizing taxes through planning, use of treaties and investment structuring is a legal and widely accepted part of professional asset management.

Which countries do not have withholding tax on dividends?

Singapore is among the list of countries that do not impose withholding tax on dividends paid to foreign investors.

Other countries included are:

- Hong-Kong

- United Arab Emirates

- Cayman Islands

- Bermuda

- Bahrain

But even if the source country does not withhold taxes, your country of tax residence may still tax the dividends according to local rules.

Dividend tax versus capital gains tax for expats

For expats, dividends are generally taxed when received, while capital gains are only taxed when the underlying assets are sold.

The main differences include:

- Dividends taxed immediately: Most countries consider dividend income to be taxable in the year it is paid, even if the money is reinvested.

- Capital gains taxed upon realization: Taxes on the gain from asset sales generally apply only when the investment is sold, and not as it grows.

- Rates often differ: Many jurisdictions tax dividends at higher rates than long-term capital gains, making growth-oriented investments (such as accumulation ETFs) more tax efficient for expats.

- Possible exemptions: Some countries fully exempt capital gains on foreign assets, providing additional tax planning opportunities.

Conclusion

International dividend tax can feel complex, but it also offers opportunities.

By understanding how different countries tax dividends, using treaties wisely, and strategically structuring investments, expats can turn cross-border challenges into advantages.

Ultimately, the key is not just minimizing taxes, but tailoring your investment strategy to your lifestyle and residency choices, creating a system where your wealth grows efficiently across borders.

Frequently asked questions

Are American expats double taxed?

Yes, US expats are taxed on their worldwide income, including dividends, but foreign tax breaks and tax treaties usually prevent them from paying taxes twice.

Are US dividends taxable to non-residents?

Yes. U.S. dividends are generally taxable to nonresidents through withholding taxes, typically at 30%, unless reduced by a tax treaty.

Do expats pay capital gains tax?

Expats pay capital gains tax if their tax residence tax country makes profits worldwide; some countries only tax local profits, while others do not tax capital gains at all.

How to declare foreign dividend income?

To report foreign dividend income, report it on your annual tax return in your country of tax residence, provide documentation of any withholding taxes paid abroad, and complete any required foreign income schedules or disclosures.

Make sure all dividends are included to avoid penalties, even if taxes have already been withheld in the source country.

Tormented by financial indecision?

Adam is an internationally recognized financial author with over 830 million answer views on Quora, a best-selling book on Amazon, and a contributor to Forbes.

#International #dividend #tax #expats #rates #strategies