Become a member of our Telegram Channel to stay informed of breaking the reporting

At the congress, American banks urge a stablecoin yield “mesh in the law that they warn, can drain up to $ 6.6 trillion to deposits of the traditional banking system, allowing credit streams to be destabilized to American companies and households.

The Bank Policy Institute (BPI), as well as the American Bankers Association, Consumer Bankers Association, the Financial Services Forum and the Independent Community Banks of America have all expressed their concerns in a letter Yesterday at the congress.

They expressed their concern about the current formulation in the guidance and the establishment of national innovation for the American Stablecoins (Genius) Act. The law signed on July 18, 2025 and establishes rules and regulations for Stablecoin expenditure that must follow.

The brilliant act is one of the most transforming laws in decades.@Jerallaireof @Richardquest on @CnnExplains what this means for Stablecoins. pic.twitter.com/bmliwjix3q

– Circle (@Circle) July 23, 2025

One of those rules is the prohibition on stablecoin emissioners who prevent them from offering interest or transferring directly to holders. However, according to the BIP, the law does not explicitly expand the prohibition to Crypto exchanges or affiliated companies.

In the letter, the BIP warned that “without an explicit prohibition that applies to exchanges that act as a distribution channel for Stablecoin emission or business -related companies, the requirements in the Genius Act can easily be avoided and undermined by the payment of interest to holders of Stabileveren.”

“The result will be a greater deposit risks, especially in times of stress,” the BIP says that it will have a negative influence on credit creation “during the economy” and $ 6.6 trillion out by the outflow of the traditional banking system.

The consequences of that event will “higher interest rates, fewer loans and higher costs for companies and households in the Hoofdstraat,” said the banking group.

Stablecoins differ fundamentally from traditional yields

The banking group said that Stablecoins fundamentally differ from bank deposits and money market funds because they do not finance or invest loans in effects to give holders of holders.

Instead, Stablecoin emissioners such as Tether (issuer of USDT) and Circle (issuer of USDC) generate in various ways in different ways to holders via third -party platforms.

Both companies have the same amount of reserves in Fiat, in their case the US dollar, as the amount of their tokens that are in circulation to ensure that their blockchain-based tokens retain a 1: 1 PEG on the Greenback.

Those reserves are largely on short -term assets those assets such as American treasury, who subsequently pay the issuers to holders.

Due to the prohibition of the Genius ACT, Egennents are not allowed to distribute the interest to holders directly. To bypass this, EXPENTEN such as Tether and Circle Agreements are going to share income with third parties with third parties or turn to loan and retention platforms such as blockfi and Gemini.

For example, Coinbase Currently, a yield of 4.1% offers everyone who owns USDC on their platform.

There are also returns-bearing stablecoins such as OUSD and SDAI that automatically enclose the efficiency of Defi loans, Real-World asset yields or other strategies directly in token. However, these stablecoins tend to come up with a higher risk level compared to USDT and USDC, mainly SMART contract, market and liquidity risks.

The BIP said those distinctions: “Wereldta why payment staboins should not pay interest, such as highly regulated and guided banks, do on deposits or offering yields such as money market funds.”

Stablecoin market a small percentage of the American money supply

The signing of the Genius Act last month was celebrated as an important milestone and turning point for the crypto room. Many saw his passing and subsequent signing as the first step to American regulators who offered the industry a long -awaited legal clarity.

Its signing also comes when US President Donald Trump and federal agencies insist to make the US the crypto capital of the world.

Within the first week of the genius law that was signed, the market capitalization for Stablecoins $ 4 billion to $ 264 billion jumped, according to to Defillama data.

Stablecoin Market Cap (Source: Defillama)

In the past week, the combined rating of Stablecoins in circulation has risen by more than 1%, around $ 2.76 billion to be around $ 271.37 billion from 6:23 am EST.

That growth is expected to continue in the coming years. In a April 30th reportThe American treasury predicted that the Stablecoin market could reach around $ 2 trillion by 2028.

On August 8, the S&P Global reviews History written and a “B” credit was assigned to the Stablecoin protocol, Sky protocol. The platform operates the DAI and USDS Stablecoins.

Despite the growing capitalization and recognition of Stablecoins, the sector is still a fraction of the American money supply. At the end of June, the American Federal Reserve (FED) reported That the American money supply was $ 22 trillion.

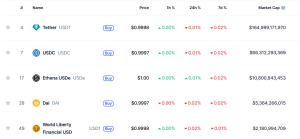

Tether’s USDT remains the largest stablecoin per market capitalization with a comfortable margin. Coinmarketcap data are appreciation at $ 164.99 billion.

Top stablecoins per market cap (source: Mint market cap))

USDC, which is supported by the New York Stock Exchange (NYSE) confirmed Firm Circle, is the second largest stablecoin in the market with its capitalization at more than $ 66.31 billion.

Related articles:

Best Wallet – Diversity your Crypto -Portfolio

- Easy to use, with function driven crypto-wallet

- Get early access to upcoming token ICOs

- Multi-chain, Multi-Wallet, Non-requiring

- Now in App Store, Google Play

- Commitment to earn native token $ best

- 250,000+ monthly active users

Become a member of our Telegram Channel to stay informed of breaking the reporting

#Bankers #warn #stabilecoin #proceeds #Maas #law #threatens #industry