Banks’ outstanding advances to both sectors also hit a six-year high in March 2025, RBI data showed.

Private sector banks registered a CAGR of 19.3 per cent in advances to the capital market sector and a 20 per cent CAGR in their exposure to the real estate sector between FY20 and FY25.

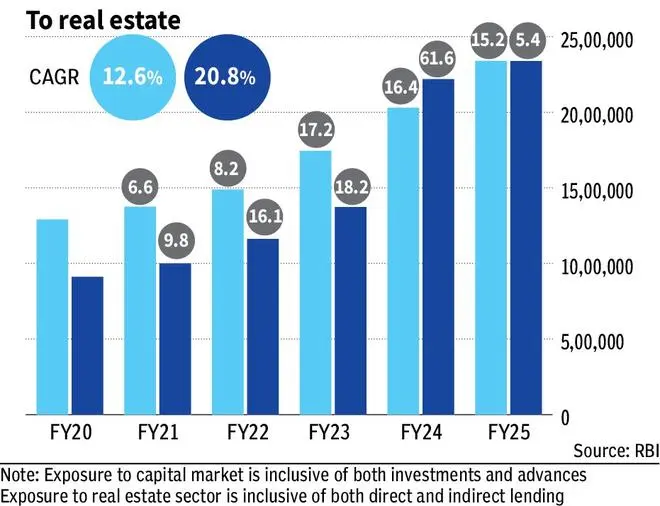

Public sector banks, on the other hand, recorded a slightly lower CAGR in their lending to the sectors. Capital market exposure grew at 15.6 percent CAGR, and real estate at 12.6 percent.

As per RBI regulations, banks’ exposure to both these sectors is classified as ‘sensitive’ given the risks inherent in asset price fluctuations.

Overall, private banks witnessed a sharp slowdown in exposure growth to sensitive sectors in FY25, after a sharp increase in the previous year, due to the impact of the merger.

On the contrary, public banks’ exposure to the capital markets increased, while in the real estate sector it decreased marginally. SCBs’ exposure to the sensitive sectors as a percentage of their total loans and advances in FY25 stood at 27.1 per cent, which is largely comparable to the previous year, data showed.

At ₹87,924 crore, public sector advances to the capital market sector grew 29 percent year-on-year. Private banks, on the other hand, witnessed a growth of 18 per cent to ₹191,945 crore as of March 2025.

Capital market exposure refers to banks providing loans to entities and individuals relating to equity markets. This may include intraday exposures and bank guarantees issued to stockbrokers (with cash margins), and loans against shares and bonds, among others. The real estate exposure includes builder financing.

Experts add that capital market exposure is likely to remain robust in FY26 given the overall boom in equity markets. However, growth in private real estate lending is expected to make bank financing to the sector sluggish in FY26.

“The banks’ exposure to the capital market sector [in FY25] is likely to rise due to increased turnover in the equity markets, which in turn leads to the requirement of higher margins for the brokers, leading to greater exposure through bank guarantees and intraday limits,” said Anil Gupta, co-group head of financial sector ratings at ICRA.

“Although volumes have declined in H1FY26, peak margin requirements for brokers remain stable and therefore exposure would not have declined in FY26,” he added.

Among PSBs, the largest lender, SBI, had the lion’s share of exposure to the capital market and real estate sectors at 61 percent and 47 percent of total advances to sensitive sectors.

Among private banks, the distribution was more evenly distributed, with HDFC Bank holding 30 percent of the private banks’ total exposure to the capital markets, and 40 percent in real estate.

“Economic growth of any country is reflected in the form of broader growth in the capital markets and real estate sector, and the same is seen in India too. With the banks’ increased focus on secured lending as compared to unsecured lending, exposures to these sectors have increased given the increase in the value of the sectors,” said Vivek Iyer, Partner and Financial Services Risk Leader, Grant Thornton Bharat.

(With inputs from Piyush Shukla)

Published on January 1, 2026

#Banks #exposure #capital #market #real #estate #sector #highest #point #years