Now, here’s today’s article:

I’ve struggled with this concept. I’ve seen many others struggle with it too.

Step 1: We discover a new shiny idea (…Roth Conversions! …Value investing in small caps! …Qualified Charitable Distributions!)

Step 2: The shiny appeal of this idea catapults it to the top of our priority list.

Step 3: Blinded by the light, we wrongly place too much emphasis on this new idea, at the expense of the big picture.

In various fields this is called a “novelty effect” or “novelty bias.” It also has implications for long-term investors and do-it-yourself financial planners, who are thinking about retirement and other long-term goals.

What if instead we had a simple, prioritized list of ideas that long-term investors should consider? Something that sweeps away prejudices and goes straight to the facts. We need a ‘sequence of actions’ that ensures you focus on the most important things first, for to come up with the shiny new idea.

Mathematics has ‘PEMDAS’.

Have personal finances “FOO” – the “financial sequence of operations.”

And what we’re going to do here is ‘FOO-adjacent’, but much more specific long-term investors, retirement planning and portfolio construction.

The trading sequence of the long-term investor

I believe that if you follow this list in orderyou will be a better long-term investor. Do not expend too much energy on a lower topic until all higher topics have been fully covered.

Step 1: Invest

I know, I know… we start with a stunning revelation: the most important step in investing is ‘investing’.

But the truth is that many people get caught up in small details before they are invested enough to make those details matter. Your stock/bond allocation doesn’t matter if you only have $100 in an account. The biggest dial you can turn is how much you decide to invest.

Consider making consistent investment deposits over time (a.k.a “dollar cost averaging.”). Focus on your savings rate, lifestyle inflation and career capital.

Step 2: Control your temperament

Warren Buffett said:

“Once you have ordinary intelligence, you need the temperament to control the tendencies that get other people into trouble in investing.

Despite what many people think about investing, behavior dominates mathematics. Simple steps, such as automated investing and rules-based rebalancing, can be critical. We all have biases (loss aversion, recency bias, anchoring) that can derail us.

Long-term returns are achieved by staying invested through crashes, avoiding panic selling, avoiding speculative manias, thinking long term, and choosing process over prediction.

The math is simple. Managing the broad spectrum of human emotions is a much greater challenge.

Step 3: Risk assessment and asset allocation

Asset allocation describes splitting your portfolio across broad asset types such as stocks, bonds, real estate, cash, etc.

Determining appropriate asset allocation is related to your personal time horizon and “need, ability and willingness” to take risks. Then you must adjust your asset allocation accordingly.

Your asset allocation explains an overwhelming portion of your total returns. In other words: your choice to invest in, for example, 80% shares versus 60% shares far more consequence then which one stocks (also called “security selection”) that you choose.

Asset Allocation >>> Security Selection.

Step 4: Broad diversification

Next, you need to broadly diversify your Asset Allocation percentages.

For example, stocks can be diversified across geographies, across sectors, across company sizes, etc.

Diversification reduces portfolio volatility, protects against significant losses if one investment fails, and ensures that long-term returns are not dependent on the performance of a single security or sector.

This broad diversification ensures a better risk-adjusted return.

Step 5: Cost control

Investing is not free. Costs are essential to understand.

Every little cost counts, and those costs add up over decades. You need to understand your expense ratios (i.e. the cost of funds), advisor fees, commissions and trading costs, and other places you pay to invest.

But it is still true that:

“Cost is what you pay, value is what you get”

The costs are only half of an important part. Value is much harder to measure, but just as important to understand.

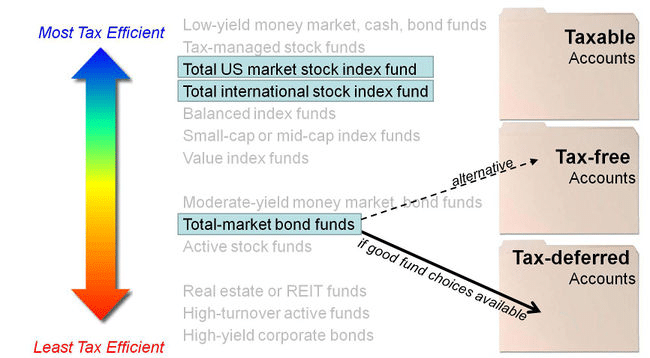

Step 6: Account selection + tax location

Different investment accounts have their own pros and cons. Examples include 401(k) and IRA (Traditional vs. Roth versions of these accounts), Health Savings Accounts (HSA), taxable investment accounts, children’s accounts (529, UTMA/UGMA, Trump).

These accounts are taxed differently. Some accounts allow tax-free contributions or withdrawals. Some accounts allow tax-free growth each year. Some accounts are subject to capital gains taxes.

A general rule of thumb is that “tax diversification” is useful in retirement because it allows the investor to respond dynamically as tax laws change.

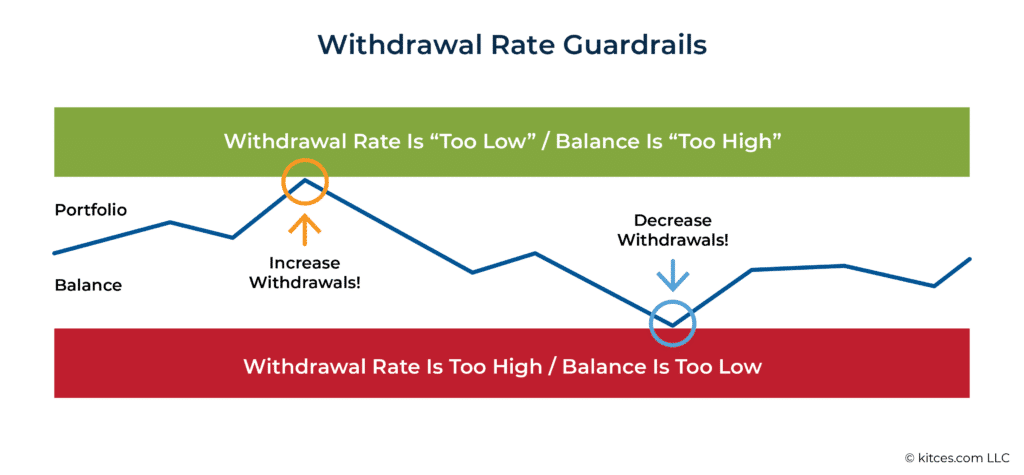

Step 7: Recording Optimization

Building a good portfolio is a separate skill set from withrowing away money (e.g. upon retirement). You follow steps 1-6, but undo that good work with recording errors.

Investors (especially those investing for personal reasons) have many tools at their disposal to help plan withdrawals.

Common examples include a “safe withdrawal rate” framework, dynamic spending rules, withdrawal guardrails, sequencing risk mitigation, and “bucketing” different withdrawal amounts versus a total return approach.

Step 8: Legacy, donation and capital transfer

From #7 onwards, any money not withdrawn is donated, transferred or left to heirs.

A good estate plan, a lifetime giving strategy, and charitable planning are all important parts of a long-term investment plan.

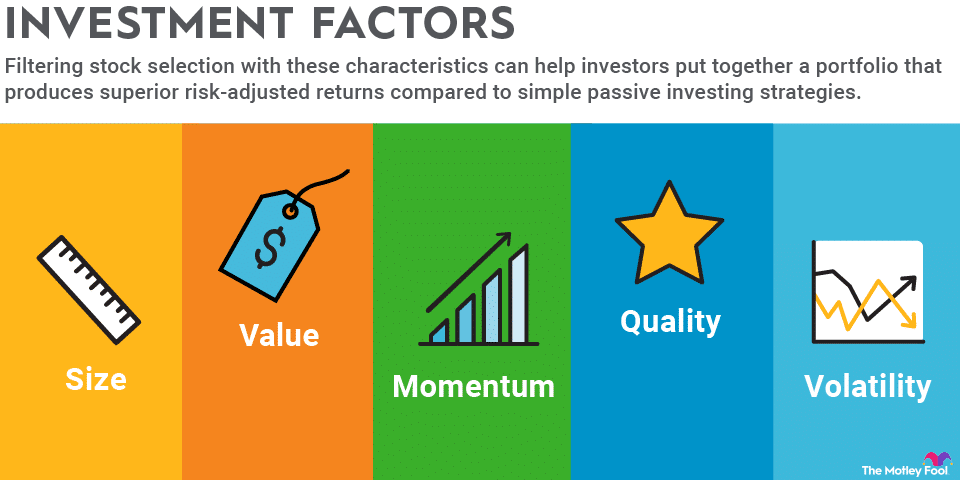

Step 9: Security Selection, Factors and Tilts

There is a good reason for a basic asset allocation Step #3and there must be broad diversification Step #4. They are that important. But investing involves more than just these two ideas.

“Security selection” is the process of choosing individual investment products. Are you investing in Apple, a broad stock index fund or an energy company investment fund? That’s a safety selection decision.

“Factors” are broad, evidence-based characteristics of securities that have historically been associated with differences in long-term returns. Examples include value (cheap versus expensive), size (small versus large companies), profitability, and momentum. Tilting your portfolio toward any of these factors can be an impactful decision.

Step 10: Tactical Tax Optimization

Many investors find small opportunities to reduce their lifetime tax bill without changing the course of their overall investment journey. Everyone pays taxes. But you do not have to pay more tax than you are obliged to.

Specific common tactics include Roth conversions, tax loss and tax gain harvesting, and optimizing the location of assets between accounts of different tax status.

Smart tax planning connections.

Step ‘Never’: neutral or downright negative behavior

That leaves us with many all-too-common behaviors that, overall, are a net negative for long-term investors. Behavior such as:

- Market timing.

- On the hunt for hot stocks.

- Economic forecasts and other macroeconomic forecasts

- Political adjustments (e.g. changing your portfolio due to political hopes or fears)

The order is important!

You might read the list and think:

- I need to focus on my shooting strategy!

- Factors! Sounds interesting. I should investigate that.

- Yeah, that guy on the radio was talking about “Roth conversions,” and it was on my list.

Certainly. Those things are part of the process. But I would call these three activities #7, #9, and #10 respectively. There are much more effective ways to spend your time and energy!

If you are participating in this long-term investing journey, I recommend that you go through this “sequence of long-term investing activities.” in order.

Manage every step in order and enjoy investing!

Thanks for reading! Here are three quick notes for you:

First – If you enjoyed this article, please join the thousands of subscribers who read Jesse’s free weekly email, where he sends you links to the smartest financial content I find online every week. 100% free, you can unsubscribe at any time.

Second – Jesse’s Podcast “Personal finance for long-term investors” has grown ~10x in recent years and now helps ~10,000 people per month. Tune in and check it out.

Last – Jesse works full time for a fiduciary asset management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free consultation with Jesse to see if you are a good fit for his practice.

We’ll talk to you soon!

#longterm #investors #trading #order #interest