A reader asks:

Investors have been concerned about the concentration in the stock markets for years. The S&P 500 is becoming increasingly concentrated, but the largest stocks also have the fundamentals to support it. How does this resolve itself? Or do you think a more concentrated stock market is the new normal?

Concentration has been a top priority for many investors for some time.

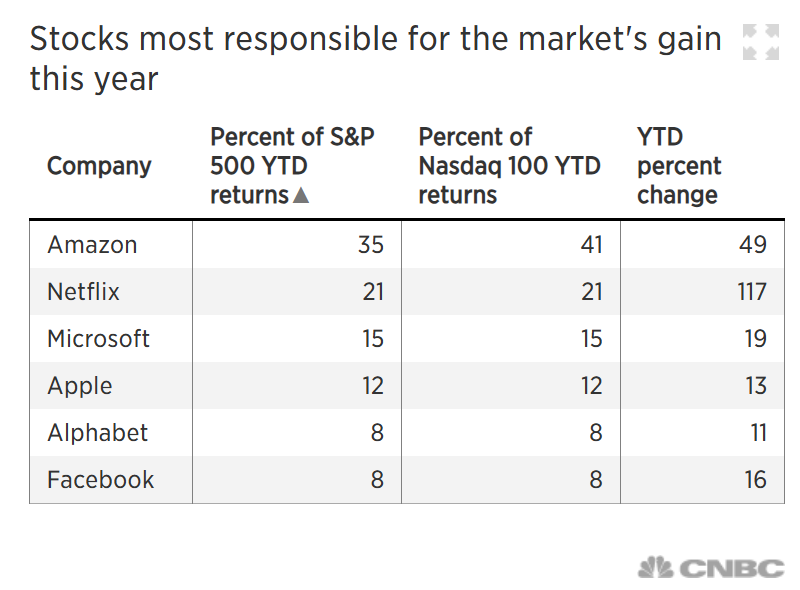

I first wrote about this topic in the summer of 2018. In that piece I referenced this story from CNBC:

Take a look at the companies they listed that year in terms of concentrated profits:

Those names sound familiar to me. The only big difference is that today you can trade Nvidia for Netflix.1 Investors were concerned about the concentration of technology stocks at the time and are still concerned today.

What if this is just the new normal for a while?

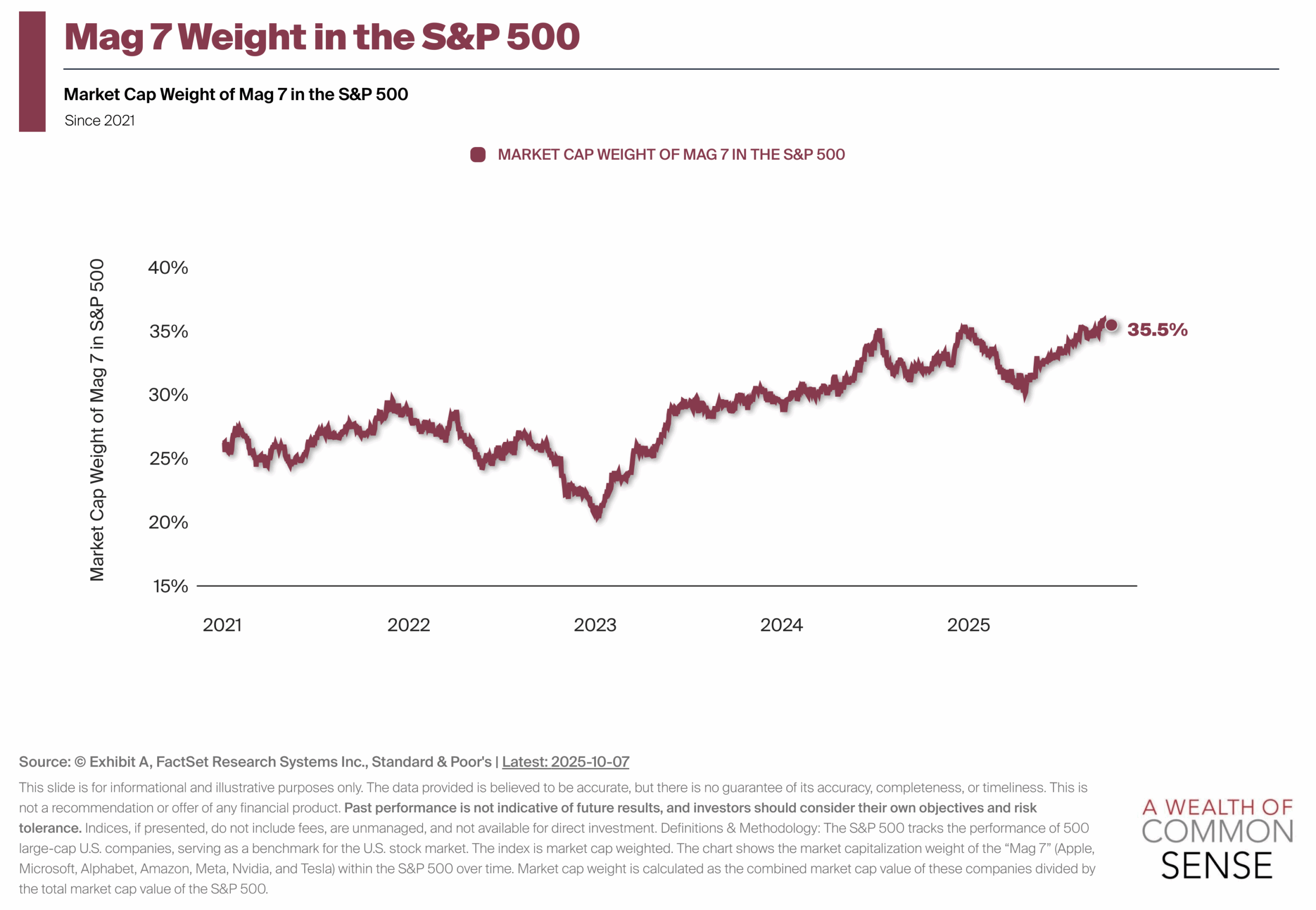

The Mag 7 continues to gobble up the stock market:

The bigger these companies get, the greater the impact they have on stock market returns.

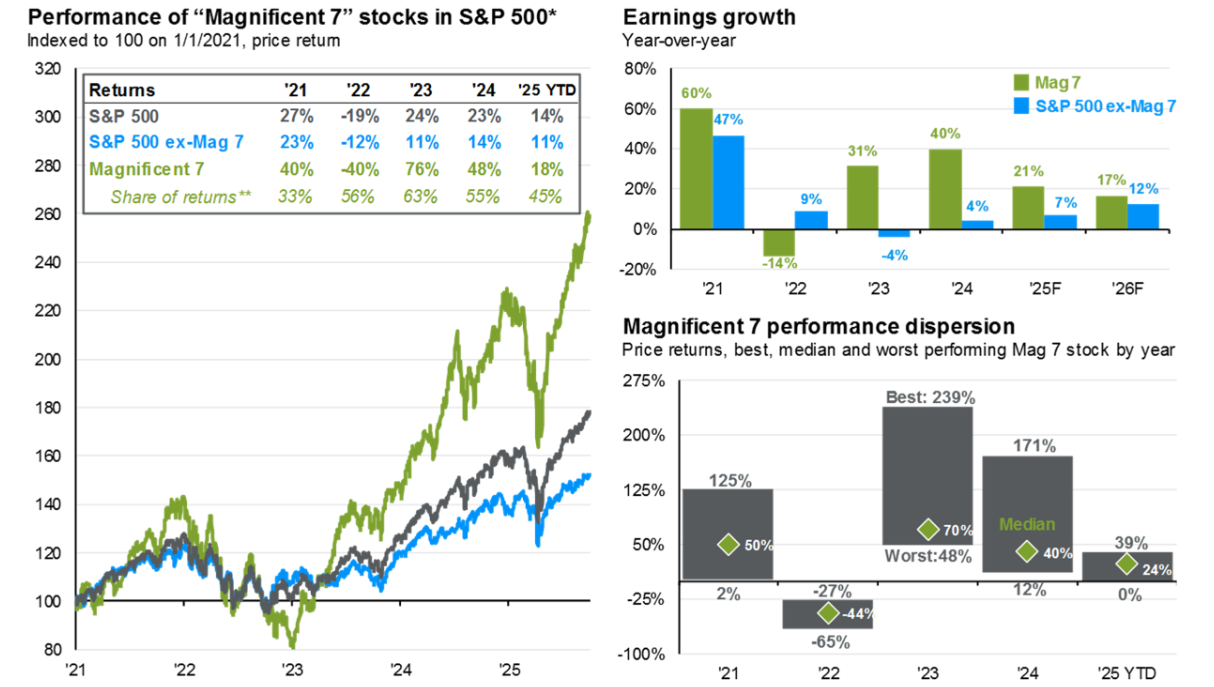

Here’s a good one JP Morgan shows the Mag 7’s contribution to performance and fundamentals:

The share of returns and earnings growth in the hands of a few companies seems unlike anything we’ve ever seen.

So how does this end?

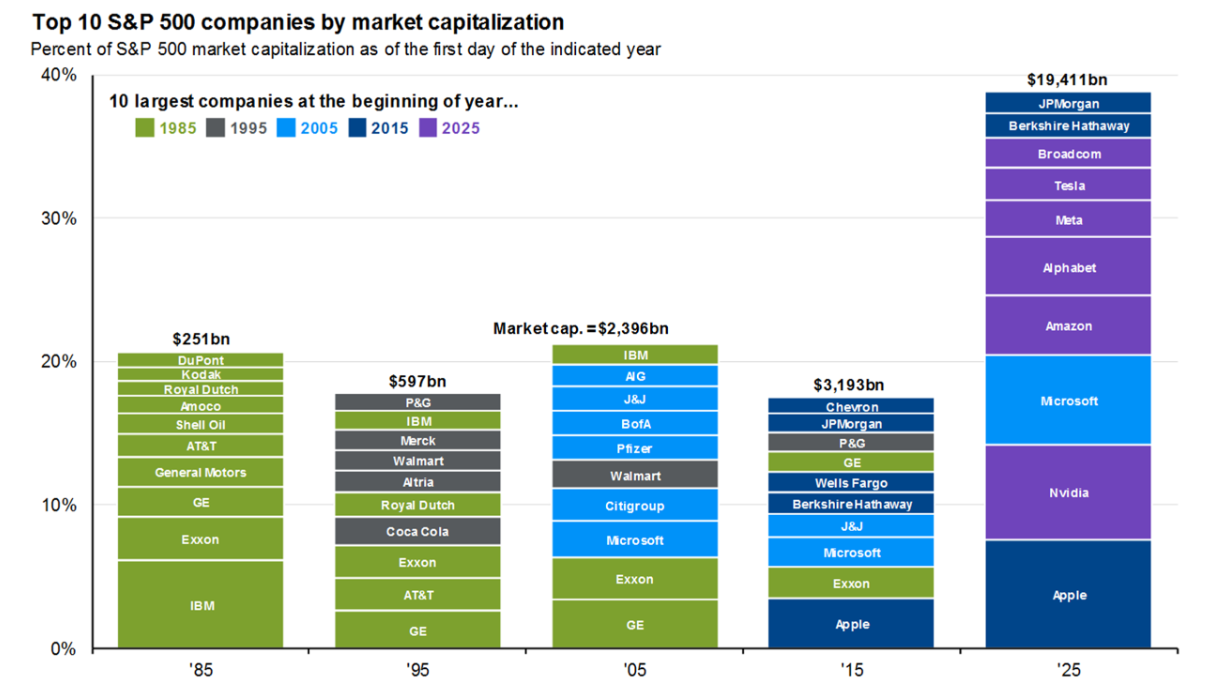

JP Morgan has another good one that shows the changes in the names in the top 10 stocks every 10 years, going back to the mid-1980s:

Microsoft is the only member of the current top 10 that was there in 2005. Turnover is the norm for the big names, even though there are stocks that stay there for years. The attrition rate is about 30-40%, or 3-4 names, every 5-10 years over the past 50 years.

That’s one way this thing could turn out. We could see some of these big stocks faltering or new entrants taking their place. We could also see the AI bubble burst in the coming years, which could do some damage to these big tech stocks.

But that does not necessarily mean that market concentration will automatically disappear.

Jurrien Timmer has this great chart that looks at the weights of the 50 largest stocks in the S&P 500, along with the other 450 names going back to the early 1960s:

He explains:

It’s worth remembering that while the top-heavy concentration was quickly reversed in the late 1990s and early 2000s, the market remained top-heavy for years in the 1950s and 1960s before excessive valuations eventually took their toll. This may take some time.

After the internet crisis, concentration was removed from the stock market, but in the 1960s and 1970s there was a longer period in which the largest shares dominated.

There are reasons to believe that we have been in a new normal of stock market concentration at the top for some time now.

The big tech stocks are so entrenched in our lives that the government wants nothing to do with breaking them up. And every time a new competitor emerges, these companies use their war chests to buy up the competition.

These companies now have huge moats around their businesses, high profit margins and produce insanely high cash flows.

I’m not saying these stocks will outperform forever. They won’t do that. And some of them will definitely drop out of the top 10.

But don’t be surprised if we’ve entered a new era where the stock market remains concentrated at the top.

Wealth inequality in the stock market is likely to persist.

Jurrien joined us this week on Ask the Compound to help answer this question:

We also covered questions about why the stock market isn’t worried about a slowing labor market, why international stocks are outperforming, why gold is up 50% this year, and how the AI boom will end.

Further reading:

Concentration on the stock market

1Netflix is just outside the top 10. According to the latest data, it is the 13th largest stock in the S&P 500 by market capitalization.

This content, which contains safety-related opinions and/or information, is provided for informational purposes only and should not be considered professional advice or an endorsement of practices, products or services in any way. No representation can be made that the views expressed here will apply to any particular facts or circumstances and should not be relied upon in any way. You should consult your own advisors on legal, business, tax and other related matters relating to investments.

The comments in this “post” (including any related blogs, podcasts, videos and social media) reflect the personal opinions, views and analyzes of the Ritholtz Wealth Management employees providing such comments and should not be construed as the views of Ritholtz Wealth Management LLC. or its respective subsidiaries or as a description of advisory services provided by Ritholtz Wealth Management or performance returns of a client of Ritholtz Wealth Management Investments.

References to any securities or digital assets, or performance data, are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. The charts and graphs provided herein are for informational purposes only and should not be relied upon in making any investment decision. Past performance is not an indication of future results. The content is only valid from the date indicated. Any projections, estimates, forecasts, objectives, prospects and/or opinions expressed in this material are subject to change without notice and may differ from or conflict with the opinions of others.

The Compound Media, Inc., a subsidiary of Ritholtz Wealth Management, receives payments from various entities for advertising in affiliated podcasts, blogs and emails. The inclusion of any such advertisements does not constitute or imply any endorsement, sponsorship or recommendation thereof, or any association therewith, by the Content Creator or by Ritholtz Wealth Management or any of its employees. Investing in securities involves the risk of loss. For additional advertising disclaimers see here: https://www.ritholtzwealth.com/advertising-disclaimers

See disclosures here.

#normal #stock #market #concentration #wealth #common #sense