September 9, 2025

9:11 AM

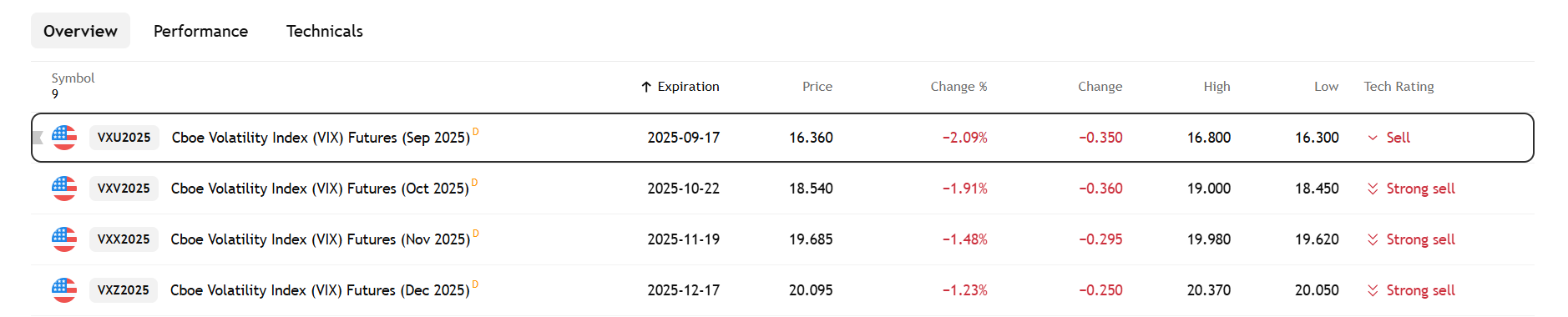

The Vix Futures deals of October are traded with an extreme premium compared to September Futures, which indicates the turbulence of the FED.

Risky devices can be confronted with more stormy conditions if the Federal Reserve lowers interest rates on 17 September, as expected. This message is broadcast by the VIX Index Futures, which measure the expected volatility of the S&P 500 index in the next 30 days.

The index, also known as the Wall Street Fear meter, is calculated in real time based on the S&P 500 option prices. It reflects how investors expect the market to swing, and higher values indicate greater uncertainty.

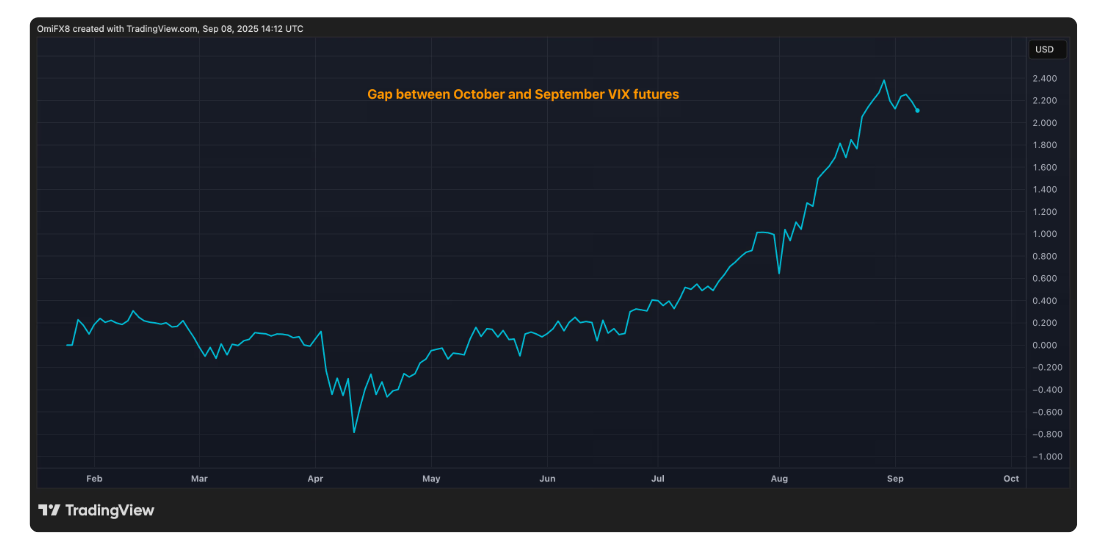

The difference between the VIX -Futures of October (contract for the following month) and the September transaction (contract for the previous month) increased to 2.09%, which is a historical level of extreme level, the HandelsView Data source according to. The September transaction is one day with the FED meeting. In the meantime, in the case of the ENAVI contract, they only exchange a small premium compared to the cash index. In other words, sellers have taken the risk before the FED session and bet that interest rates will keep the markets stable as the decision approaches.

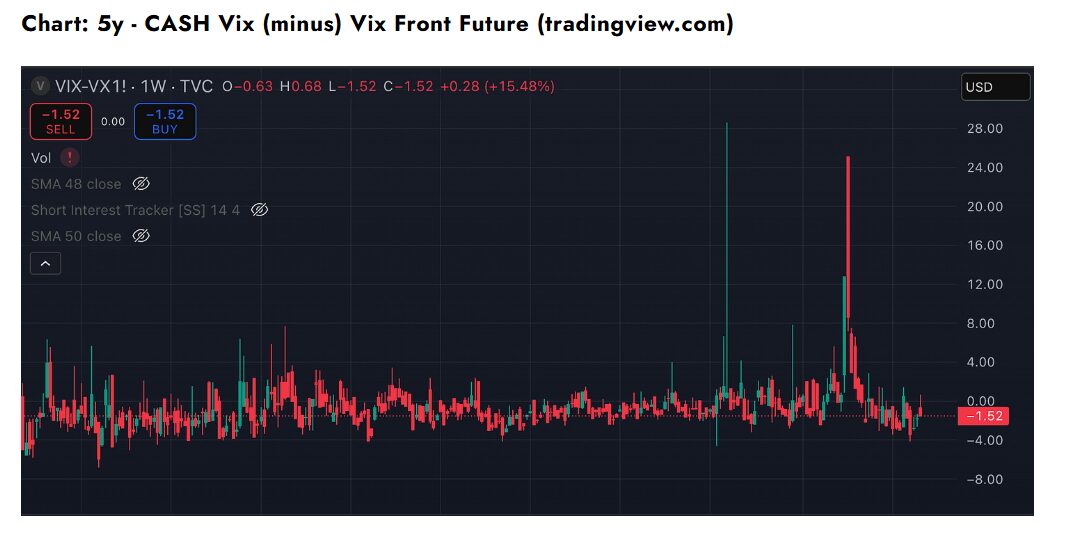

Cash Vix Pointer

According to CME Fedwatch, the US Central Bank is expected to reduce its target with at least 25 basis points during next week’s meeting. Some market participants expect a reduction of up to 50 basis points.

Dark stormy clouds gather in October

However, the Futures transactions of October show something else. These suggest that investors expect an increased turbulence after the FED decision is in force and the interest rates are priced.

“The September Vix Futures transactions have released the risk, while October can be ugly … I think this topic is worth keeping in mind for risky tools.” – wrote Vantini, the cryptoernivative data analysis company, Amberdata, the newest In their newsletter.

Difference between September and October Vix

Historically, VIX showed a strong negative correlation with stock prices, which generally rise during the periods of bear markets and market stress, while it dropped as stock prices rose. This means that the potential volatility growth can be characterized by a decrease in stock prices after the fed decision.

It is known that Bitcoin follows the atmosphere of Wall Street. This means that the explosion of shares can quickly spread to the cryptomarket. And, just like the shares, the turbulent period can be characterized by bear prices.

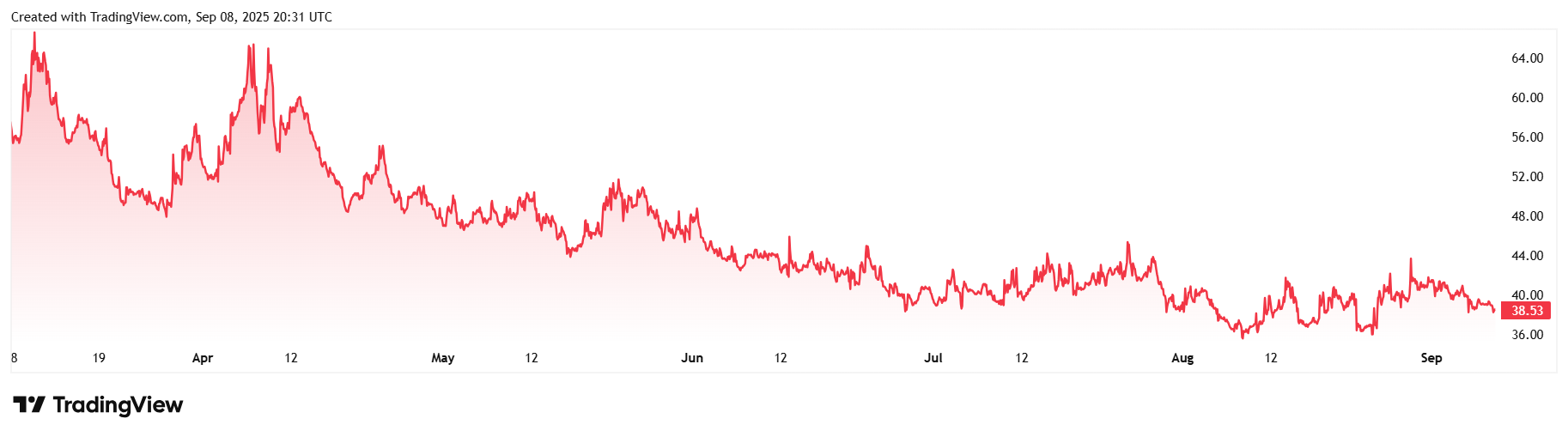

BVIV -Indexvolution in the past 6 months

Since November last year, the price of Bitcoin spot and the correlation between 30 -day implicit volatility indices have become negative. In addition, Bitcoin Volatility Indexes-BvIV and DVOL-HAVE recently reached record-high correlatiors levels with VIX, which Bitcoin emphasizes more and more consistent with broader market volatility trends of the market.

#Dark #clouds #gather #Bitcoin #interest #rate #reduction #Fed