Reece – A tough prospect that are expected for tax 2026

The stock price of Reece Limited (ASX: REH) has registered a difficult year, a decrease of approximately 60 percent from a $ 29.20 to sub a $ 12.00. The company reported its results for the 12 months to 30 June, and it seems busy the income for interest and tax (EBIT) margin of 7.4 percent in tax 2024 to 6.1 percent in the six months to June 2025 could continue.

Fiscal EBIT 2025 of a $ 548 million fell by 20 percent on a marginal decrease in sales to $ 9.0 billion. The disappointing results of the American activities (267 branches, a higher net 24) with EBIT, however, fall from $ 137 million to $ 112 million to $ 97 million in the past three half years is a concern. Accordingly, the American EBIT margins have fallen from 5.1 percent to 4.6 percent to 3.6 percent, in the same period.

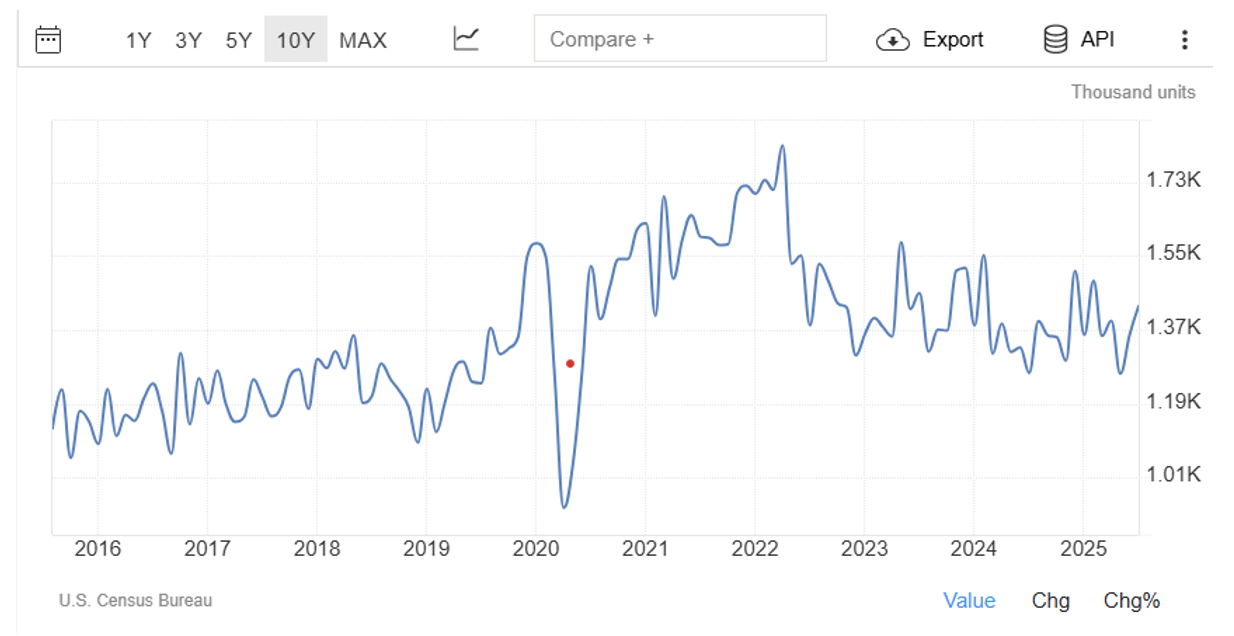

In a commentary on the prospects, management in its own country became the uncertainty (676 branches, a net 15) with a period of soft activity to play, and this was combined with the chance that the American housing market will be limited for the next 12-18 months with affordability that will continue to weigh on housing activity. As is illustrated below, the start of the American homes have fallen from 1.82 million in 2020 to an average of approximately 1.37 million (-25 percent) more recently.

Graph 1: American housing market

Source: US Census Bureau

For the year until June 2025, the net debt rose from $ 518 million to $ 590 million and this was largely due to a net A $ 87 million in business acquisitions. Capital expenditures were a $ 258 million, because the management in the company reinvests with a focus on operational efficiency. The gross interest for tax 2026 is expected to vary between $ 50 million and $ 60 million. The profit per share of REH (EPS) fell by 24 percent to $ 0.49, while the dividend per share fell by 29 percent from $ 0.2575 to $ 0.1836.

Read my earlier article here: leaking trust – Reece’s Outlook looks out.

Chief Executive Officer of Montgomery Investment Management, David Buckland has more than 30 years of experience in the industry.

David is a very well -informed and very experienced executive for financial services. Before he came to Montgomery in 2012, David was CEO and executive director of Hunter Hall for 11 years, as well as director at JP Morgan in Sydney and London for eight years.

This message was contributed by a representative of Montgomery Investment Management PTY Limited (AFL No. 354564). The main purpose of this message is to provide factual information and not to provide financial product advice. Moreover, the information provided is not intended to give a recommendation or opinion about a financial product. However, each comments and opinion of opinion can only contain general advice that has been drawn up without taking into account your personal objectives, financial circumstances or needs. Therefore, before acting on the basis of one of the information provided, you must consider the suitability in the light of your personal objectives, financial circumstances and needs and you must consider requesting independent advice from a financial adviser if necessary before you make decisions. This message excludes specific personal advice.

#Reece #tough #prospect #expected #tax