For the article, view the last on my podcast, Personal finances for long -term investors:

Now, here is today’s article:

I had a nice e -mail dialog with listener Bethany About the pension situation of her parents, and she asked me:

Why do you usually recommend the higher delay in social security to 70? Is this just to guarantee the lifespan of their portfolio?

Great question!

Why do some financial planners suggest that in a couple the spouse with the more Social security benefits collect delay up to 70 years, while the spouse with the fewer Social security benefit starts to collect at the age of 62?

Here is the simple reason why the partner earns with a higher should have to (at least to consider) Postponing social security until the age of 70.

Mama, dad and the bigger advantage

An example will help. Let’s think about two people, Mommy And Pa.

Mother has a smaller advantage of social security.

Dad has a greater advantage of social security. Let’s say that Dad’s benefit is twice as large as that of mothers.

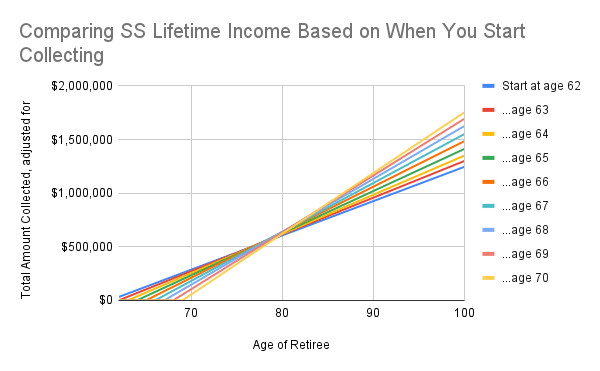

For both, regardless of their benefits, their “break-even” age around the age of 80. This article shows you how that works:

Because of easy figures, we will simply say that their break life is 80 years old. That means we only Consider their Own individual benefit**, they have to live beyond the age of 80 (their break life) to pick the benefits of postponing social security. When they die for Age 80, they would (in retrospect) prefer to collect social security in an earlier age.

**This is a crucial qualification that we will have to change later.

But we have to only consider their own individual advantages? No!

When a spouse dies, the surviving spouse may be eligible to inherit the social security benefit of the deceased spouse, so that the higher of the two benefits is received in the future.

In other words: there are essential scenarios true Mommy will receive Dad Greater social security benefits. Namely, when daddy dies first. In other words:

- The smaller advantage of mother will cease to exist in the death of the first husband. Always.

- The greater advantage of Dad will continue to live until the death of the second spouses. Always.

There are (4) possible scenarios …

1 – Mama and Dad both die for Age 80

2 – Mother dies for 80, daddy dies after 80

3 – Dad dies for 80, Mama dies after 80

4 – Both die after the age of 80.

In three of those four scenarios, at least one spouse lives above the age of 80. In 75% of the scenarios, daddy’s social security was delayed until the age of 70 the right decision for the family.

Why * would * not pursue this strategy?

Now, I am outgoing that all four of our “death scenarios” are just as likely; that the chances for each are 25%. It is clear that real life does not work that way. Every individual will have a unique and difficult to predict mortality.

That is why I like to ask questions about health history, etc. If both mom and dad are relatively unhealthy, and both have a long family history of early death, I could certainly see the reason for both spouses who gather early.

Health and Health History Are the main reasons why a few these kinds of claim strategy may not pursue.

Perhaps there may be more questions about the social security that generally claims. Kitces.com recently released a great line of thought about various factors and risks for social security, the conclusion of which is …

… is that most traditional social security research is too far biased to claim social security for Later agesAnd not enough to early ages. Some of the arguments in the article are very logical for me. Although I disagree with the most important argument (comparing social security “returns with that of a 60/40 portfolio).

Why would a few otherwise not be able to follow the strategy of today, where the lesser benefit of husband gathered early and the larger beneficial spouse delayed up to 70?

Immediate cash flow needs. Some couples now simply need the income for costs of living. In those cases, the theoretical lifelong-maximizing strategy takes a rear seat for financial reality.

Age crack between spouses. If the lower -earning husband is much younger, the surviving benefit may not come into play for decades. In that scenario, maximizing the higher benefit is less urgent and rather taking benefits can be more logical.

Tax considerations. Social security interacts with other income flows. This is important to consider.

Trust in other pension sources. If the couple already has considerable pensions, savings or guaranteed income flows, the Social Security Survivor benefit may not be that critical. They could rather collect and enjoy the income while they are younger and healthier.

Thank you for reading! Here are three fast notes for you:

First – If you liked this article, add to 1000’s subscribers who read the free weekly E -mail from Jesse, where he sends you links to the smartest financial content that I find online every week. 100% free, unsubscribed at any time.

Second – Jesse’s Podcast “Personal finances for long -term investors” has grown ~ 10 times in recent years and now helps ~ 10,000 people per month. Coordinate and view it.

Last -Jesse works full -time for a fiduciary asset management company in Upstate NY. Jesse and his colleagues help families to solve the expensive problems he writes about and podcasts about. Plan a free phone call with Jesse To see if you fit well with his practice.

We talk to you quickly!

#higher #earning #spouse #delay #social #security #interest