close-up image of a man counting Indian currency istock photo for BL | Photo credit: iStockphoto

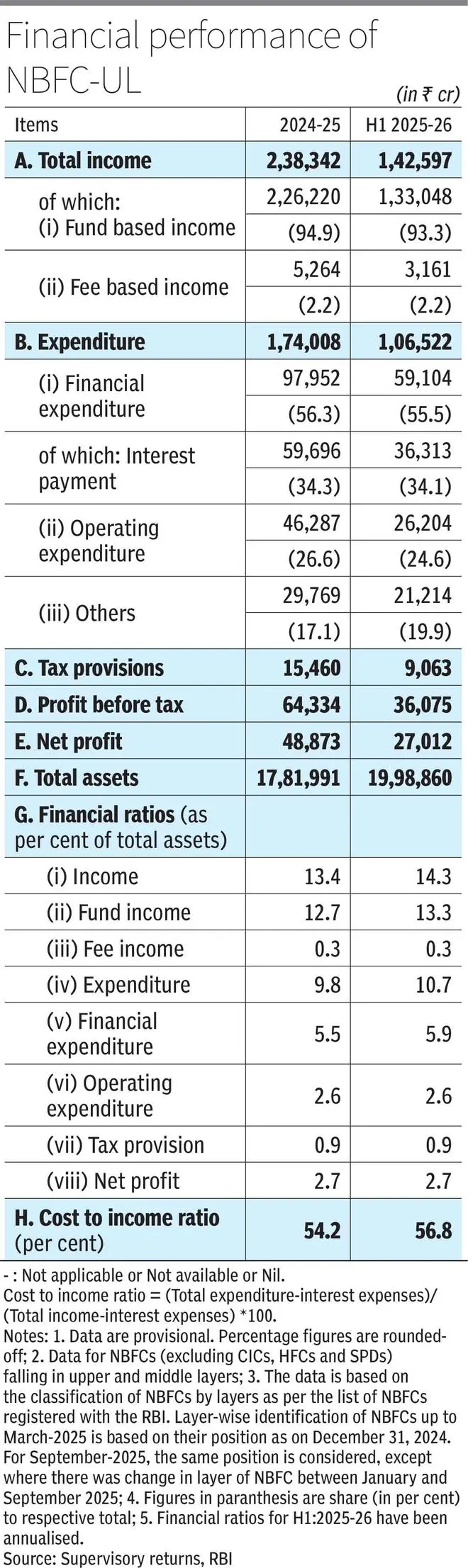

NBFCs are regulated under the RBI’s Scale-Based Regulatory Framework (SBR), which applies differential regulation commensurate with the scale and systemic importance of NBFCs. As of March 2025, there are 15 NBFCs (four of which are HFCs) in the upper tier category, which are subject to stricter regulations than the smaller NBFCs. The top tier NBFCs hold 30.2 percent of the total assets of the NBFCs at the end of March, while the middle tier (ML) NBFCs have a share of 64.6 percent due to the presence of government-owned NBFCs, while the basic tier (BL) NBFCs had a meager 5.2 percent share of the total assets.

Liabilities side

“On the liabilities side, growth in bank loans from NBFCs has moderated, with NBFC-ML experiencing a slowdown in growth compared to NBFC-UL, which registered a marginal expansion. NBFCs compensated for this moderation by increasing their dependence on market loans, driven by NBFC-ML. The increase in risk weights on bank loans to NBFCs, which was introduced in November 2023, was aimed at reducing dependence on NBFCs from bank loans to moderate loans,” the RBI said.

“On the asset side, loans and advances grew by 19.4 per cent at the end of March 2025, with upper tier NBFCs recording higher growth than NBFC-ML. Unsecured lending by NBFCs increased largely due to base effect, while secured loan growth declined over the same period. This moderation was mainly driven by mid tier NBFCs, whose secured credit growth declined at the end of March 2025 fell to 15.8 percent from 29.9 percent a year ago,” it added.

The asset quality of the NBFC sector showed further improvement in FY25 with the gross non-performing asset ratio (GNPA) declining from 3.5 per cent a year ago to 2.9 per cent in March 2025. The asset quality of all classifications of NBFCs, except NBFC-MFIs, has improved, the RBI said. END

Published on December 29, 2025

#Credit #extended #NBFCs #rise #GDP #March #RBI