The Reserve Bank of India (RBI) has already switched from monthly to 15-day credit reporting from January 1, 2025. Now, it has issued draft rules that will take the system further: By July 1, 2026, banks and NBFCs will have to update your credit details with bureaus every week.Here’s what that actually means if you’re a borrower with loans, credit cards or EMI-based purchases.

1. What exactly is changing?

First, two separate, but related steps:Step 1 (already in effect): 15-day updates Beginning January 1, 2025, all lenders must update credit bureau data every 15 days instead of approximately once a month.Step 2 (suggested): Weekly updates from July 1, 2026

Made using AI

RBI has released draft changes on its website Credit Information Reporting Directions2025. If completed in their current form, they will require:

- Full file once a month: Lenders send a full snapshot of all active and recently closed accounts as of the end of the month.

- Weekly “incremental” files (such as on the 9th, 16th, 23rd and last day of the month):

- New accounts opened

- Accounts closed

- Changes caused by the borrower (repayments, foreclosure, change of address, guarantor, etc.)

- Changes in asset classification (for example, when an account becomes stressed or recovers)

In addition to weekly updates, RBI also wants:

- Reporting of CKYC (Central KYC) numbers to make identity matching cleaner

- Standard, uniform validation rules so that one agency doesn’t reject data that another accepts

- A monthly

Data quality Index Score (DQI) for each lender – essentially a number for how clean and current their data is

Think about it this way: Your credit report changes from a monthly snapshot to a biweekly diary and then to a weekly log that should eventually become almost real-time.

2. Faster rewards: Good behavior will be visible sooner

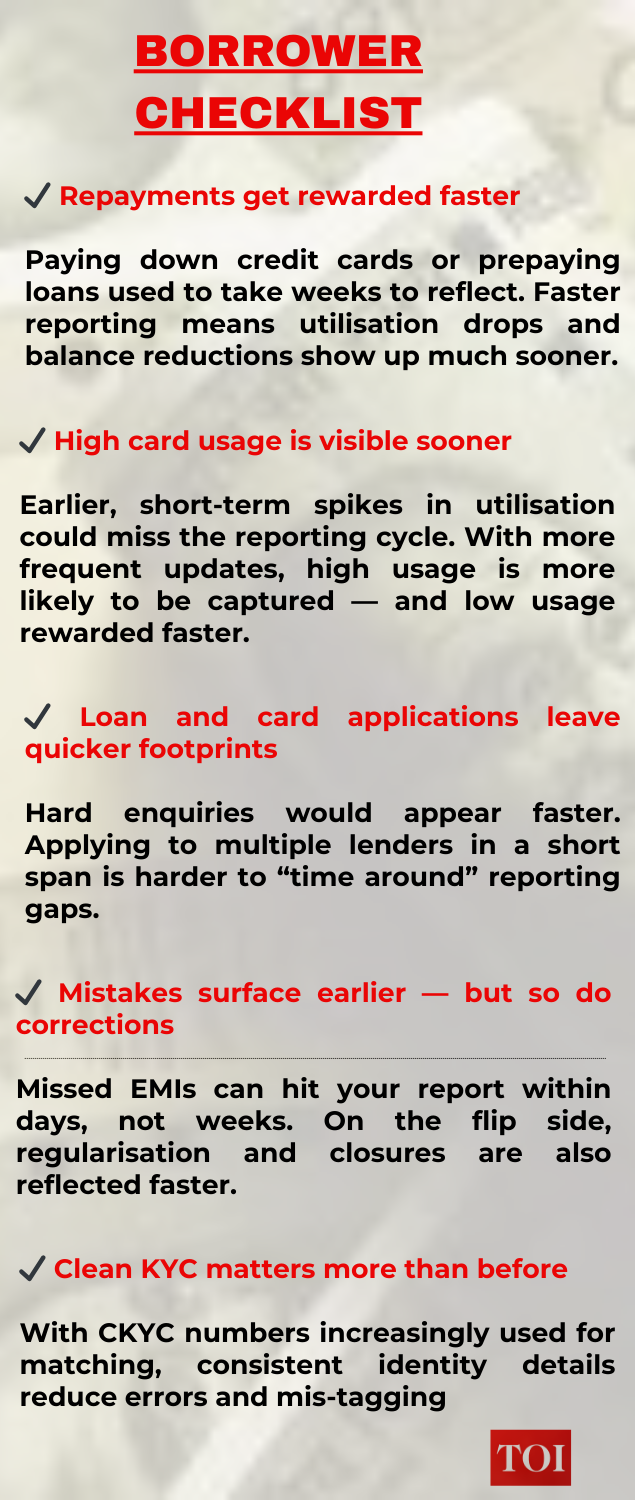

The biggest win for consumers is timing. Many borrowers have faced this scenario:> You prepay a large portion of a personal loan or drain a credit card, and then wait… and wait… for your credit score to reflect it.Under the old monthly system, the delay could easily amount to 30 to 45 days. Even with a 15-day report, you could still wait a few weeks. Weekly updates further compress that delay.What will change for you:

- Faster score improvement after prepayments

- If you pay off a large part of the debt on, for example, the sixth of the month: for monthly cycles, this may not appear until after the following month’s file. With weekly reporting, it can be picked up in the next “incremental” file and reach the agencies within a few days.

Faster recovery from one-time errors If you missed an EMI three months ago but have since regularized and paid on time, the status correction (from overdue to regular) should be communicated sooner. This can ensure that your score stabilizes more quickly.More timely access to better offers Many lenders automatically screen customers for pre-approved personal loans, top-ups or credit cards based on credit scores. A system that reflects improvements on a weekly basis increases your chances of being identified as a “good” borrower sooner.Net effect: if you are disciplined, the system is no longer so slow in recognizing them.

3. Stronger shield against fraud and errors

RBI’s move is not just about rewarding good behavior; it’s also about reducing the damage caused by bad data and fraud. Less ‘ghost loans’ and identity abuseIn a monthly system, there is a period where fraudsters can take advantage of delays, for example by taking on multiple loans or lines of credit before the first one even appears on your report. Weekly updates shorten that period significantly, making it more difficult to execute such hit-and-run loans.Better detection of errorsRBI guidelines already require agencies and lenders to correct incorrect entries within tight timelines, with a compensation mechanism (₹100 per day) if rectification is delayed beyond 30 days from your complaint.

Made using AI

Weekly reporting plus:

- uniform validation rules, and

- mandatory data quality scores

- …means fewer mismatches, fewer file rejections, and less space for your report to show:

- a loan as “open” when you have taken it out, or

- a higher outstanding amount than you actually owe.

Easier to correctly link your data

- Requiring lenders to share CKYC numbers (where they have them) with credit bureaus could address a classic Indian problem:

- Same person, multiple spellings of the name, different addresses, different ID combinations.

Cleaner identification reduces the chance of someone else’s loan being placed on your profile – a nightmare scenario that can devastate your score.In short: the accuracy of your credit report should improve, and if something is wrong, there’s a tighter framework to fix it.

4. The downside: less room to game the system, more discipline

There is a trade-off for consumers: the system will also punish bad behavior more quickly.Hard pulls and fast applications appear fasterIf you apply for multiple loans or credit cards in a short period of time, these tough questions will be reported weekly instead of on a long delay. That’s possible:

- Take a few points off your score faster, and

- Communicate to lenders that you are aggressively seeking credit.

In other words, the classic tactic of “apply to five lenders before the first inquiry ends up in my report” is becoming more difficult.Missed EMIs are more likely to biteA missed or delayed EMI doesn’t wait until the end of the month to appear on your report. With weekly increases and fast agency withdrawal timelines, the sloppiness in reimbursements is likely to be visible within days, not weeks. ([TaxGuru][2])That’s good from a systemic risk perspective, but for you it means:

- No comfort in “I’ll fix it next month; it won’t show so quickly.”

- If you slip, expect the score to respond quickly.

More frequent score movementEven small actions – closing a card, taking a new BNPL line, moving an EMI date – can show up faster. Expect your score to fluctuate more often, especially if you are financially active.The key is not to obsess over every 10-point move, but to keep an eye on the trend:Does it increase over three to six months?Are there any major negative surprises?

5. What this doesn’t mean

It’s easy to misinterpret “weekly credit score updates” and assume a few things that aren’t automatically true.1. You are not guaranteed a free weekly credit reportRBI already mandates that credit bureaus give you one free full credit report (with score) per year upon request. ([Reserve Bank of India][5])The new weekly rules are about how often lenders send data to agencies, not how often agencies must give you detailed reports for free. Many apps and fintechs will show you your score more often, but that is a commercial choice and not a direct RBI guarantee.A higher score every week is not automaticIf nothing meaningful changes in your borrowing behavior:

- Paying regular EMIs on time is already factored into your score.

- Weekly updates won’t magically increase it every seven days.

The benefit is that when you make major changes (debt payoff, foreclosure, settlement), they should reflect more quickly.3. It is not a promise of loan approvalEven with more up-to-date data, lenders still use their own internal rules – income thresholds, employer lists, geography, age, industry exposure – before approving a loan. Weekly reporting simply makes the starting information more accurate and up to date.

6. What you need to do now as a borrower

You don’t have to do anything technical to “activate” weekly updates – that’s between RBI, lenders and agencies. But you *can* tailor your behavior to get the most out of the new system.

a) Strategically clearing expensive debt

- Because good moves are recognized more quickly, it makes sense to:

- Tackle maxed out high interest credit cards and personal loans first.

- Try to keep your credit utilization (used limit ÷ total limit) on each card below 30-40%.

- Weekly reporting means the impact of these refunds should be reflected sooner.

b) Spread out credit applicationsBecause questions appear faster:Avoid applying for multiple cards or loans within the same month “just to see who approves.”Prioritize offers that are likely to be approved (pre-approved or pre-qualified offers).c) Check your report at least once a year – and after major changesGiven the tighter timelines and compensation rules for corrections:Get your free annual report from at least one agency.Also look after major events: taking out a home loan, restructuring a loan or resolving a long-term dispute.If something is wrong, file a complaint with the lender and agency; If they do not resolve the issue within the timeframes specified by the RBI, you are entitled to compensation. ([Reserve Bank of India][4])d) Keep your KYC trail cleanSince CKYC numbers will increasingly anchor your data, make sure that:

- Your mobile number and email address will be updated with banks and NBFCs.

- Your primary identity documents (Aadhaar, PAN) are consistent in spelling and address.

- Cleaner KYC data reduces the chance of wrong tags and makes fraud detection easier.

The big picture: towards “real-time” creditRBI’s weekly update plan is part of a broader effort to make India’s credit infrastructure real-time, more accurate and more borrower-friendly. Policymakers and bankers talk openly about the eventual daily reporting – weekly is the bridging step to get there. For consumers, the message is simple:If you use credit responsibly, the new rules are largely good news:

- Your improvements will be visible faster, your profile will be harder to abuse, and the system will have clearer standards for fixing errors.

- If you use credit casually, the system will notice and price it in much faster.

Either way, your credit report is about to get a lot more vibrant. The best response is to think of it less as a static score and more as a weekly report on your financial habits.

#credit #report #weekly #RBIs #rules #EMIs #cards #loans #Times #India