We trust in gold

With confidence in central financial institutions that are undermined, and with the status of the US dollar as the indisputable reserve currency of the world that is being questioned, it is no surprise that gold is the assets that holds its place in the spotlight.

As Figure 1. The exponential rise in Gold’s price reveals.

Figure 1. Gold price, September 17, 2025. $ USD

Source: Goldprice.org

However, what is surprising is that the question “what supports our currency?” Is not (yet) answered with abstract policy or even digital leds.

And ironically, we owe the revival of Gold to none other than Donald J. Trump, whose unpredictable political and economic maneuvers have shown what once a steady, methodical and somewhat predictable approach to the worldwide financial landscape was in a precarious and unpredictable adventurous ride.

Instead of predictability, decorum and statesmanship, we have a game with high deployment where rates such as Confetti fly, the Echo Echo interest rate via social media and the Federal Reserve (the FED) more is treated as a personal adviser than an autonomous guardian stability guard.

The shift has not yet rattled the stock market, but it has stimulated gold to new heights and has changed it from a nostalgic relic into a must-have hedge against the madness and the depreciation of the US dollar.

Gold’s calm advantage

For many, albeit not all, investors, the counter -intuitive attraction of gold lies in a simple economic truth: it does not pay interest. In contrast to shares that pay for dividends or bonds that offer a yield, gold is simply inert there and unchangeable. It is usually an argument not to possess it in a portfolio – you can’t do anything with it and it produces nothing. And historically this was the heel of Achilles – why hold a bald possession if you could earn a return elsewhere?

What is the Golden of the World worth?

The total amount of mined gold is estimated at 216,265 tons. Converting this into kilograms:

216,265 tons = 216,265,000 kg.

The density of Gold is 19,320 kg/m³. To find the volume:

Volume = mass / density = 216.265,000 kg / 19.320 kg / m³ ≈ 11.194.25 m³.

A cube with this volume would be the same:

Side length = ∛ (11.194.25) ≈ 22.36 meters.

This cube would be about half of the length of a 50-meter Olympic swimming pool or approximately the height of a seven-storey building, or about the length of a standard basketball court.

Its value is around $ 37.2 trillion or US $ 25 trillion. To put that amount in perspective, the estimated value of all real estate from Manhattan in 2021 was US $ 3.5 trillion.

You could possess seven Manhattan Islands’s lettable real estate or a virtually useless, albeit the big cube of gold. What would be the better investment in the next 50 years, taking into account the annual rent increases on the property and no gold income?

Although the long -term arguments against keeping gold are forced, the policy of Gold, the lack of income, has become in -depth in the current environment, has become super power.

Consider the competition: government bonds, especially American treasury. They have long been the favorite choice for “risk -free” return. Investors assign their funds to American treasury for safety and a modest yield. Trump’s persistent campaign to put pressure on the Federal Reserve (the FED) in reducing interest rates – often due to public tirades or the naming of loyalists, in combination with the tendency of his administration to fiscal dissatisfaction and protectionist measures such as reasons that the Netflation has risen the inflation.

The actual yield is the nominal interest rate mining inflation. When Trump’s policy pushes inflation higher-through disturbances of the supply chain due to trade wars or tax reductions in the field of shortage can dive the real yield on a 10-year treasury in negative territory. Giving money to the US government to receive less purchasing power than you started is when looking at your savings in Slow Motion.

In this scenario, gold shines – literally and figuratively. Without proceeds to talk about, the chances of becoming the real proceeds of bonds took negative.

In the meantime, Trump’s interference has eroded the independence of the FED, making monetary policy more like a political football than as a considered aid for economic management. This has dismantled the traditional matter against gold, positioned, perhaps temporarily, as at least one of the logical alternatives to the preservation of wealth.

For many, however, gold is not an investment; It is a statement of skepticism to the ‘system’. Remember that gold is always a bet on fear.

During the era of the seventies, when inflation raged and the real yields became negative, the gold prices shot up from approximately US $ 35 per ounce to more than US $ 800. Nowadays, echoes of that period are in abundance, reinforced by Trump’s playbook. His threats of deeper cuts and unconventional interventions (“Not that I don’t have the right to do something I want to do. I am the president of the United States.”) Have created an environment where investors expect long -term or negative real return. Gold, immune for these manipulations, has at least become the anchoractive for the time being.

Erosion of faith and inflation

The wider storyline is one of decreasing trust in a pillar of the American economy. Central banks must be impartial stewards, economies around crises or through them with data -controlled resolutions. But under the influence of Trump, the FED has been politicized and therefore it has become slightly less ‘less’. It is important that politicization is not hypothetical; It has been manifested in administrative agreements, public criticism and policy pressure that may be seen as priority to self -interest over stability.

When systemically important institutions lose their reliability mantle, at least some investors will be attracted to what they regard as more reliable alternatives. Nowadays that is gold – it is physical, finite and unbound by the whims of the government. Nobody can print anymore, unlike Fiat -currencies that expand by on the

In the meantime, for example, Trump’s tariff wars have exacerbated the tensions of global trade, causing the disruptions of delivery and increased prices. Every new escalation – whether with China, Europe or allies – reduces the predictability of international trade, which means that capital goes to Safer ports.

Moreover, Trump’s social media outbursts act as volatility amplifiers. A single mailrest against the power or hint of the dollar on standard values and currency devaluation can send financial markets in a downward play. Investors, tired of this unpredictability, come to a buffer, a observed refuge.

Consider the increase in stock market-built funds (ETFs) and the physical bullion requirement during Trump’s first term. Data shows that periods of increased trading rhetoric with peaks in gold prices, because uncertainty caused anxiety. By expanding this, under similar influences during Trump’s second term, we were able to see even more pronounced effects, where gold serves as the de facto currencyback stop in portfolios worldwide.

Chaos as a catalyst

They say that there are opportunities during the disorder, and for gold lovers, the Trump Chaos brand has been a real gold mine – word play. Any impulsive decision – from withdrawal from trading spacts to questioning alliances – injects uncertainty.

Gold thrives on fear. It is the ultimate opponent of ‘assets’: when faith in paper assets decreases, the allure of the metal becomes deeper. Trump’s approach has unintentionally created a perfect storm. By challenging the standards of the central bank, he has made gold look like the adult in the room. In the midst of a landscape of manipulated interest rates and balloon fern debts, the scarcity and history of Gold return as reasons to believe in Gold’s status as a value storage.

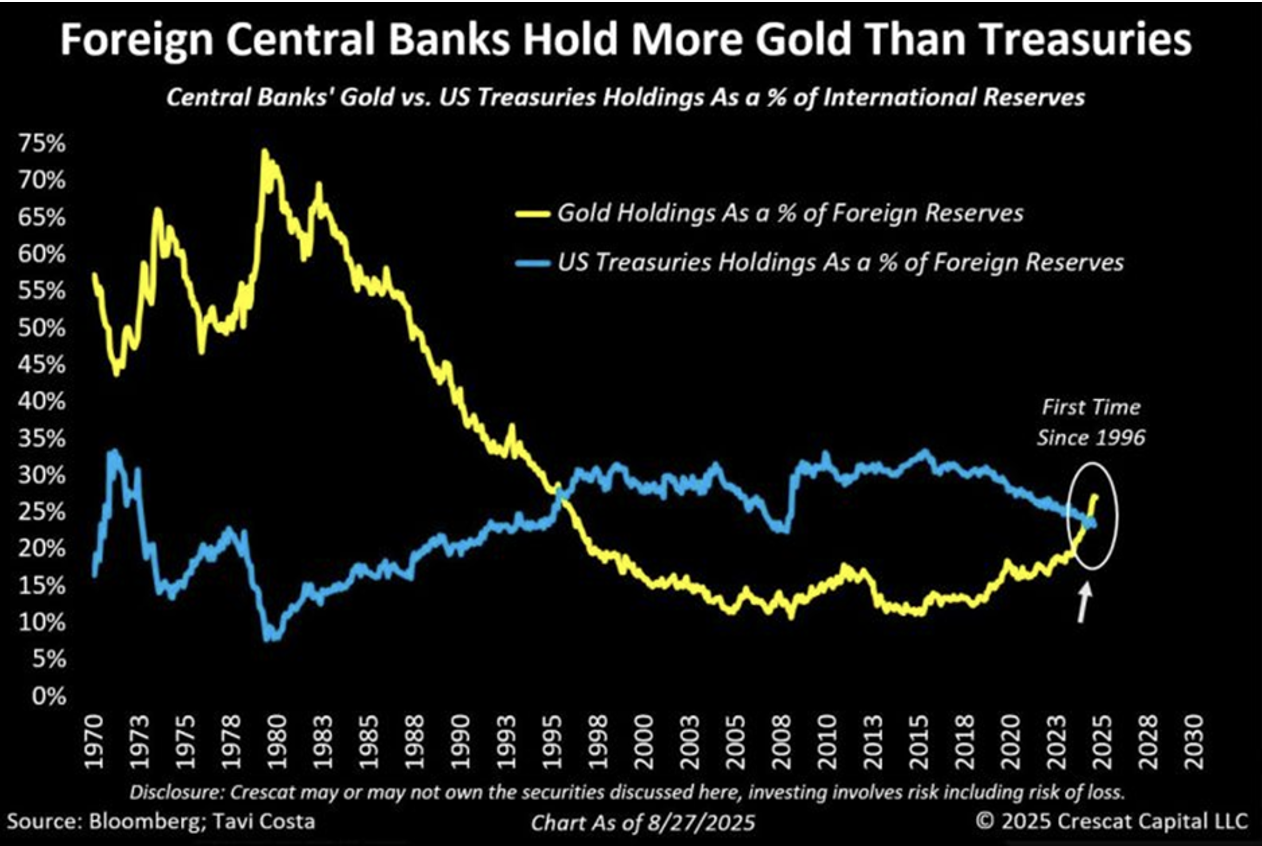

The increasing interest in gold is not the exclusive domain of individuals. Trump’s “America First” attitude has tense alliances and promoted a multipolar world where nation states hamster gold as a hedge against the decreasing dominance of the US dollar. Central banks in countries such as Russia and China have performed their gold reserves, partly in response to observed American unpredictability.

As Figure 2., reveals, foreign central banks now have more gold than American treasury.

Figure 2. Foreign central banks have more gold than treasuries

Source: Bloomberg

This global shift strengthens the role of gold and creates a self -fulfilling prophecy in which the demand stimulates prices higher.

A new era?

I remain married with the idea that in the long term other traditional and income -producing assets exceeds than gold. But that does not reduce its potential tactical role in a portfolio.

From the uncertainty that keeps us alert, to the policy that spectacle gives priority over stability, and to the roller coaster of Donald J. Trump, there is a multiple of reasons to explain the record price of Gold.

At least for now, that heirloom jewelry or forgotten coin collection is not only sentimental – it is tactical. Gold may not be rich quickly, but it may help to tolerate the unpredictable. And while institutions are faltering under political pressure, gold may offer safety.

Whether you are an experienced investor or just a curious observer, the message is clear: Gold’s shine becomes brighter in a world where trust is being affected.

Roger Montgomery is the founder and chairman of Montgomery Investment Management. Roger has more than three decades of experience in fund management and related activities, including stock analysis, stock and derivative strategy, trade and effects. Prior to the establishment of Montgomery, Roger positions in Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also the author of the best -selling investment guide for the stock market, value. Aabel-Hoe to appreciate the best shares and buy them for less than they are worth.

Roger regularly appears on television and radio, and in the press, including ABC Radio and TV, the Australian and Ausbiz. View upcoming media performances.

This message was contributed by a representative of Montgomery Investment Management PTY Limited (AFL No. 354564). The main purpose of this message is to provide factual information and not to provide financial product advice. Moreover, the information provided is not intended to give a recommendation or opinion about a financial product. However, each comments and opinion of opinion can only contain general advice that has been drawn up without taking into account your personal objectives, financial circumstances or needs. Therefore, before acting on the basis of one of the information provided, you must consider the suitability in the light of your personal objectives, financial circumstances and needs and you must consider requesting independent advice from a financial adviser if necessary before you make decisions. This message excludes specific personal advice.

#trust #gold