The aggregated returns of pension funds since 2000 have been almost identical To a simple 60-40 index portfolio.

That feels somewhat expected that it seems, but what about the true crème de la crème, the best settings. Certainly can they beat a simple buy and hold allocation?

It turns out that they really can’t. Below we remember an article that we wrote a few years ago: “Do Calper’s have to dismiss everyone and buy what ETFs?”

“He was a smooth politician from the US class, which is the only way to survive in that job. It has nothing to do with investments.”

That’s how Institutional investor Recently described a former CIO of the Pension System of the California Public Employees, also known as Calpers.

The description is especially interesting when it considering that the “I” in “CIO” stands for “investment”, which lifts an eyebrow about how the role “has nothing to do with investing”.

For readers who are less familiar with Calpers, it manages pension and health benefits for more than a million public employees, pensioners and their families. They supervise the largest pension fund in the country, with a value of more than $ 450 billion.

With that enormous amount of assets, there is a lot of control over how those assets are used. The CIO roll that manages this pension is one of the most prestigious and powerful in the country, hence Institutional investorS Interested. Apparently it is also one of the most difficult roles to hold. In the past decade, the position has on average a new CIO on average approximately every other year.

Now this article will not spend much time on the Calpers board, because many others have spilled a lot of ink there. Moreover, the drama around the pension is never ending and will probably have a new turn by the time we publish our article. (To be honest, Harvard’s donation problems are almost as dramatic …)

Instead, we are going to use the investment approach of Calpers as a starting point for a broader discussion about portfolio entry allocation, return, costs and wasted efforts. And if we do our work correctly, we hope that you will feel a little less stress about your own portfolio positioning by the time we are ready.

The stunning waste of the Calpers market market

The explained mission of Calpers is to “deliver benefits of pension and health care to members and their beneficiaries”.

Nowhere in this mission does it state that the aim is to invest in many private funds and to pay the blown salaries of countless private equity and hedge fund managers. But that is exactly what Calpers’ does.

Retirement Investment policy Document – And we don’t come up with this – is 118 pages long.

Their list of investments and funds is 286 pages long. (Maybe they should read the book “The index card“)

Their structure is so complicated that for a long time Calpers cannot even calculate the costs that it pays to its private investments. With regard to that comment, by far the largest contribution to high costs is the private equity allocation of Calpers, which they intend to increase the allocation. Is that a well thought out idea or is it an orphan greeting Mary -pass after years of underperformance? According to a recent portfolio of Calpers, 0.49% returned from 2000 to 2020.

Now it is easy to criticize. But is there a better way?

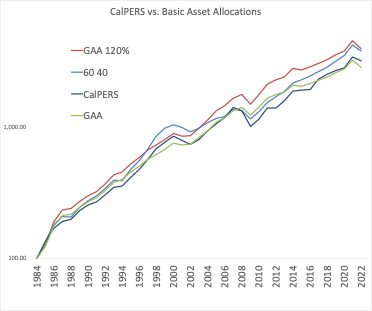

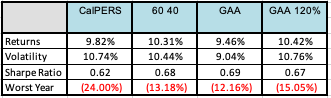

Let us investigate the historical return of Calpers on some basic strategies for asset spreading.

We start with the current portfolio entry allocation of Calpers:

Source: Calpers

Now that we know what Calpers is working with, we let the returns compare with three basic portfolios that start in 1985.

- The classic 60/40 US shares and bonds benchmark.

- A GAA portfolio from Global Asset Allocation (GAA) from our book Global allocation of assets (Available as a Free e book here). The allocation approaches the allocation of the global market portfolio of all public assets in the world.

- A GAA portfolio with a slight leverage, because many of the funds and strategies that use Calpers have embedded leverage.

Source: Calpers, Global Financial Data, Cambria

As you can see on the table, Calpers from 1985-2022 cannot distinguish itself from our simple “nothing” benchmarks.

To be clearer, the returns are not bad. They just don’t Good.

Consider the implications:

All the time and money issued by investment committees about the allocation …

All the time and money spent on purchasing and allocating private funds …

All the time and money spent on consultants …

All the time and money spent on hiring new employees and CIOs …

All the time and money spent putting endless reports to follow the thousands of investments …

Everything – absolutely wasted.

Calpers would have been better to just fire their entire staff and buy some ETFs. They have to call Steve Edmundson? It would certainly make the record a lot easier!

Moreover, they would save hundreds of millions a year on operating costs and external fund costs. Cumulative over the years, the costs run well in the billions.

I personally take the “i” section of the acronym very seriously and I offered to manage the Calpers pension for free.

“The pension funds that are struggling with underperformance and large costs and staffing. I will manage your portfolio for free. Buy a number of ETFs. Rebal every year or so. Keep an annual shareholders’ meeting about a pale pale Ales. Perhaps write in assessment for a year.”

I have Applied three times before the CIO rollBut Calpers has rejected an interview every time.

Perhaps Calpers should update her mission statement to “deliver benefit and health care benefits to members Calpers -employees” Private fund managers and their beneficiaries. ‘

In this case they would succeed.

Is it just Calpers, or is it the industry?

One could look at the above results and conclude that Calpers is a bucket.

Critics can reduce and say: “Ok Meb, we get that Calpers cannot buy and retain a base, but let’s be honest – it’s the government! We define our government through mediocrity. Every serious private pension or institution should use smart money, the big hedge fund managers.”

Fair point. So let’s broaden our analysis.

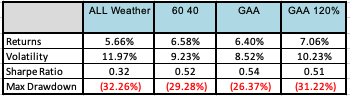

We will do this by investigating the largest and most famous hedge fund manager, Bridgewater. This $ 100 billion+ money manager offers two main portfolios, a buy and hold “All -Weather” strategy and a “pure alpha” strategy.

In 2014 we went to Clone Bridgewater’s All Weather ”Portfolio-a’s allocation that, according to Bridge Gewater, was tested by two recessions, a real estate bubble and a global financial crisis.

The clone, based on a simple global market portfolio that consists of indexes, has well replicated Bridgewater’s offer when it was tested back. What is even more important, running the clone would require zero hedge fund management costs and lockups and would not have been weighed by a tax investment efficiency. To be honest, this backrest has the advantage afterwards and does not pay any costs or transaction costs.

The All weather portfolioWith its focus on risk carity, it shows that if you build a portfolio, you do not necessarily have to accept pre -packaged asset classes.

When it comes to shares, they are inherent leverage, for example, and most companies have debts on their balance. So there is no reason or obligation to hire shares at their fictional value. A choice for “Deleverage shares” would be to invest half in shares and half in cash. And the same applies to bindings, you can use them up or down to make them more or less volatile.

This approach has been around for a long time, more than sixty years. Dating from the days of Markowitz, Tinbin and Sharpe, the concept is essentially a super diversified buy-and-hold and again balance folio-one in which the founder of Bridgewater Ray Dalio says he would invest if he died and needed a simple allocation for his children.

So the largest hedge fund in the world should stamp an allocation that could be written on an index card?

Again, from 1998-2022 we see that a basis 60/40 or worldwide market portfolio is doing better than the largest hedge fund complex in the world.

Source: Morningstar, Global Financial Data, Cambria

One can answer: “Ok meb, all the weather should be a purchase and hold portfolio. They charge low costs. You want the good things, the actively managed Pure Alpha!”

What about the actively managed portfolio of Bridgewater?

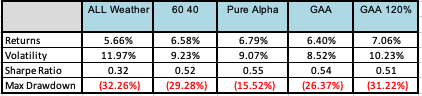

Dalio separated the All Weather Portfolio from the Pure Alpha strategy from Bridgewater, which is intended as the multi-strategy, to go everywhere.

His idea was to separate ‘beta’ or market performance from ‘Alpha’ or extra performance on top of the average marketing. He believes that beta is something you have to pay very little for (we went on the record by saying that you don’t have to pay anything for it).

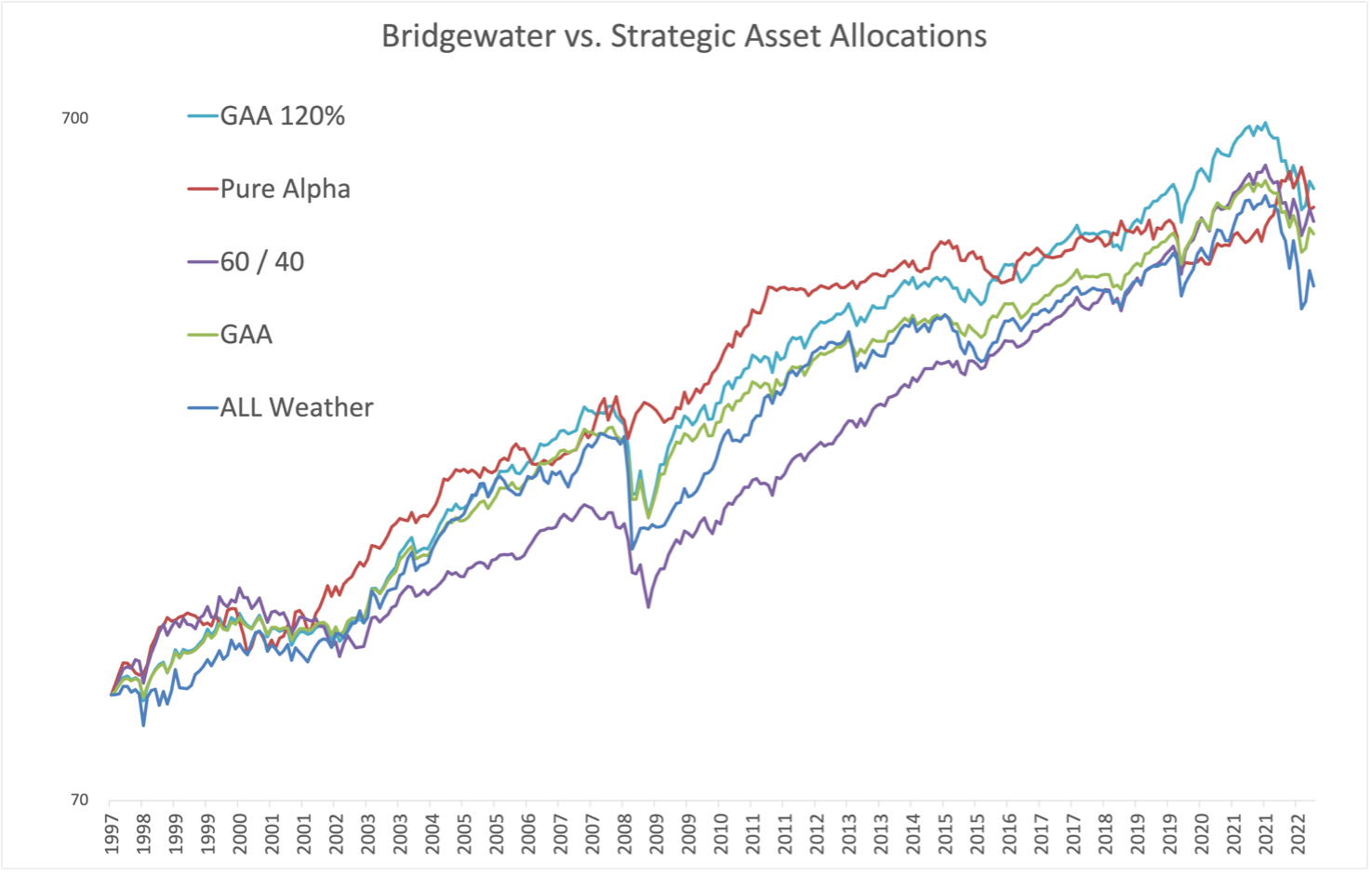

Now let’s bring the Pure Alfa strategy into the mix. Below we will compare it with all weather conditions, the traditional 60/40 portfolio and the Gloal Asset Allocation (GAA) portfolio from our book and higher. Finally, the risk carity strategy uses some leverage, so we also did a test with GAA and leverage of 20%.

The replication strategy Back tested the respective performance of the portfolios between 1998 and 2022.

Source: Morningstar, Global Financial Data, Cambria

Again, the return of Pure Alfa was almost identical to the GAA and 60/40 portfolios, with performance that differed less than 0.5%. And don’t miss that Pure Alpha has actually left the lever version of the GAA portfolio.

Again, this is not bad, it’s just not good.

Some may say: “But Dalio and the company did this in real time in the 1990s with real money.”

We absolutely give up our hat that argument, and moreover the Pure Alpha looks like it needs another return path than the other allocations, which probably offers some diversification of the non-correlation to traditional assets. We also acknowledge that the benchmarks include a special one Strong behind running run for our shares.

Here is the problem. Many of these hedge funds and private equity strategies cost the end investors 2 and 20, or 2% management costs and 20% of the performance. So that 10% annual gross performance after all those reimbursements are reduced to 6%.

So yes, maybe Bridgewater and other funds generate Alfa, the problem is that they all keep it for themselves.

Anyway, it is good to see that you can replicate a huge amount of their strategy, only by buying the global market portfolio with ETFs and reinforcing it once a year, while avoiding enormous management costs, paying extra taxes or need mass minimal buy-ins.

The relevance for your portfolio

Let’s take this away from the academic and make it relevant for your money and portfolio.

While continuing with articles at the end of the year and proclaiming how you can position your portfolio for a sample 2024, or more likely the preference for gloom and downfall, news, news, a threatening large recession and crash is coming … If you emphasize how much money to put in gold, or oil, or emerging markets …

“Does it even matter?”

If the largest pension fund and the largest hedge fund cannot perform better than the fundamental Buy and Hold supplies allocations, what chance do you have?

For all pension funds and donations there are, the offer is – we are happy to design a strategic asset spread for free. We save you the $ 1 million in basic and bonus for the Calpers Cio role. The only thing we ask is that we might meet once a year, possibly and share some drinks.

#Institutions #beat #fundamental #buy #hold #allocation #Meb #Faber #Research #Fair #Market #Investing #Blog