After a sharp decline in the first quarter, the Sentiment Index of the CRE Finance Council Board of Governors rose to 112.3 in Q2 from 87.9, back above the neutral 100 -based line. The increase of 27.8 percent marks one of the strongest quarterly improvements in the history of the index.

The rebound in the total 2Q index followed a decrease of 30.5 percent in the first three months of the year. That was the second largest drop ever, only surpassed at the start of the pandemic in early 2020.

A dramatic shift in sentiment

The second quarterly study, conducted from July 8 to July 22, showed a “dramatic shift in sentiment when market participants adapted to the developing economic landscape and renewed optimism in stabilizing the expectations of the rental lines and improving capital market conditions.”

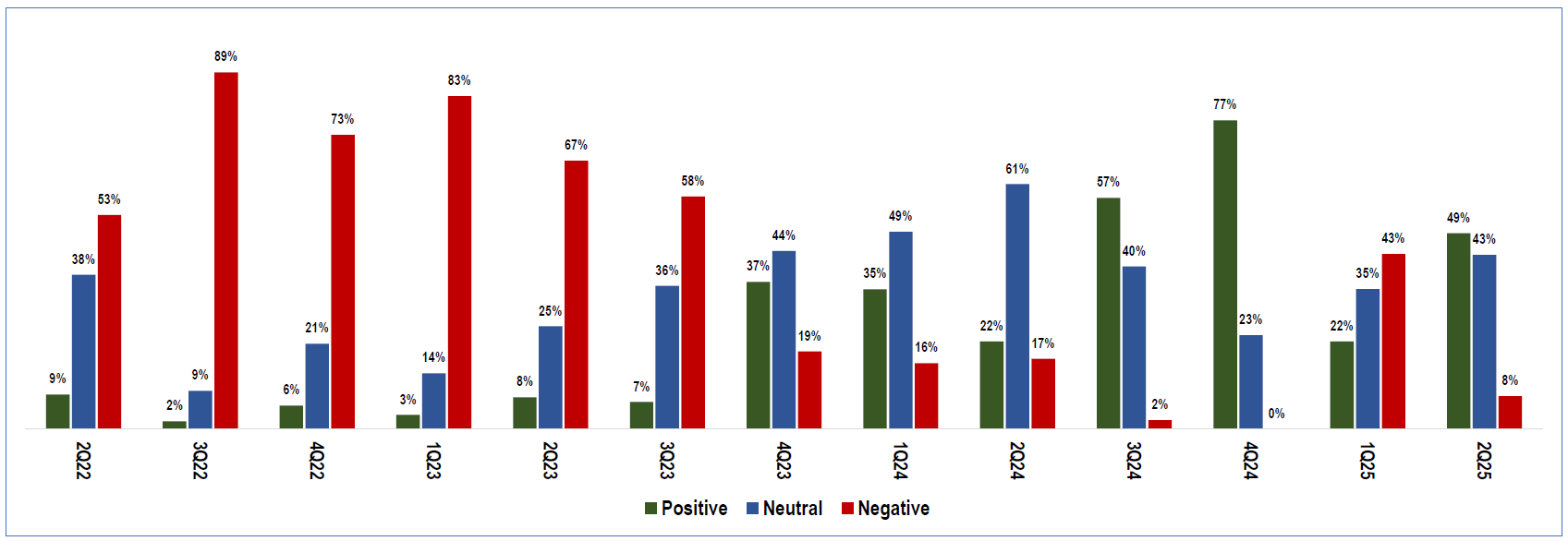

The general prospects of the industry showed a robust recovery of the first quarterly survey, with 49 percent who expressed a favorable picture for cre-financial companies in the coming 12 months, an increase of 22 percent in 1q. Only 8 percent remained negative, a decrease of 43 percent in the previous quarter.

Lisa Pendergast, President and CEO of CREFC, said in prepared comments that the change in the index emphasizes the resilience and adaptability of the cre -finance industry. While the challenges remain, the market recovers its foot, she noticed.

The BOG index is intended to measure quarterly-to-quarter shifts in market conditions and prospects. In one of the most meaningful reactions, 71 percent of governors reported that the hunger of their company for new CRE -Loanen or investments is increasing moderately or considerably for the second half of 2025.

Most important index height points

In one of the most important key questions, sentiment became positive, in which only 27 percent of the respondents expected economic conditions to deteriorate in the coming 12 months. That is a dramatic improvement compared to the first quarter, when 80 percent of the respondents expected the US economy to see deteriorating circumstances compared to the previous 12 months. This time the majority (54 percent) expect it to remain the same and 19 percent anticipate improvement.

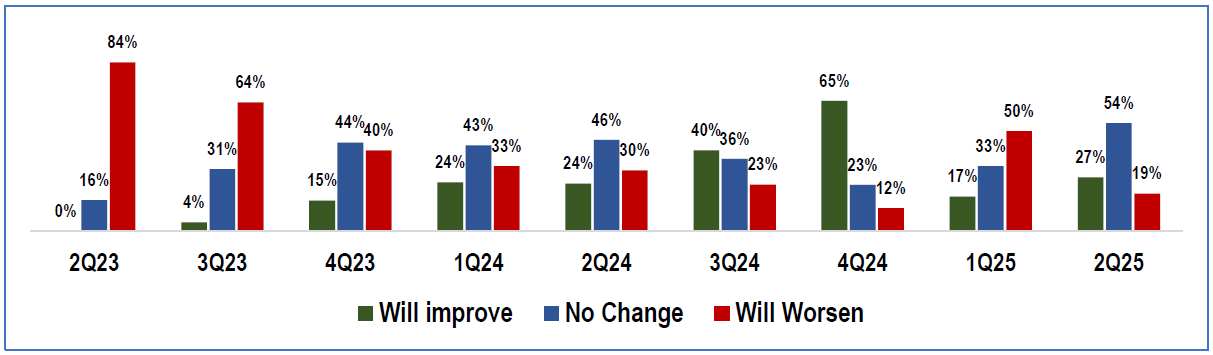

The outlook for cre-basic principles are stabilized in the second quarterly study with 81 percent who provided Fundamentals to improve or remain the same and only 19 percent of the respondents who expect deteriorating circumstances, decrease of 50 percent in Q1.

The board was described as an exceptional bullish about the financing question, in which 86 percent of the respondents expected an increased demand for the borrower, an increase of 48 percent in 1q, and none of the respondents who expect less requirement.

The survey also indicates a sharp rebound in buyer’s activity for cre- and multi-family assets in the coming 12 months after a soft first quarter. Expectations almost doubled, with 65 percent of respondents who predict more demand, an increase of 35 percent in the first quarter, and only 3 percent expect less demand, compared to 20 percent in the previous survey.

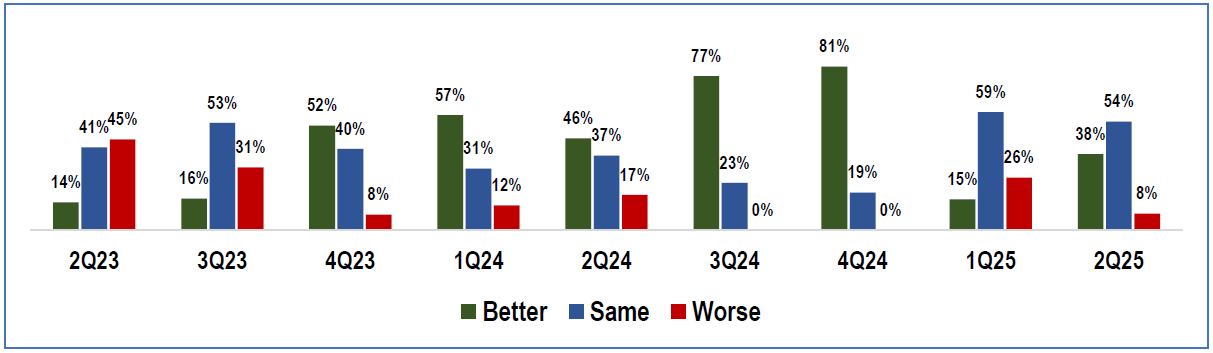

With transactions that are expected to increase and the borrowers return, the respondents also had more faith in market liquidity. In the coming 12 months, 92 percent better or the same liquidity, an increase of 74 percent last quarter expects, with only 8 percent those worse conditions. That is a decrease of 26 percent in 1q.

Although the Federal Open Market Committee refused to reduce the rate of the benchmark federal funds and to keep it between 4.25 percent and 4.5 percent on a range, the respondents reflected a growing belief that the rate environment will become more stable and more promotion for business life in the coming 12 months. The next FOMC meeting is in September, but chairman Jerome Powell said on Wednesday that the committee did not decide whether it will lower the rates. Nevertheless, 38 percent of the RECCs Bog survey respondents see a more favorable tariff movement, an increase of 30 percent in the previous quarter. The negative sentiment fell slightly from 30 percent in 1q to 27 percent.

Asked where they expect the target range to be on December 31, 78 percent of the respondents said they would expect at least one reduction of 25 basic points by the end of the year. The majority, 53 percent, expect the target range to be 4.00 to 4.25 percent.

In general, the Governors will see a much more favorable federal policy landscape in the coming 12 months, with 49 percent that expects a positive effect from government actions, an increase of 11 percent in 1q. The survey showed that only 16 percent related a negative impact, compared to 59 percent in the previous quarter.

#Sentiment #Index #Market #Optimism #Striking #CREFC