A reader asks:

Long -term S&P 500 return figures are often quoted as already in 1926. Although almost a century with songs sounds great, nobody could really ‘buy’ the S&P then. The index arrives in the index of the 1950s and Bogle to actually buy it when a single purchase appears in the mid -1970s. Return numbers of the 50-year-old long-term long-term since Bogle stay parallel to the projections at 1926 or does this modern era show significant differences?

This is a person who knows their market history.

This is also my kind of question, so let’s dig in the historical component before we come to the performance numbers.

The standard statistics company1 Originally keeping track of 233 shares, but it was too difficult to maintain daily or hourly learning on so many shares for computers, so the S&P 90 was made in 1926.2

That original S&P 90 consisted of 50 industrial, 20 railways and 20 utilities stocks.

The S&P 500 was founded in 1957 consisting of 425 industrial, 60 utilities and 15 railways, which covered approximately 90% of the American stock exchange value.

In 1976, financial shares were finally added to the index, which moved to a 400-40-40-20 model of industrial, utilities, financial and transport shares.3

The inaugural Vanguard S&P 500 index fund of Jack Bogle was released that same year. In last bookBogle notes that the fund can only possess 280 shares because it would have been so heavy from a cost perspective to buy all 500 names. There was also a sales tax of 8% to buy that first index fund.

By 1988, the fixed model of 400 Industrials, 40 utilities, 40 financial data and 20 transports were left to display a more dynamic economy.

Here is the summary:

1923 – Standard Statistics Company begins the publication of daily stocks averages for 233 companies.

1926 – Launch of the S&P 90: 50 Industrials, 20 railways, 20 utilities.

1957 – The S&P 500 was made: 425 Industrials, 60 utilities, 15 railways.

1976 – The index has been revised to 400 industry, 40 utilities, 40 financial resources, 20 transports.

1976 – Vanguard launches the first retail index fund that follows the S&P 500.

1988 the fixed 400-40-40-20 model has been abandoned; Sector weights become adaptive to better display the economy.

Nowadays you look at something like 35% to 50% in technological shares, depending on how they are categorized, so we have clearly seen a lot of change over time.

Now let’s look at the performance history.

I have good historical data from DFA that go all the way back to 1926 and the launch of the S&P 90.

From 1926-1956 the S&P 500 was compiled with an annual return of 10.1%. That is not bad considering the disaster at titanic level of the great depression that shares fell more than 85%.

From the founding of the S&P 500 in 1957 to July this year, the S&P 500 has an annual return of 10.6%.

The IPO for the first Vanguard S&P 500 Index Fund was on August 31, 1976. If you start from the beginning of September 1976, the S&P 11.8% per year has risen.

Here is a handy graph that I made:

As you can see, the returns have not deteriorated over time with the arrival of the S&P 500 index or the index fund. In fact, they have become better, which partly comes from the fact that it is now easier to invest in the stock market.

Investing more people means more money that flows into shares, which means higher valuations and the like.

Certainly, you could poke some holes by changing your start and end date to make things look better or worse than these figures. But I would say that these time frames cover a wide range of market and economic environments.

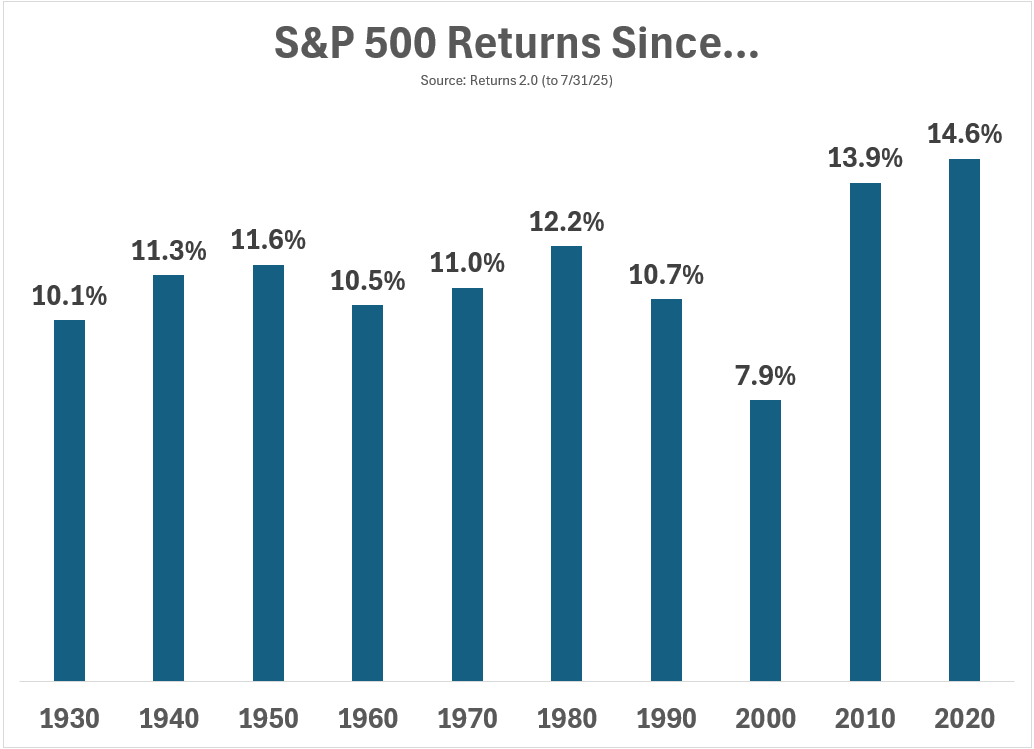

Here is another way to view S&P 500 retours in the longer term:

In shorter time frames you can get higher (2010 and 2020) or lower (2000) than average results. The annual returns are relatively consistent in longer time frames.

There is much more that can and will be thrown at the stock market in the coming decades, but the changes that we have experienced in the market structure for the past 50-75 years have not damaged the portfolio rates.

The long term still wins.

I answered this question about the latest edition of Ask The Compound:

Barry Ritholtz Is this week in my show to discuss questions about the cheap buying of luxury vehicles, how you can diversify the MAG 7, how you can measure the performance of your financial adviser and how you can perform the necessary diligence on private investment options.

Continue reading:

The evolution of financial advice

1They did not merged with Poors Publishing until the beginning of the 1940s, when it was Standaard & Poors.

2You could see the prices for the S&P 90 per hour, while the rest of the shares they followed only had a weekly price report.

3It is strange that it took so long, but apparently many financial companies have been sold in the past.

#short #history #wealth #common #sense