Prospects of 10-year G-Sec yields falling further to 6.30-6.35 percent exist if both rate deals and repo rate cuts materialize | Photo credit:

Market experts expect the 10-year G-Sec yield (6.33 percent GS 2035) to thaw towards the 6.40 percent level ahead of the December monetary policy committee meeting.

They believe that there are prospects that 10-year G-Sec yields will fall further to 6.30-6.35 percent if both rate deals and repo rate cuts materialize.

CPI inflation

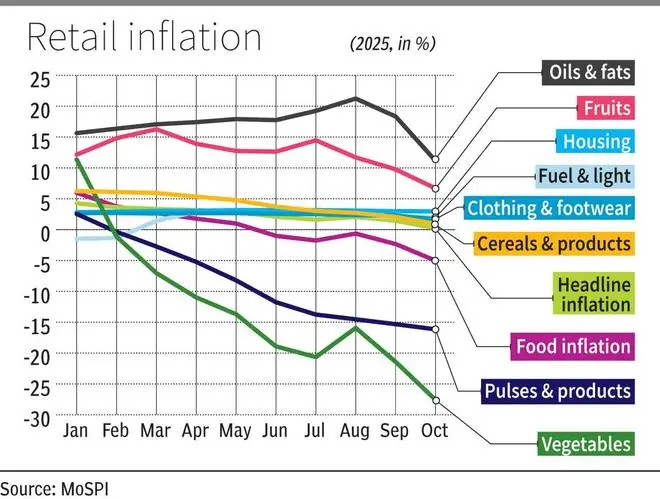

Referring to the CPI inflation for October which stood at 0.25 per cent, marginally below market expectations of 0.40 per cent, V Rama Chandra Reddy, Head – Treasury, Karur Vysya Bank, noted that with inflation hovering around zero, pressure is clearly increasing on the RBI to ease monetary conditions in the upcoming MPC meet.

A reduction in the repo rate of 25 basis points (from 5.50 percent to 5.25 percent) seems increasingly likely; If not, a shift in the policy stance towards ‘accommodative’ or even both cannot be ruled out, he added.

“Consistent buying activity in the ‘others’ category, which is likely to represent RBI’s secondary market operations on NDS-OM, is supporting the bond market. As we move closer to the policy decision, yields are expected to soften further, with the new 10-year benchmark likely to stabilize around 6.38-6.40 per cent before policy outcomes indicate the next direction,” Reddy said.

Venkatakrishnan Srinivasan, founder and managing partner of Rockfort Fincap LLP, noted that despite the record low, the 10-year G-Sec yield fell only slowly to 6.50 percent from the previous close of 6.51 percent.

“The modest reaction reflects the market’s cautious interpretation: Traders and economists want to be sure that this disinflationary trend is sustainable and sustainable before aggressively repositioning on the maturity front. The consensus expectation of a 25 basis point cut in the repo rate in December now looks stronger than ever. However, with the rupee still hovering near ₹88.6 per dollar and concerns over global rates lingering, investors prefer to wait confirmation that the low inflation phase is not just a one-off event driven by base effects and temporary supply corrections,” he said.

Further, from a bond market perspective, yields are likely to remain anchored in the 6.45-6.55 percent range for now, with room to drift towards 6.35-6.45 percent once policy easing is confirmed or external pressures subside.

Ajay Manglunia, executive director of Capri Global Capital, said multi-year low retail inflation is fueling hopes for rate easing.

“But the fact is that US Treasury yields are not coming down. They are still consistently above 4 percent. And the rate cut in the US has been slow. The RBI has been cutting rates in a somewhat aggressive manner… So if there is any rate easing, there could be a 25 basis point rate cut in the next quarter,” he said.

Bond market experts also took heart from RBI Governor Sanjay Malhotra’s observations on bond yields last month.

Malhotra said, “The 10-year G-sec will not move from one to one (in response to the repo rate cut). Let’s also keep that in mind… while there is room for more (movement in rates), and we believe it should go down.

“A number of measures have been considered in this regard, including how the primary G-Sec auctions will be conducted; the tenor of this government offer, not just the central government but also the state government. We are confident that the transmission of monetary policy has already taken place to a large extent and will continue to do so in the future,” Malhotra said.

Published on November 12, 2025

#Record #inflation #fuels #possibility #repo #rate #salutary #effect #GSec #yields