Error, small talk entry not found

On April 9 last year, Donald Trump postponed his Liberation Day tariffs, fueling a stock market rally led by optimism in the field of artificial intelligence (AI). That optimism turned to fear this year, as joy over AI’s productivity improvements turned to panic about how many businesses it would destroy.

That panic reached an even more urgent level last week, when James van Geelen, a thematic investor and former entrepreneur who founded a healthcare company before delving into investment research at Substack, hypothesized that AI would devastate the entire global consumer economy, rendering generations of white-collar workers redundant.

Shares of software companies have plummeted since Anthropic began adapting its Large Language Models (LLMs) to code better versions of their software. As one analyst noted, “If code can write code, who needs programmers?” That fear spread to the stock prices of real estate companies, cybersecurity companies, IT services and outsourcing companies, as well as financial services and asset management companies.

And anyone who’s seen the shorts made over the past week with a clue or two about graphics AI tools from China’s DeepSeek must also be wondering what’s happening to the jobs of the hundreds of VFX engineers and artists who typically fill the credits of modern action and fantasy films.

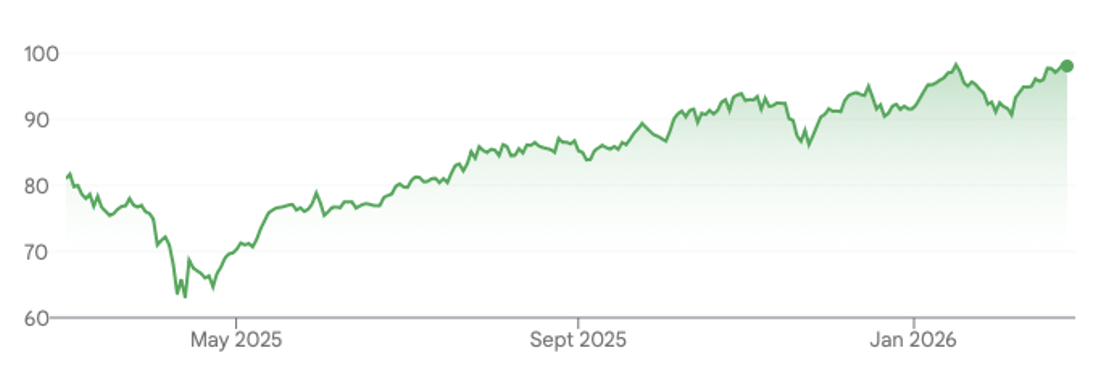

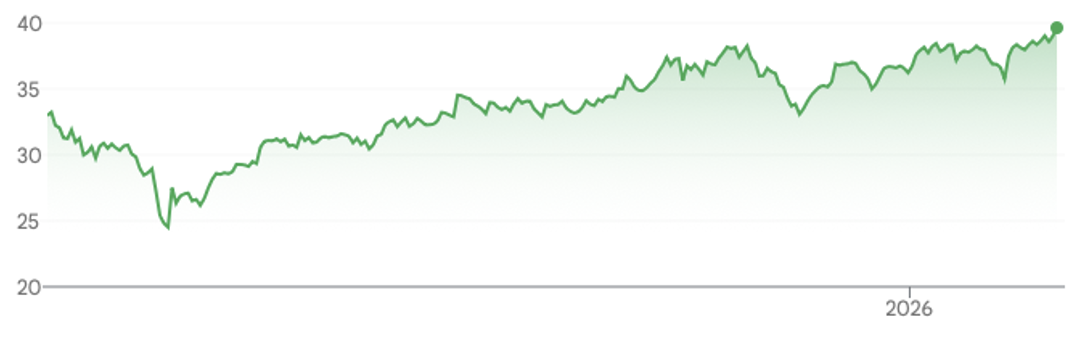

One sector that still seems optimistic is robotics. As Figure 1 and Figure 2 illustrate, some of the optimism previously prevalent in the AI and software theme appears to have migrated to robotics.

Figure 1. Global X Robo Global Robotics & Automation ETF (ASX: ROBO) 1 year.

Source: Google Finance

But here again there is a range of views on how humanity will benefit from robots, be destroyed by them, or experience neither benefit nor loss.

Figure 2. Global X Robotics and Artificial Intelligence ETF (NASDAQ: BOTZ) 1 year.

Source: Google Finance

But despite the optimism, there is also a debate about the future adoption and usability of humanoid robots.

On one side are the “Engineering Realists,” led by pioneers like Rodney Brooks, who worked in robotics for fifty years and decades as an MIT Robotic Professor and at Rethink Robotics. On the other side are the ‘Embody AI’ optimists like James van Geelen of Citrini Research, who believe we have arrived at the ‘GhatGPT tipping point for AI-powered autonomous humanoids.

While both agree that robots are a matter of ‘when’ rather than ‘if’, they differ greatly on the ‘how’ and ‘how fast’. And the answers to these questions will determine whether the BOTZ and ROBO ETFs remain at record highs.

By way of example, Citrini Research argues that Vision-Language-Action (VLA) models, such as NVIDIA’s GR00T, have finally given robots a “brain worth battery power,” allowing them to learn tasks like washing dishes in a week. However, Brooks argues that this is a fundamental misunderstanding in physics, with the prediction that ‘deployable agility’ will remain ‘pathetic’ until at least 2036. He argues that current machine learning is “collecting the wrong data” and cannot solve the deep mechanical problems of force sensing and materials.

Brooks sees a lack of progress on autonomy, while Citrini sees an opportunity for data collection that will accelerate learning of VLA models, pointing to the falling costs of hardware – particularly Unitree’s $16,000 humanoid – as evidence suggests that robots are finally on a Moore’s Law cost curve. However, Brooks remains unimpressed by these low-cost units, noting that they are often too weak to provide, for example, the physical support needed for people-oriented tasks such as caring for the elderly or disabled.

I think the two views clash most sharply on the humanoid design. Citrini sees the humanoid form as essential because our world is “ergonomically designed” for two arms and ten digits. Brooks, however, dismisses the “humanoid” form as marketing, suggesting that practical robots will be task-specific and will eventually develop forms of momentum and specialized appendages – superior to human forms – to become useful for those specific tasks.

As an example, Brooks points out that today’s bipeds are inherently unsafe; if they lose power, they don’t just stop, they fall over.

Meanwhile, another significant difference lies in the implementation strategy. Citrini Research highlights teleoperation (remote human operators taking over when robots fail) as a brilliant “bridge.” Brooks sees this same trend as a plan to roll out remote-controlled “dolls” rather than truly autonomous helpers, which could justify the current optimism in the stock market.

In terms of timelines, Citrini sees widespread use of humanoids in warehouses (such as Amazon’s Digit) and an eventual ‘consumer crossover’ within 3-4 years. Brooks considers the claim that robots will be in 10 percent of homes by 2030 historically unlikely, noting that no technology — not even the Internet or cell phones — has ever scaled up at that pace. He emphasizes that without new mechanical systems, these robots will remain too dangerous to be in close proximity to people.

After researching both sides of the debate, my opinion is as follows:

- In a rush to be first, the “offshore pilot” model is the most likely solution to the autonomy gap, allowing companies to immediately sell and deploy robots in structured environments such as warehouses and simple retail tasks without solving the artificial general intelligence – “AGI” or “dexterity” problems that Brooks identifies.

- As companies roll out humanoid forms, Brooks is probably right that cost and complexity will see functional usability trump aesthetics. We’ll likely see ‘humanoids’ with specialized grippers – holding arms for ‘ergonomic’ tasks, forgoing the unstable bipedal legs for safety and battery life.

- I have more sympathy for Brooks’ “pathetic agility” view, which warns that robots will likely prevent robots from entering the home (kitchen, laundry, child and elder care) for much longer than investors hope. The complexity of “multi-finger dexterity” in invisible environments remains a huge technical hurdle that “more data” may not solve.

Ultimately, investors should be careful not to lump robots into structured environments like BMW and Porsche factories, with the widespread adoption of Terminator-style humanoids everywhere, including at home and on the battlefield. The robotic ‘ChatGPT moment’ is real in the factory, where the environment is predictable. But I agree that we are probably still a long way from everyone owning and deploying a fully autonomous butler in their home.

*This article was written on February 26, 2026.

He is also the author of the best-selling investing guide to the stock market, Value.able – how to value and buy the best stocks for less than they are worth.

Roger regularly appears on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The main purpose of this message is to provide factual information and not advice about financial products. Furthermore, the information provided is not intended as a recommendation or opinion about any financial product. However, any comments and statements of opinion should contain general advice only, prepared without taking into account your personal objectives, financial circumstances or needs. Therefore, before acting on any information provided, you should always consider its suitability in the light of your personal objectives, financial circumstances and needs and, if necessary, seek independent advice from a financial advisor before making any decision. Personal advice is expressly excluded in this message.

#Error #small #talk #entry