The notorious irrational exuberance speech by Alan Greenspan is a classic example of how crazy markets can always get crazier.

This was the actual text From his speech during a policy dinner in December 1996:

It is clear that persistent low inflation implies less uncertainty about the future, and lower risk premiums implies higher prices of shares and other merits. We can see that in the reverse relationship shown by price/profit ratios and the inflation percentage in the past. But how do we know when irrational exuberance unnecessarily escalated assets values, which are then subjected to unexpected and long -term contractions as they have in Japan in the past decade? And how do we take that assessment into account in monetary policy? We, as central bankers, do not have to worry if a collapsing financial assets are not in danger of reducing the real economy, its production, jobs and price stability. Indeed, the competitive stock market market breach of 1987 had few negative consequences for the economy. But we should not underestimate or become complacent about the complexity of the interactions of asset markets and the economy. Evaluating shifts in balance in general, and in particular with asset prices, must therefore be an integral part of the development of monetary policy.

The former FED chair did not smash on the table that the stock market was a bubble, but he certainly implied that something was wrong.

From 1980 to the speech of Greenspan to the Taart at the end of 1996, the S&P 500 rose in total by more than 1,200% or a blistering return of 16.5% on an annual basis. The ratings were up, in time to time. The IPO from Netscape took place a year earlier. Things felt very toppy.

That didn’t matter. The market left like a rocket ship after the speech of Greenspan:

From the time of Greenspan’s speech during the rest of the decade, the S&P would more than double, good enough for an annual return of almost 26% to the end of 1999. The market rose by 33% in 1997, 28% in 1998 and another 21% in 1999.1

The DOT-Com bubble eventually burst in the spring of 2000 and cut the S&P 500 together with a drawing of more than 80% in the Nasdaq.

Some people start to wonder if we are in a similar situation.

No two markets are ever the same. The companies in the Dot-Com bubble did not earn money. They did not have the ridiculous profit margins that technical shares have today. But there are some similarities.

The AI Capex output bing is creepy similar to the Telecomm Buildout that took place in the 1990s.

Speculative activity is also everywhere – spacs, meme -shares, Iposleverage, story stocks, high valuations, deregulation, etc.

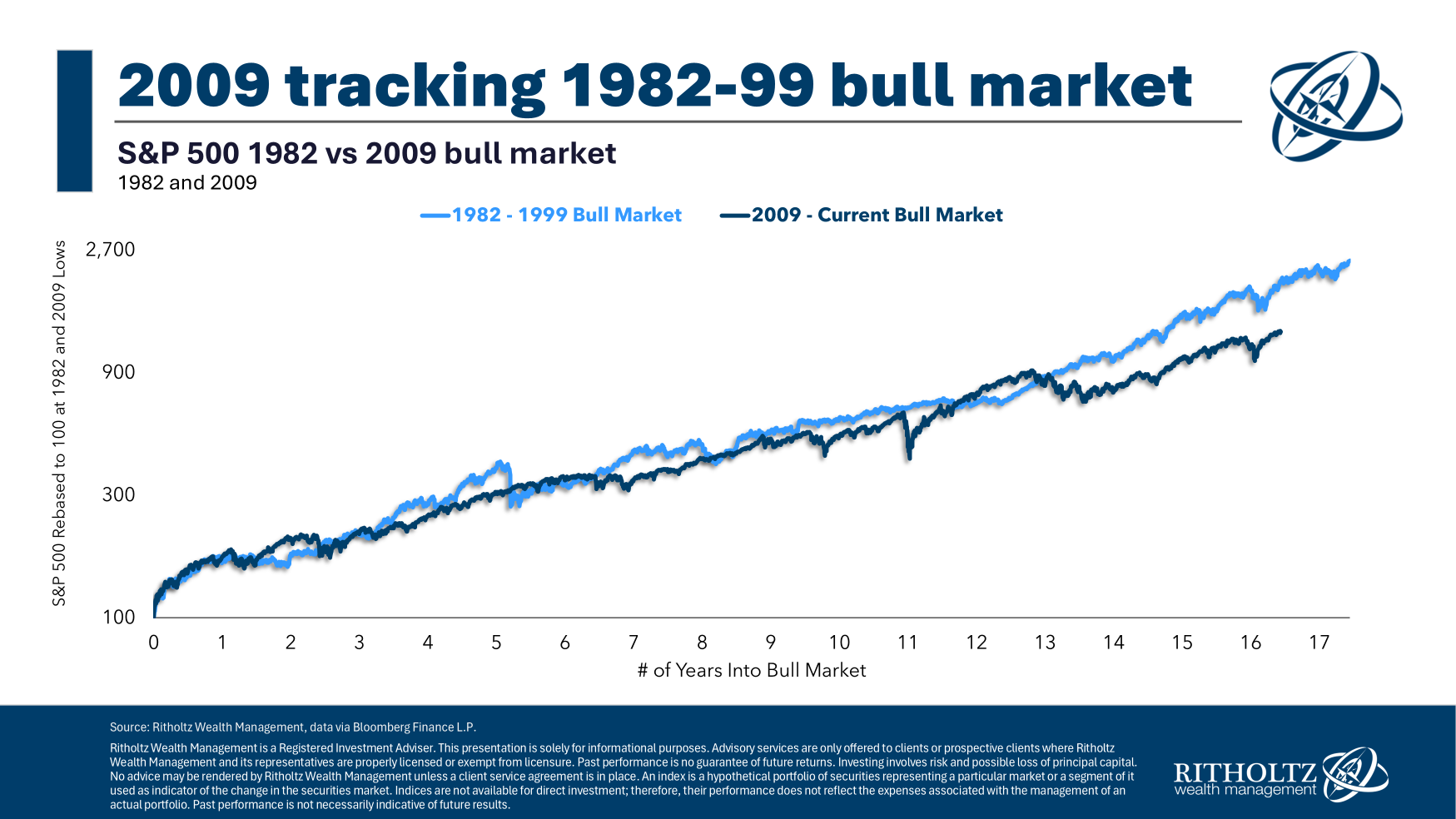

And the two bull markets have adopted a similar process over time:

Many people try to find out if this is the early stages of a bubble or the end of the road.

Investing would be a lot easier if there was a simple way to predict these types of markets. Unfortunately that is not. Nobody can predict when human nature will take things too far or when it stops on a dime. The pendulum always waves; We just don’t know how far in both directions.

Predicting the market in the short term is impossible.

Investing for the long term is the best remedy for the uncertainties of the short run.

If you had invested in the speech of Greenspan in the S&P 500 in December 1996 and held it up until today, you would just be shy of 10% per year. In the next decades, 9/11, several wars, oil, oil, to $ 150/vessel then negative, the pandemic, 40-year-old high inflation, the bear market of 2022, the bear market and about a dozen different duration and so to $ 150/barrel and about a dozen other duration corrections.

But even after all those bad things you would still have more or less achieved the annual return of the market.

That’s not bad.

If you had invested at the height of the market just before the DOT-Com Bubble burst at the end of 1999, you would be a little more than 8% per year. That is not a terrible result, given that all the bad things that you should have endured plus that was the most expensive ratings the US stock market has ever seen.

It is clear that nobody invests that way (except Bob). People don’t put all their money to work in one go.

Most people invest in 1996, 1999, 2007, 2009, 2020 and everything in between. One of the best characteristics of dollar costs in the market is in the course of the time you can diversify in time, level of valuation and market environment.

If you are on average on the market over time, you must welcome the volatility.

If you are fully invested, you must be willing to accept volatility or diversify your assets to dampen the pain it can cause.

These things are much simpler and more useful than trying to predict the start or end of a financial assetubbel.

Continue reading:

An epic bull market

1And that followed +37% in 1995 and +23% in 1996. Only an insane run.

#wealth #common #sense