The book was primarily a common sense introduction to how to manage money as a physician in a way that would lead to financial success. It has helped tens (hundreds?) of thousands of physicians, and it was largely accurate and functioned as intended. But it wasn’t perfect. It wasn’t perfect because my crystal ball wasn’t functioning. There have been some economic changes in the last twelve years that make at least one chapter in the book look quite strange.

That chapter is called The Big Squeeze.

The Big Squeeze would consist of physicians caught between the rock of declining and even declining revenues and the hard place of the rising costs of medical education and student loans. That didn’t really go as expected when I wrote the chapter.

Doctors’ incomes

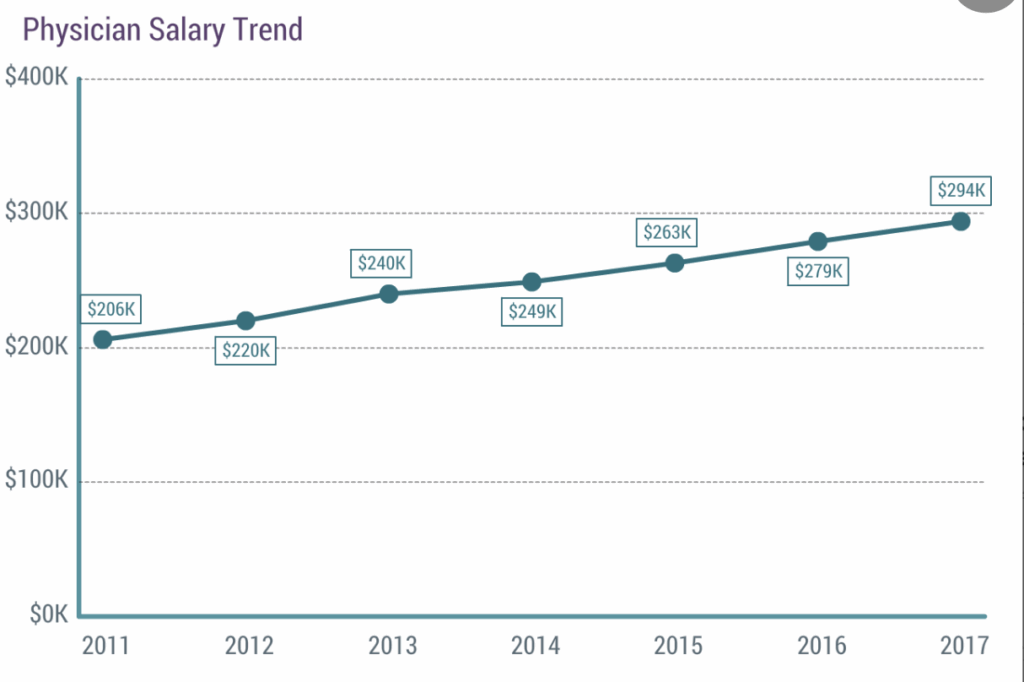

Doctors’ incomes have continued to rise, at least on average. Here’s a recent Medscape survey slide showing the trend:

Here’s a similar slide from the 2017 survey:

I know that many doctors are earning less than they used to, some doctors are working more to maintain the same income, and the general trend is that fewer and fewer doctors are self-employed. But the fact remains that, on average, at least over the past twelve years, physicians’ incomes have increased, not decreased. Yes, I know a lot of that increase is just inflation. But if we use the 2024 number ($374,000) and that 2011 number ($206,000), that’s an annualized increase of 4.7%. Meanwhile, inflation, as measured by the CPI-U, increased by just 2.6% annually between 2011 and 2024. That includes the 2021-2023 inflation spike, so it’s clear that physician incomes haven’t actually fallen.

More information here:

16 Ways to Make More Money as a Doctor

Will more money make me happier?

Residents say a modest salary increase is ‘a shame’. Some believe they earn more than double their wages

The cost of medical school

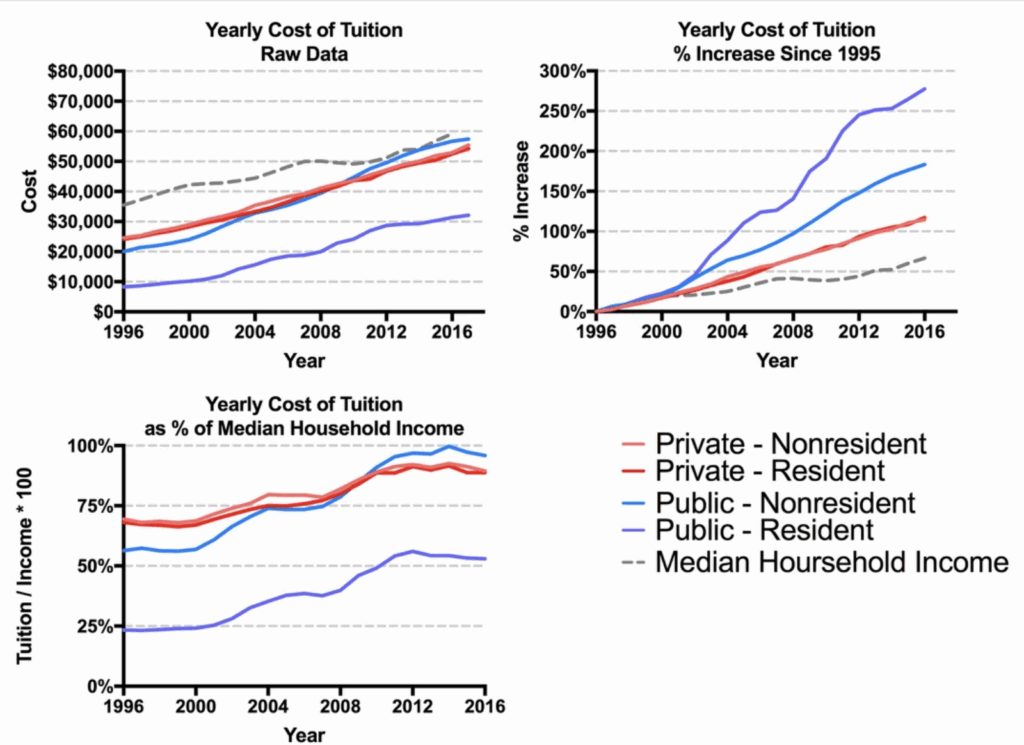

Now that we’ve covered the rock, let’s talk about the hard place. We’re talking about the cost of medical school. It is certainly true that average tuition and cost of attendance have increased. Here it is a graph from Reddit which shows that, at least until about 2016:

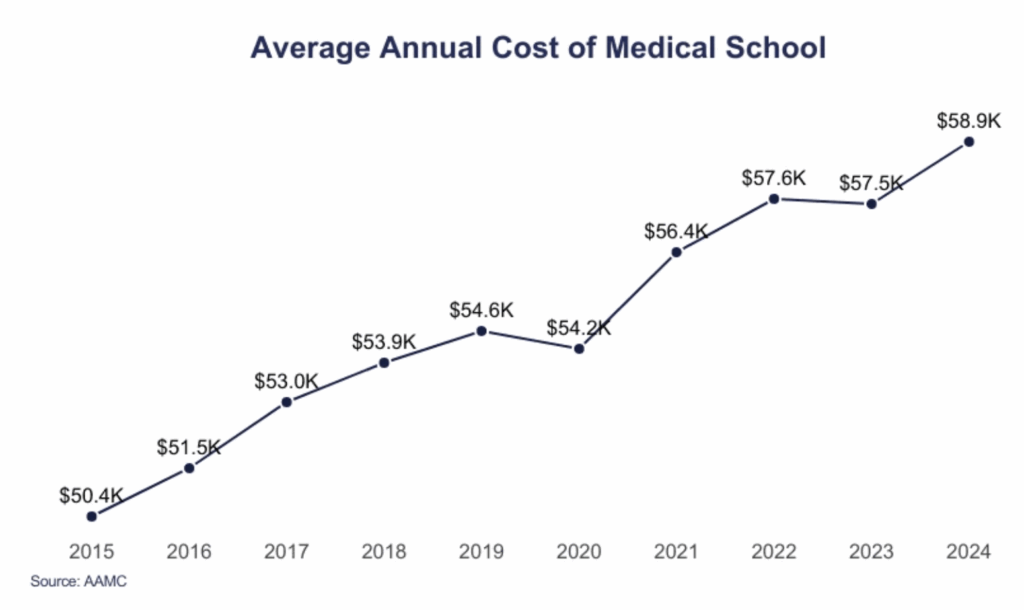

But it hasn’t increased nearly as much between 2013 and now; in fact, it has actually leveled off as a percentage of median household income. More recent data shows a similar trend:

Yes, it seems like a steep line, but tuition and fees have only increased from $50,400 to $58,900 in nine years. That is 1.8% per year. CPI-U rose by 3.1% in those years. If anything, MD schools are CHEAPER now than they were in 2015, adjusted for inflation. This explains the data shown each year in the Graduate Medical Student Survey.

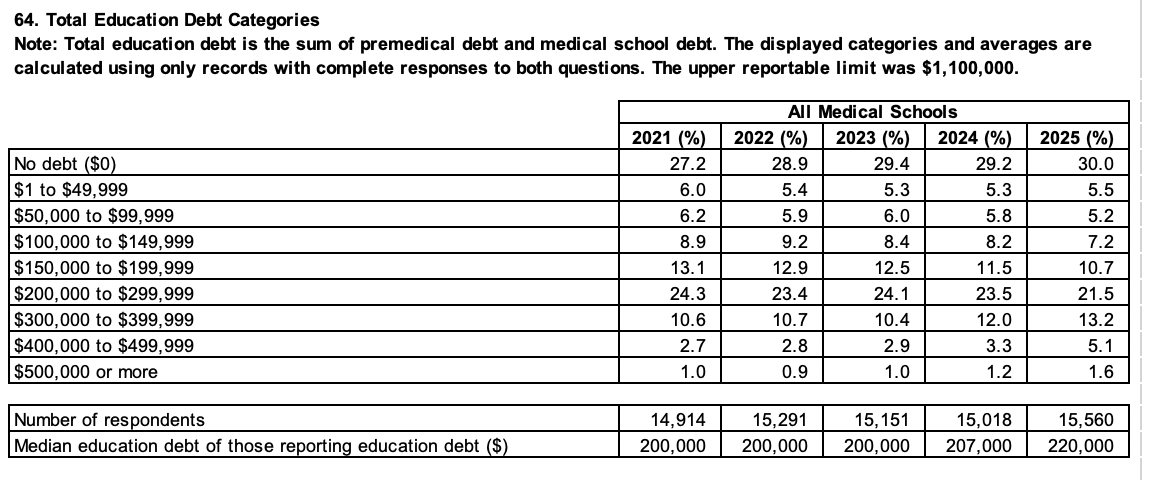

I look at this every year, and for a LONG time (well before 2021) the average debt figure stayed between $195,000 and $207,000. It now stands at $220,000, but the fact remains that borrowing $220,000 to get a job that pays $374,000 a year is a GREAT financial investment. Medical students, at least American medical students, are on average not put under too much pressure.

The situation is even better than these data appear. The general trend from 2013 until the introduction of the OBBBA in mid-2025 was for federal student loan policies to become increasingly generous. Interest rates fell precipitously, at least until 2022. Each new IDR that came was more generous than the last. When SAVE was implemented, it was so good for borrowers that the states panicked and took it to court (where it lost). Perhaps 50% of indebted physicians take a job after training, at least for a few years, that qualifies for Public Service Loan Forgiveness (PSLF). The pandemic-induced student loan holiday turned student loans from a burden to a tailwind with no payments required for 3.5 years and 0% interest. Some people received PSLF without ever paying even a five-figure total on their student loans.

On average, physicians were not pressured by declining incomes and rising education costs. I was wrong. I projected the current trends from then into the future, and the future was nothing like the past. Now the pendulum has swung back a bit with OBBBA. The Repayment Assistance Plan (RAP) is not nearly as good as SAVE should have been, and new borrowers will not have the option to pay for the entire medical school with public money. But PSLF was essentially unchanged.

Yet this is not the pressure that doctors feel. There are two sticking points that they really feel like I didn’t write about at all in 2013.

The housing crisis

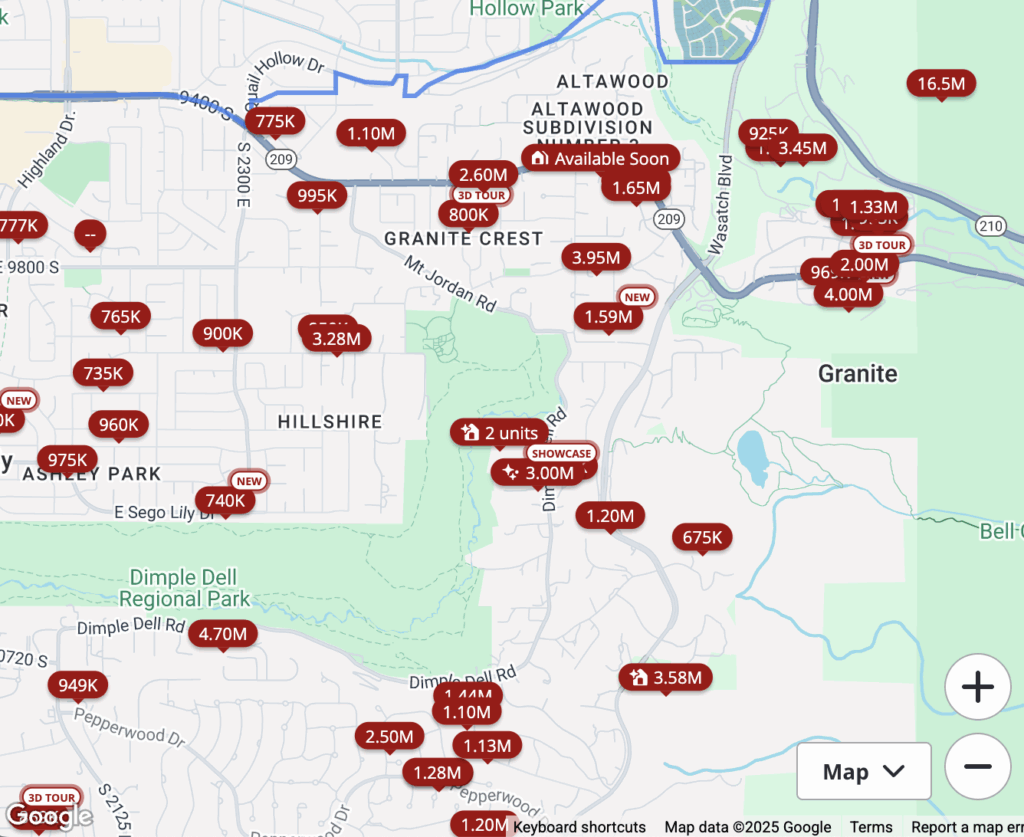

The biggest financial problem in America today is the housing crisis, and doctors are no different. The average home in America now costs more than $420,000. That’s a lot of money when the median household income is only $80,000. Buying a house that costs six times your income is a foolish move. There is also enormous regional and neighborhood variation. In 2010 we bought our house for over half a million dollars. Here is a current Zillow map of homes for sale in the area we looked at in 2010.

In my area, nothing has been listed for a six-figure sum for a long time. And Utah isn’t even really a high cost of living (HCOLA) area. Average home prices in HCOLAs include:

- San Francisco: $1.27 million

- Washington DC: $594,000

- Boston: $780,000

- Manhattan: $1.17 million

And what kind of doctor, who earns in the top 1%-3%, wants to live in the MEDIAN house? The doctors’ houses cost double. At least.

I should have had a chapter in that book that said you should buy your house now, even if you were still in high school. Student loans are not the major problem in most young physicians’ financial lives. Their house/mortgage is.

More information here:

How to buy a house the right way

How to help your child buy a house

The Burnout Crisis

You know what else I missed when I wrote that book twelve years ago? How big would a burnout be. I recently had a conversation with a surgeon almost my age. He was completely burned out and the solution ultimately was a change in employment situation to one where he (and his wife) were paid 1/3 less (at least initially) to regain control of their work environment and leave a toxic work environment. This is not uncommon. It might even be the norm to experience mid-career burnout.

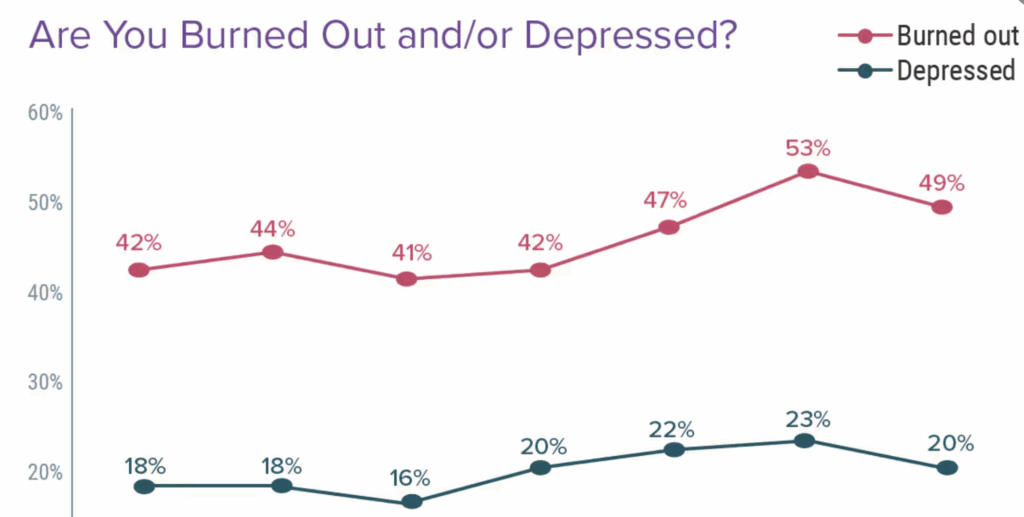

Take a look at this graph from a recent Medscape study.

Burnout is the biggest financial risk to your career. You can insure yourself against disability, but not against burnout. This has become a much broader focus of what we do here at WCI over the past decade. Half of WCICON content is now about wellbeing and burnout, and these are often the best attended and most appreciated sessions.

The bottom line is that the Big Squeeze did show up and it was a good move to be financially prepared for it. But the Great Squeeze wasn’t between income declines and student loans. It was between housing costs and burnout.

What do you think? What have been the biggest financial challenges of your career? How big of a role did maintaining income, dealing with student loans, buying homes and preventing burnout play?

#happened #big #push #White #coat #investor