Now, here’s today’s article:

Reader Jon: Jesse, I’m not sure why people would buy traditional bonds when you can get similar returns in an ETF that is more liquid?

Many other readers: my bond funds took a hit in 2022, and some are still underwater. But individual government bonds always return to the level! How could you ever Do you want to own a bond fund?

This is a nuanced topic, but since most retirees own or will own some bonds, it’s worth looking into.

As we peel the onion today, I hope you realize that this question is equivalent to:

- Would you rather buy your eggs one by one?

- …or by the dozen?

It doesn’t change the egg. It doesn’t change the meals you can prepare. It doesn’t change the space in your refrigerator. They are the same eggs.

So –

Should retirees own individual bonds instead of bond funds, or vice versa?

Maturity = The root of the problem

The core of the problem is that individual bonds are maturing. Ultimately, they return their face value to the owners, plus interest.

When interest rates rise and bond prices fall, owners often think: “Well, I’ll just hold on to it until adulthood and get my full worth back.” Bond owners feel they can ignore the price. It is imaginary on the border.

But bond funds not adult. They only return interest. To get your capital back, you must sell shares of the fund: possibly at a loss! The same rate hike that individual bond holders ignored feels much harder to ignore when it comes to a bond fund.

But what is a bond fund?

But what is a bond fund? What does a bond fund entail? Isn’t it…nothing more than the sum of many individual bonds?

If people have convinced themselves to ignore price changes in individual bonds, why can’t we do the same in bond funds?

The maturity reset

There is one essential difference between individual bonds and bond funds. As far as I’m concerned, this is the ONLY difference that makes sense in this conversation.

Bond funds (and those who manage them) tend to ‘reset’ fund maturities regularly. In contrast, most individual investors only do this sporadically.

What exactly does that mean?

To take BSV – the Vanguard Short-Term Bond ETF. It owns a range of US Treasury bonds with maturities ranging from 1 to 5 years and currently has an average maturity of 2.6 years.

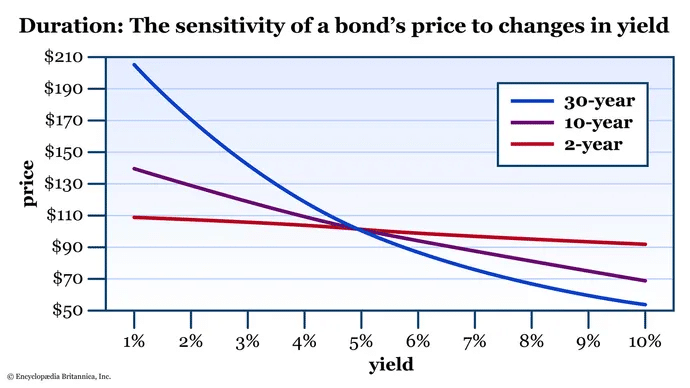

As a reminder, the term is a measure of interest rate sensitivity.

Every day the individual bonds in BSV move one day closer to their maturity date. Every day the total duration of BSV ticks down. And if the fund managers stood by and did nothing, the fund would eventually fully mature and return all its capital to its owners.

But BSV has a job, and it is that job not reach adulthood. Its job is to maintain a duration in the middle of the 2.X range. That is the purpose of this particular instrument, and many investors depend on it to maintain its predefined purpose. To achieve this, fund managers regularly trim here and there, reinvesting fund income in longer-dated bonds to offset the remaining bonds as they move toward maturity.

That’s how bond funds like BSV work.

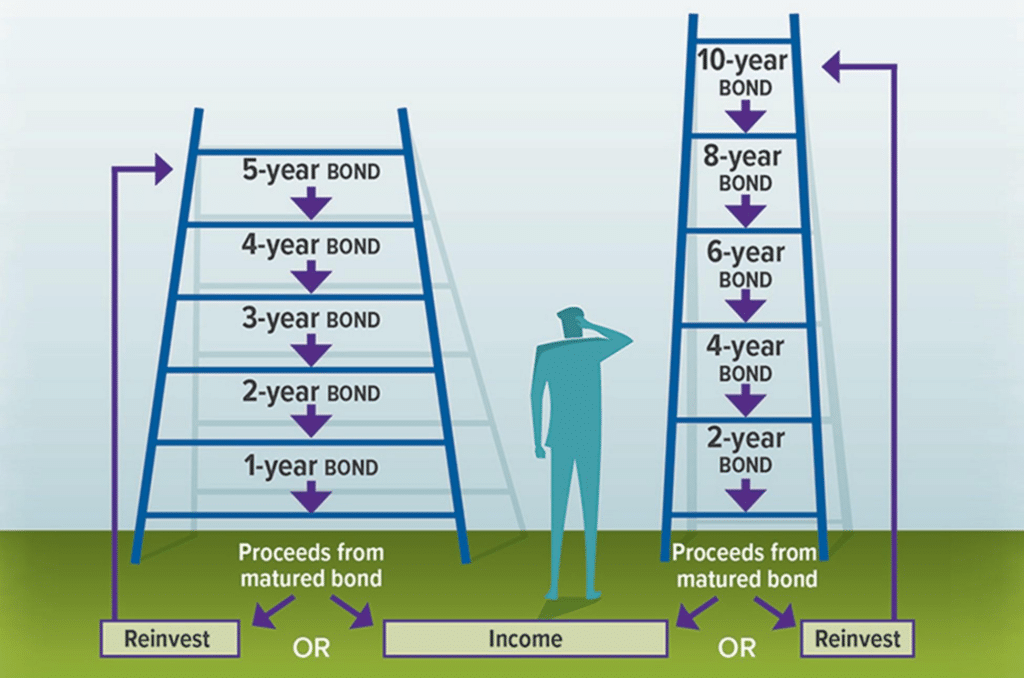

But now let’s compare that to Joe Retiree, aka “Mr. DIY Bond Ladder.”

Joe may have $50,000 in 1-, 2-, 3-, 4-, and 5-year Treasury bonds. Every day, Joe’s bond ladder gets one day closer to adulthood. Every day, the total duration of Joe’s bond exposure decreases.

But unlike BSV’s fund managers, Joe doesn’t care. In fact, this is probably what Joe had in mind. It’s really a feature and not a bug. Joe want to its 1-year government bond will soon mature. He wants to finance his pension with that capital. Then he’ll rebalance his portfolio to free up $50,000 to buy a new, shiny, five-year bond. Laddering was successful.

Let’s take a break.

See what just happened there? Did you catch it?!

Joe Retiree does it precisely what the BSV fund manager does. He resets his running time. Joe only does it once a year, while the BSV manager might do it once a week.

That’s the only difference! They are basically the same!

Would you rather?

On a side note, would you rather buy…

- A 10-year bond, price = $1000, yield = 2%

- A 10-year bond, price = $900, yield = 3%

Trick question. They lead to the same result. In ten years you will have $1,200 in cash from both bonds.**

Price and interest are opposing forces. The price of your bonds may have fallen, but that’s because yields have risen in an equal but opposite way. And if the price of your bonds rises, the yield falls. It’s cold, mechanical math.

(**Yes – the cash flows will be different and if we apply a discount rate the end result may be different. But accept this simple example for what it is)

But the fund price is still down!

I know some of you may be saying: “But my bond funds… their prices are still low since 2022!!!”

It’s true.

This is a diagram for AGG (its duration is ~6 years). Since 2022, it is still down 15%. Still not recovered (although the owners have received a stream of interest along the way).

But AGG is a fund. The managers consistently reset the duration.

If Joe Retiree had built something like a twelve-year bond ladder in 2022; its duration would be equal to that of AGG. And if Joe had done that, where would his bail ladder be now?

Its longer-dated individual bonds would have taken a hit in 2022, and they would still be underwater. Joe was able to calm himself by saying: “To me, they don’t feel underwater. I’m just waiting for them to grow up in six, seven, eight years.”

That’s fine if it makes Joe feel better.

But mathematically, Joe’s spinning bond ladder has matched AGG step for step. Joe rebalances his ladder once a year, while AGG rebalances much more often. That’s the only difference.

Other than that…

- The cash flows are the same.

- The portfolio values are the same.

- The returns are the same.

Everything is the same.

Bond funds are collections of individual bonds. A retiree’s bond ladder is exactly the same.

Apart from any tracking error due to the rebalancing frequency, we should not expect any significant differences.

Thanks for reading! Here are three quick notes for you:

First – If you enjoyed this article, please join the thousands of subscribers who read Jesse’s weekly free email, where he sends you links to the smartest financial content I find online every week. 100% free, you can unsubscribe at any time.

Second – Jesse’s Podcast “Personal finance for long-term investors” has grown ~10x in recent years and now helps ~10,000 people per month. Tune in and check it out.

Last – Jesse works full time for a fiduciary asset management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free consultation with Jesse to see if you are a good fit for his practice.

We’ll talk to you soon!

#Bonds #bond #funds #interest #rate