What is an I-bond?

The U.S. government offers two types of savings bonds: EE Bonds (nominal) and I Bonds (inflation-adjusted). You buy them both directly from the government TreasuryDirect website. I-bonds are a type of inflation-indexed bond, somewhat similar to TIPS. But you can never lose principal on them, you don’t get phantom income from them, and you don’t pay taxes on them until you sell them. Like EE bonds, you must own them for at least one year and give up three months’ interest if you sell them after an ownership period of less than five years.

You can hold the bond for a maximum of 30 years. I-bonds have two components to their returns: a fixed interest rate and an inflation adjustment linked to the Urban Consumer Price Index (CPI-U). So when inflation was high in 2022-2023, I-bonds looked particularly attractive as investments. At one point they paid over 9% risk-free while the shares plummeted. FOMO kicked in and we decided to complicate our financial lives to earn 9% on a very small portion of our portfolio.

More information here:

I Bonds and TIPS: which inflation-indexed bond should you buy now?

Why are you selling your I-bonds?

I Bonds sound pretty great, right? Why would anyone want to sell them?

The biggest problem with I Bonds is that you can only buy $10,000 of them per year. That’s fine if you have a relatively small portfolio and start investing in it early each year. After twenty years, you could have something in the neighborhood of a $250,000 portfolio. But they just don’t work as well in larger portfolios. The restriction is actually per person or entity, which means that you and your spouse and your trusts and your corporations can each purchase $10,000 worth of I-bonds each year. We have done this for a number of years starting in 2021.

But you must manage a separate account for each entity. And even when you add it all up, it still wasn’t enough money to move things around for us, so we decided to simplify. By dumping I-bonds and transferring the handful of individual TIPS owned by one of the TreasuryDirect accounts, we were able to close three financial accounts. The good news is that dumping the I bonds is MUCH easier and faster than transferring the TIPS to our Vanguard brokerage account. It took less than five minutes total to sell all the I-bonds in three different accounts. We simply move that money into the TIPS ETF (SCHP) that we use to balance the portfolio.

Note that there is a relatively new method to purchase “unlimited” I-bonds (via a gift box), but it initially seemed to me that you can still only deliver $10,000 a year to a recipient. It would still take 30 years to deliver $300,000 worth of I-Bonds to your spouse, even if you could buy them all in advance. And since they only last 30 years, it’s clearly not unlimited, even if it does make I Bonds a slightly better option for some people.

However, in further correspondence with a WCI member, he informed me that, at least at this time, there is no annual limit on the number of I-bonds that can be delivered in a year, although you can only deliver $10,000 per day. I asked him to submit a guest post about it. If you read more about the Frequently asked questions about TreasuryDirect gift boxesThere are a few other issues to consider, but it appears that you can now purchase an unlimited number of I-bonds through this loophole. I wouldn’t be surprised if it’s close, and we’re still happy to delete three accounts from our lives, even though there’s apparently a solution to the main reason we’re dumping these I-bonds. But this could certainly change the calculus for others, at least as long as this loophole remains open. Hopefully it will just be expanded instead of closed.

How to sell your I bonds

Log into your TreasuryDirect account using your username, the “OTP” emailed to you, and your password. Your screen should look like this.

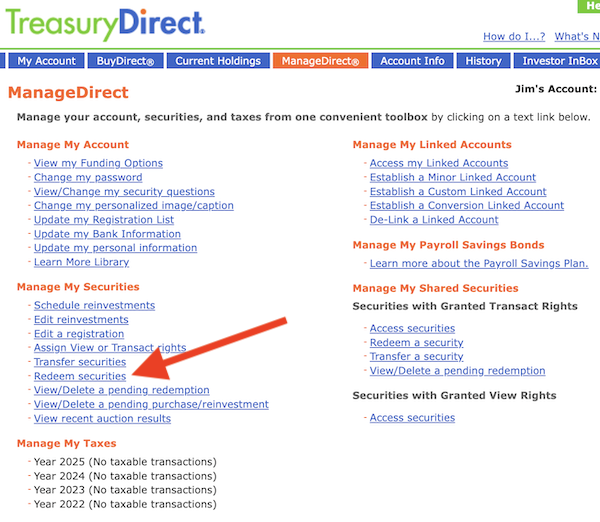

Click on the “ManageDirect” link and you will arrive at this screen:

Click on ‘Redeem Securities’ and it will take you here:

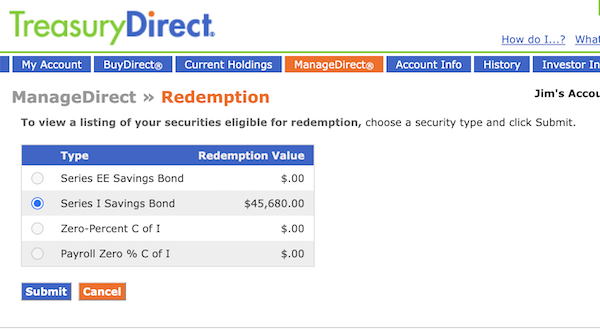

Click on what you want to sell (in this case the I-Bonds, which are all owned by this account) and click “Submit” and it will take you here:

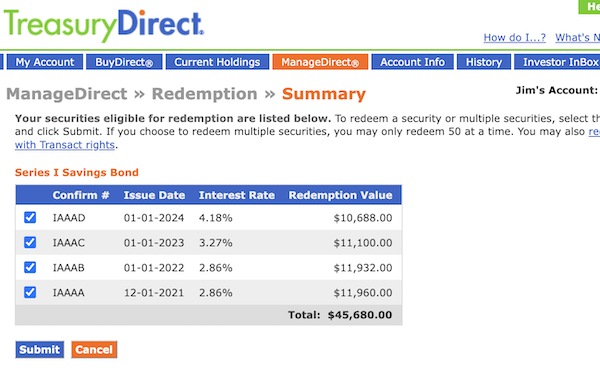

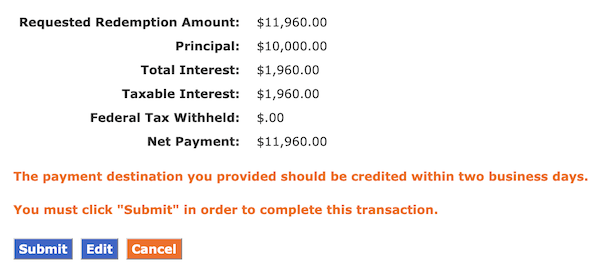

Click on the products you want to sell (all of them in my case) and click ‘Send’. You will then get a large, long page, the bottom of which looks like this.

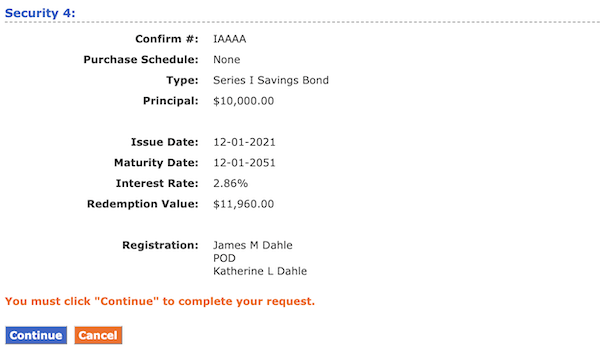

Hit ‘Continue’ and you’ll get a similar page, the bottom of which looks like this:

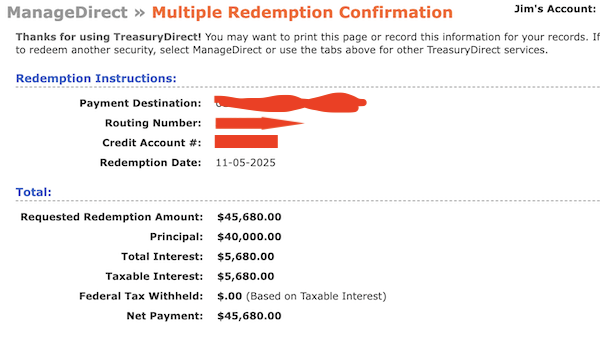

And you click ‘Send’. Voila, your I-bonds have been sold, at least the ones in this account. The confirmation page states that the money will be in your linked bank account within two business days.

Easy peasy. Despite all the complaints you hear about dealing with TreasuryDirect, this may be the easiest thing I’ve ever done there. I cleared three accounts in less than five minutes. I’m sure it will take months to transfer those individual TIPS to Vanguard (it took almost a week just to get the Medallion Signature Guarantee needed for the paperwork). I think the alternative is to keep the TreasuryDirect account we have until they all mature over the next five to ten years, but I’d rather work on it now to avoid ever having to log into TreasuryDirect again to check them.

More information here:

How to pass on bonds to heirs

How did we do with I-bonds?

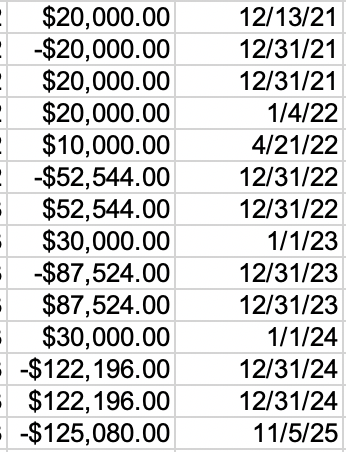

We have now gone back and forth with our I Bond investments. Here are the details from the investment spreadsheet:

We started buying them four years ago, bought a few more every January, and sold them all after owning them for more than a year but less than five years (so we lost three months’ interest on each one). We didn’t pay taxes on the income as it grew, but now that we’ve sold, we owe federal income taxes at ordinary income tax rates.

Our total profit was $15,080, which equates to an annualized return of 4.32% before taxes. After applying our marginal tax rate of 37% + 3.8% = 40.8%, we earned $8,927.36, an after-tax return of 2.62% per year. Considering that annualized inflation during that period was 4.18%, it’s a little hard to get super excited about that return. Especially when you compare it to US stocks with high growth during that period. However, I am excited to get rid of three accounts.

What do you think? Do you have questions about the process? Do you keep your I Bonds, or do you want to sell them?

#sell #bonds #White #coat #investor