- Tokenized U.S. and non-U.S. government bonds added $2.12 billion in market capitalization in the first two months of 2026, while stablecoins lag behind with an increase of $1.19 billion.

- The first quarter of 2026 is already on track to be the strongest quarter for tokenized treasuries ever.

- Yield-bearing stablecoins will dominate stablecoin supply growth in 2026, partially offsetting the multibillion-dollar losses of USDT and USDC.

Stablecoins have historically dwarfed tokenized treasuries by most measures, with their quarterly supply expansion regularly reaching tens of billions. However, in the first quarter of 2026 so far, the tokenized treasury market has increased $2.12 billion in market capitalization, while stablecoins just added $1.19 billion. For the first time, tokenized treasuries are growing faster than stablecoins in absolute terms.

So what has changed?

Note: Q1 2026 data runs through February 24, 2026.

The market became cautious and returns became the answer

Crypto markets are going through a rough patch and investors are responding by opting for assets that offer more stability and predictable returns. Tokenized government bonds fit that profile almost perfectly: they are backed by US government bonds and generate real interest rates, which have even increased slightly this year.

Tokenized government bonds are currently listed eight consecutive quarters of expansion. Furthermore, even though we are only halfway through the quarter, The first quarter of 2026 is already on track to be the strongest quarter for tokenized treasuries ever. This indicates that demand is not only continuing, but also increasing.

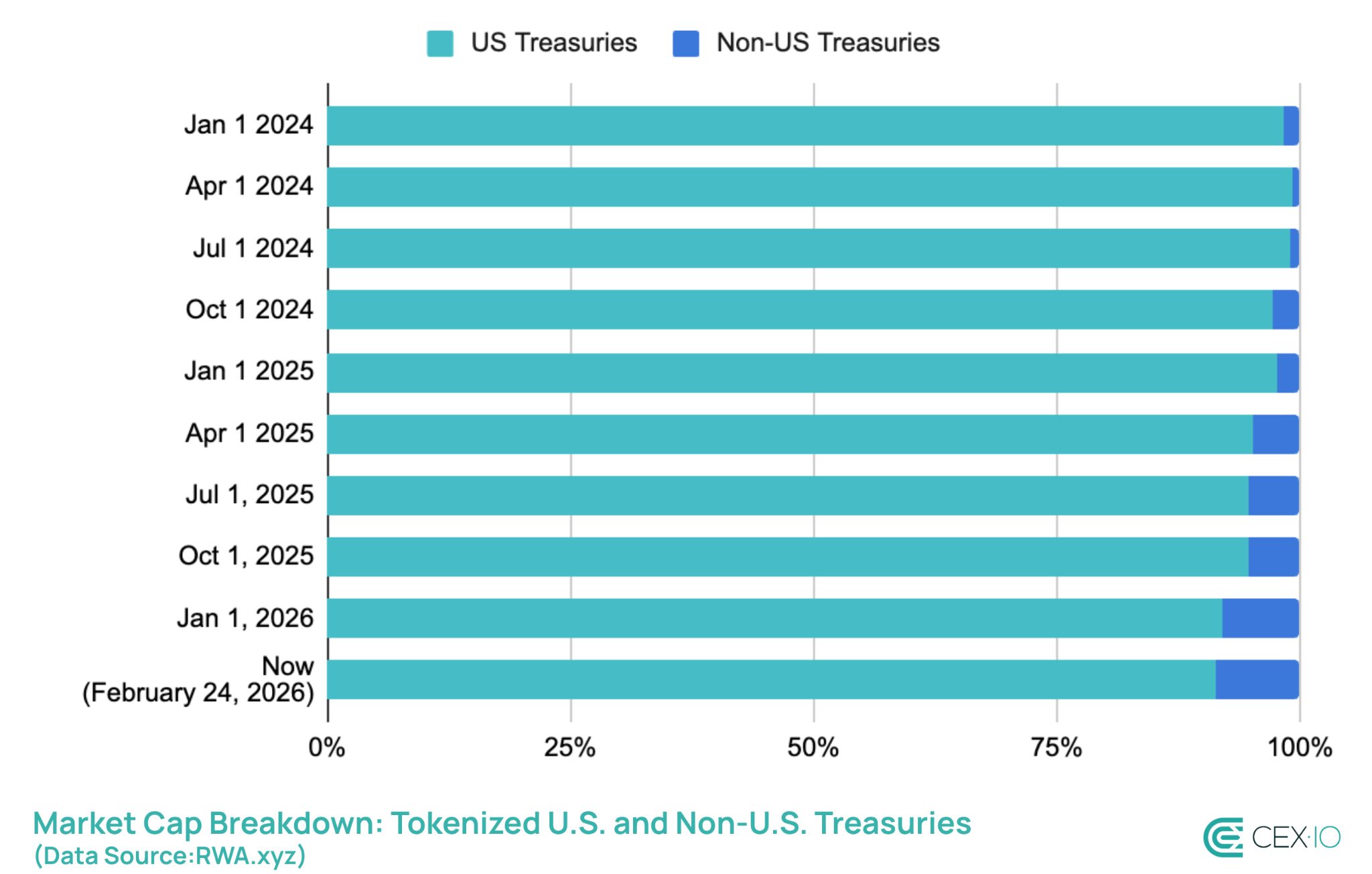

As such, tokenized US government bonds have grown since early 2024 $750 million until almost $11 billion – an increase of about 15x. Non-US Treasuries followed a similar trajectory, of just $13 million to beyond $1 billion during the same period.

Non-US Treasuries in particular have steadily increased their footprint in the tokenized treasuries market. Their share of total market capitalization has grown from roughly 1% two years ago to almost 9% today, signaling a gradual diversification away from US bonds.

The supply of stablecoins is also shifting towards returns

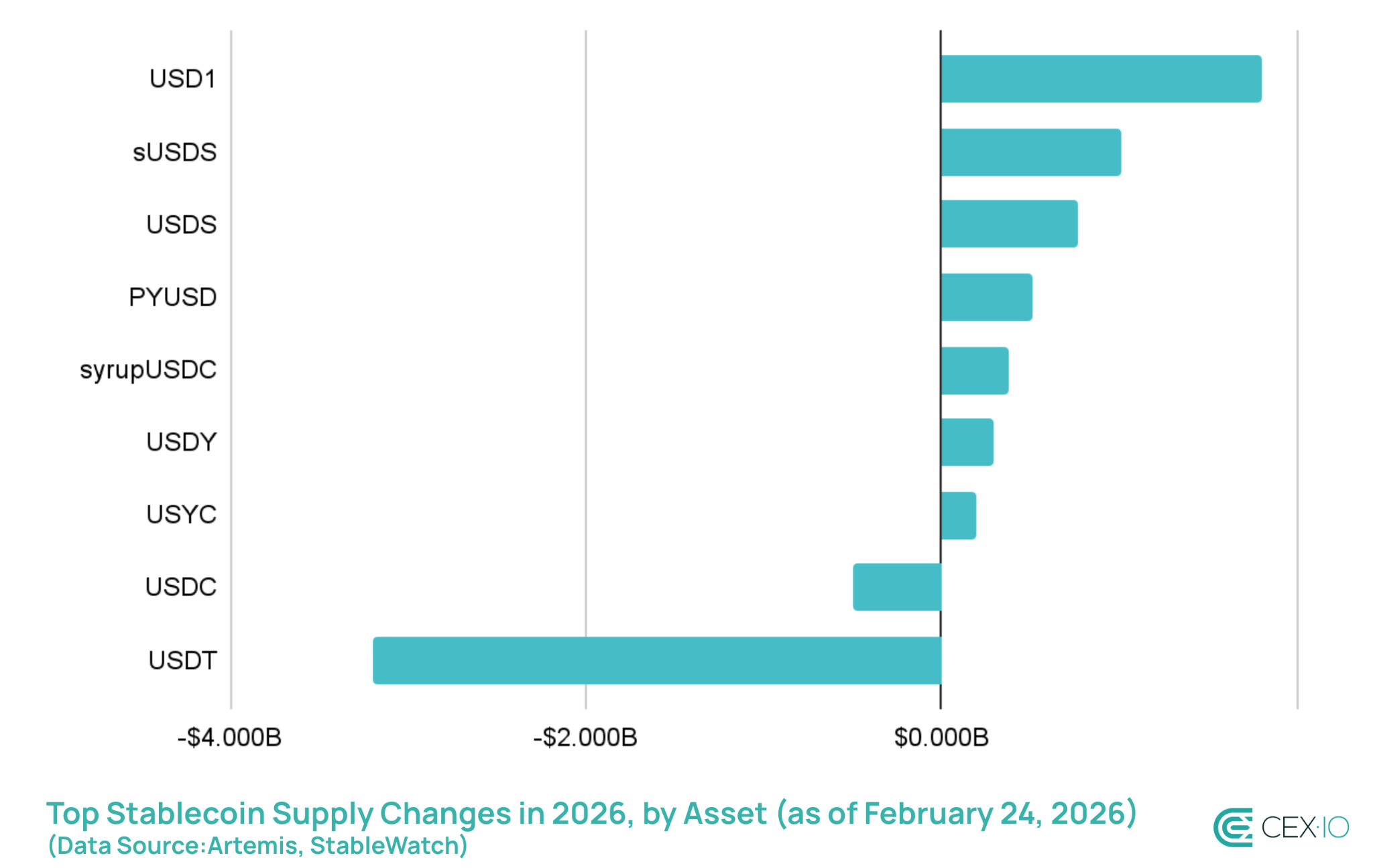

The supply of stablecoins is currently showing the worst dynamics in years. In the first two months of 2026 Ethereum has already lost more than $8 billion in stablecoin supply – the worst performance since the second quarter of 2022. In turn, USDT and USDC have lost $3.2 billion and $0.5 billion in supply so far this year, respectively.

Under conventional measures, this would be a sign of a sector in retreat. But the total supply of stablecoins has hardly changed in total, because the market is restructuring around returns.

Among the stablecoins that posted the largest absolute supply gains in 2026 were yield-bearing assets such as USDY, sUSDS, USYCAnd syrupUSDC leads the pack. Other top performers are also closely linked to return-generating mechanisms. USDSfor example, largely serves as an entry point to sUSDS, while USD 1 has benefited from the launch of World Liberty Markets, expanding its DeFi utility and access to yields. So even if the return is indirect, it clearly drives adoption.

Overall, the yield-bearing stablecoins showed a 5% have increased so far in 2026 and have currently become the best performing segments in the stablecoin sector.

What this means for the industry

During bull markets, stablecoins thrive as liquidity vehicles, on the sidelines of active speculation. In a more cautious environment, idle capital comes at a price, and protocols and users alike are looking for on-chain tools that work harder. If bearish conditions persist, yield-bearing stablecoins and tokenized treasuries are well positioned to continue growing as investors look for stability and consistent returns.

The growth of yield-bearing assets is already registering outside the crypto markets. In Washington, returns on stablecoins have risen become one of the more controversial topics in ongoing US crypto legislation. Specifically, the issue is whether centralized exchanges are allowed to pay out returns on stablecoin balances, a model that banks see as a direct threat to their depository activities. That debate is narrower than what the DeFi-native yield products covered here represent, but reflects the same underlying shift: crypto asset returns are no longer a niche feature, they’re becoming an expectation – and one that the traditional finance industry is taking seriously enough to push back through legislation.

The web content provided by CEX.IO is for educational purposes only. The information and tools provided are not, and should not be construed as, an offer, or a solicitation of an offer, or a recommendation, to buy, sell or hold digital assets, or to open a particular account or to adopt a specific investment strategy. The digital asset markets are highly volatile and can lead to monetary losses.

The availability of the products, features and services on the CEX.IO Platform is subject to jurisdictional restrictions. To understand what products and services are available in your region, please see our list of supported countries and territories. This page contains additional links to information about individual products and their accessibility.

#Tokenized #Treasuries #Outpace #Stablecoin #Growth