The last four years have been very interesting in the Toronto real estate market.

Actually, the last twenty-two years have been very interesting! I don’t know if there’s ever been a boring moment as long as I’ve been in this business, but for the purposes of today’s discussion, we’re talking about “interesting” because it relates to coming off a twenty-year bull run and witnessing the market decline.

I want you to think about this statement for a moment:

“If I can’t sell the apartment, I’ll just keep it and rent it out.”

Now ask yourself Why and inside What situation where a condo seller would utter these words.

There are all kinds of scenarios, and each of these scenarios can be further divided into sub-scenarios a), b) and c).

But consider the following three situations for someone might say, “If I can’t sell the apartment, I’ll just keep it and rent it out.”

1) An old investor who wants to sell the apartment and leave the space.

2) An end user who has bought a house, has moved and wants to sell the existing apartment.

In the first scenario, the investor wants to leave the space, he or she does not get the price he or she needs or wants, and he or she decides to remain a landlord for a little longer. That’s not ideal, but not terrible either.

In the second scenario, the end user is clearly in a financial position that allows him or her to complete the home purchase without Selling the apartment, thus being ‘forced’ to keep it, will not result in financial danger. However, it does make the owner an ‘accidental landlord’.

I have experienced both situations a lot of since the market started falling in 2022, and some have been fine while others have been disastrous.

A couple living in downtown Toronto called me in late 2022 and said they had bought a house in British Columbia and moved there, and now they wanted to put their apartment up for sale.

At the time we had discussed how the market was changing and what ‘realistic expectations’ should look like.

I did a full market analysis of the apartment and gave them an assessment of its ‘fair market value’. However, they wanted to sell for the price their neighbor got in March.

I told them from the beginning, “I don’t think this is the right way to proceed,” but they said they were “not in a hurry” and “didn’t need to sell,” so I told them that as long as they agreed to the worst-case scenario where the market continues to decline and the apartment remains unsold, we could proceed.

As expected, there were virtually no viewings and we never received an offer.

I told them several times to adjust the price but they were unwilling.

January came and they finally agreed to adjust the price, but only based on what I told them in August of the previous year when we first discussed the sale. Unfortunately, the market continued to decline, and that number was now in the rearview mirror.

Again they said to me, ‘It’s fine, but we won’t do that need to sell,” and we stayed on the market until April.

Then they told me, “We’re going to keep the apartment and rent it out.”

I did my job; I played devil’s advocate with them and discussed what it would be like for them to ‘manage’ a property in Toronto while they were in British Columbia, but they said they weren’t concerned about that at all.

We found a suitable tenant in April and the tenant took over the building in May.

However, those tenants only stayed for a year. So in May 2024 I was tasked with finding new tenants for them.

That was the last I heard from those customers, but me did note that the property appeared on MLS for rental in May 2025 (i.e. not with me), only this time the landlord specified in the lease was a property management company.

I assume with a high degree of certainty that “managing” a 1,400 square foot, 2 bedroom, 3 bathroom apartment in downtown Toronto, as well as the tenants renting out a property like this (their personality, requests, demands, etc.) became too much for my (former) clients, and they ended up hiring a property management company to take charge.

Every property management company is different, but many charge 20% of gross rent right from the top. That’s one lot.

As for the value of the condo, I don’t think I need to point out that the market has steadily declined since we first listed it for sale in the fall of 2022.

Ultimately, you can’t really say whether these clients’ actions were “right” or “wrong.”

Sure, they downsized more than they could tolerate, and in retrospect it’s easy to say, “They should have sold in 2022,” but they appear to be in a financial position that allows them to hold the apartment for as long as they want or need, presumably to chase the market price that existed at our 2022 peak.

An argument can be made that they should have implemented a 5-6% haircut in the fall of 2022, reinvested the money and avoided a further 10% decline, but that’s simply true. An way of seeing.

Who knows what was on their minds then, or even now.

The point I’m going to make is this:

There are a lot of units on the rental market that were originally intended for the resale market.

We discussed this in 2025, and so did I personally three clients put their apartments up for sale last year and then decide to keep them, turn around and rent them out.

You would think this would have had consequences for the rental market, especially for apartments in the city center. Suffice it to say, most people wouldn’t hesitate to sell a 3-bedroom house downtown, then turn around and rent it out.

Now that 2025 is in the books, I wanted to revisit a quarterly article here on Toronto Realty Blog and look at the updated statistics for the downtown apartment rental market.

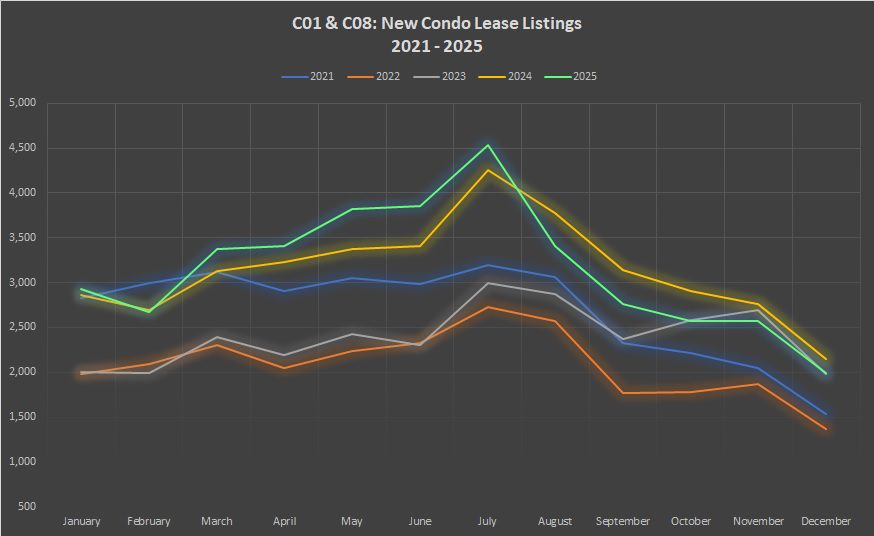

When we last looked at the data in late September, we saw, quite astonishingly, a reject in the number of new apartment listings.

That trend continued in the fourth quarter:

This is the spitting image of a ‘trend reversal’.

New advertisements have arrived six of the first seven months of 2025 (with the only down month being only 1%), and suddenly in August the trend reversed.

From August through December, we saw five consecutive months of year-over-year quotes downand three of those months were down double digits.

For all the talk about “the rental market being flooded with inventory,” I’m not sure the following chart supports this:

Okay, if you want to make the “flooded” claim in March, April and May, then you might have a point.

Definitely “flooded” compared to 2022 and 2023, although somewhat in line with 2024.

But as we enter summer, the trend changes dramatically.

Not only that, by the time we reach October, the number of new listings starts to drop below both 2023 and 2024.

Ads were still good, Good ahead of 2021 and 2022, but many more units have been completed since then.

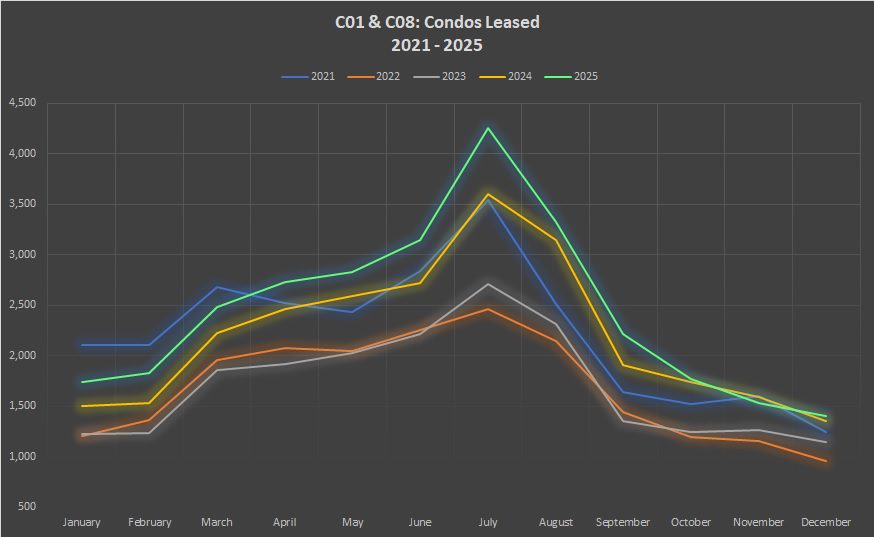

As it relates to rented units, we saw very large figures on an annual basis in the first, second and third quarters.

That also changed when we went to Q4:

I’m not sure what happened in November. That red figure certainly feels like an outlier!

But in general, with the number of lease entries is declining, perhaps we should not be surprised that the number rented units also decreased.

These do not have to be tied hand in hand, but you obviously cannot lease what does not exist.

The following diagram is interesting and worth another discussion:

How many articles have you read in 2025 about there being “fewer international students” here in Toronto?

Five? Ten? Twenty?

That’s news everywhereand considering that September 1st is the most common possession date for students, and thus July is the most popular month for students to lock in a rental, you might think that the number of rented units would have plummeted in July.

But that didn’t happen.

In fact, the chart above shows what can only be described as a “peak” in July.

You can’t miss it.

It literally puts your eyes out!

Now that we’re done looking at the number entries as well as the number of units rentedwe need to put this together and see how efficiently the stock is absorbed.

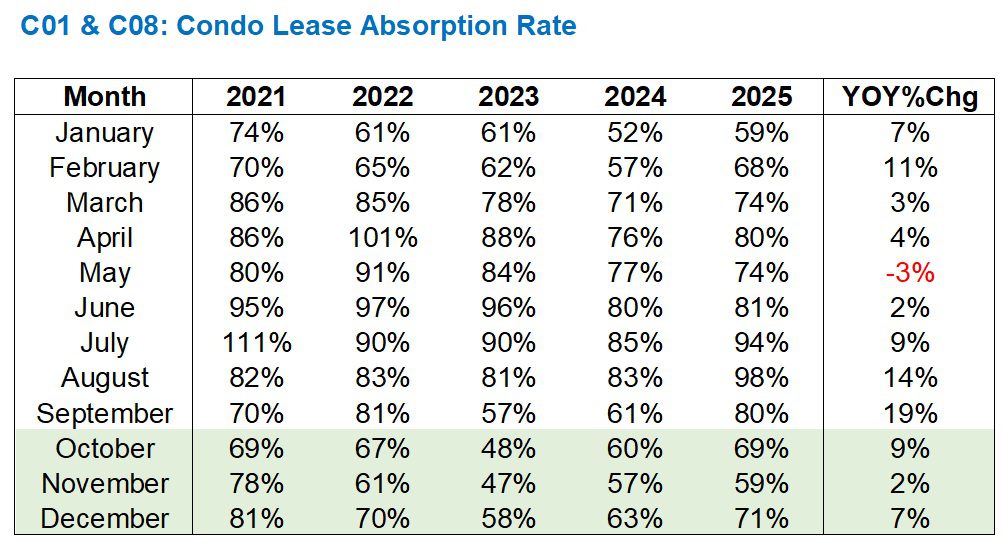

So ours absorption rate on the market, or what many people call the “sales-to-new-listings ratio,” or SLRR for short:

Again, I would have to think that given all the talk about the “slow rental market,” we shouldn’t do that to expect to see a year-over-year increase in the absorption rate.

But it’s not just a year-on-year increase that’s worth noting.

If you look at the month of October, that 69% absorption rate is even higher than in 2024, 2023 and 2022, and tied with 2021.

This hardly feels like a “soft” rental market to me.

Although November’s 59% absorption rate is substantially lower than 2021, it is still higher than 2024 and 2023, and only 2% lower than 2022.

December is higher than all from 2024, 2023 and 2022, and only in December 2021.

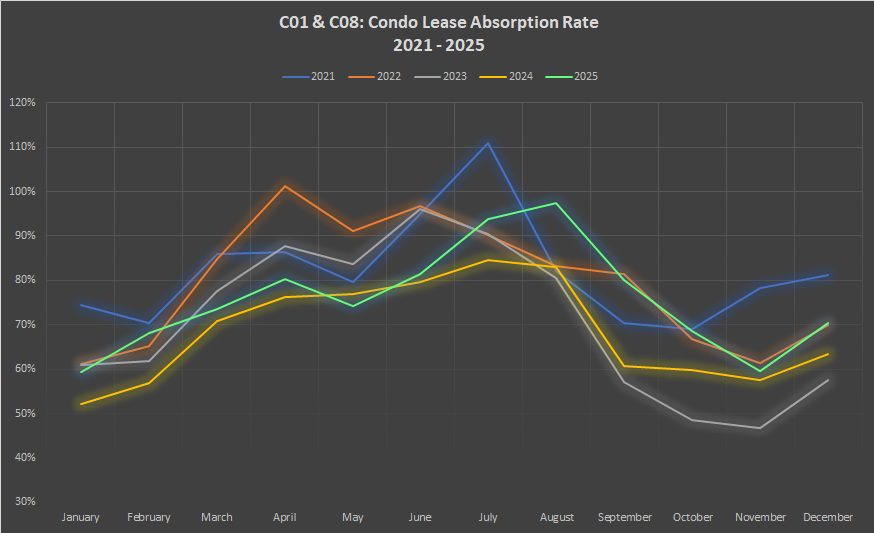

Our bright green line below shows that this is not a soft rental market. Far from it, actually…

There is nothing about this chart that says “weakness” or “soft.”

Nothing says ‘decreasing’.

If you want to see it decreasingJust wait until my upcoming post on the GTA resale condominium market, where you’ll see lines on graphs that are almost off the charts, figuratively speaking, and literally speaking too.

For what it’s worth, I have three investment apartments and all three are occupied by the original tenants. Two of the tenants occupied the building in 2024 and one tenant in early 2025.

If you’re looking for a takeaway or two from the previous charts, I’d offer this:

1) Lease offers are down year after year.

2) The absorption rates are upwards year after year.

Let’s see how Q1 goes, and we’ll be back here for an update in the first week of April!

#rental #market #downtown #Toronto #Toronto #Realty #Blog