Through BLACK ENTERPRISE editors

October 18, 2025

Self-employed individuals, such as small business owners and independent contractors, are always looking for ways to reduce their tax bill and better manage healthcare costs. An option that is often overlooked among many new entrepreneurs is a health savings account (HSA).

An HSA is a tax-advantaged account that helps pay for qualified medical expenses, such as certain ones vision care And dental serviceswith tax-free dollars. Unlike a flexible spending account (FSA), which is sponsored and managed by an employer, you can set up and manage your own HSA even if you are self-employed. GoodRxa drug savings platform, shares important considerations to keep in mind before opening an HSA on your own.

Key Takeaways:

- As a self-employed freelancer or business owner, you can open a health savings account (HSA) if you have a qualified high-deductible health plan.

- An HSA can help self-employed people save money on out-of-pocket health care costs, such as reading glasses and over-the-counter medications.

- Make sure you understand the HSA rules before opening an account.

Can a self-employed person have an HSA?

Yes. A self-employed person may qualify for an HSA if they have a qualification high deductible health plan (HDHP). This includes Instacart shoppers, freelance consultants, Uber drivers, and small business owners. You do not need to have an employer or a full-time job to qualify for an HSA.

What are the requirements to open an HSA?

There are a few rules that self-employed people should be aware of before opening an HSA. First, you must have one qualified HDHP. Your health insurance must meet annual out-of-pocket limits and minimum deductibles. These plans are usually included higher deductibles and lower monthly premiums than other types of coverage.

If your HDHP qualifies, you’ll need to make sure you meet other requirements. Here are a few HSA qualifications outlined by the Internal Revenue Service:

- You have no health coverage other than certain ones coverage ignoredsuch as dental and eye insurance.

- Individuals who have signed up Medicare are not allowed contribute to an HSA.

- Persons who are dependent on the return of someone else are not allowed to collect the deduction.

- You have HDHP coverage on the first day of the last month of the year to meet the line of the last month. For many self-employed people this is December 1, whose insurance year often starts on January 1.

Beginning January 1, 2026, the eligibility rules for health savings accounts (HSAs) will be expanded. Under the One Big Beautiful Bill Act (OBBBA), bronze and catastrophic Affordable Care Act (ACA) marketplace plans will be reclassified as qualifying HDHPs. This change will make it easier for more self-employed people to take advantage of the tax benefits of an HSA without having to switch to a traditional HDHP.

How do you open an HSA?

If you meet the qualifications to open an HSA, you will need to find a custodian or trustee. This could be a bank, credit union, insurance company, or an IRS-approved broker. A few things to consider when opening an account are:

- What are the administration costs?

- Is there a minimum dollar amount to open the account?

- Are there investment opportunities?

- Is there a minimum cash balance required before I can invest my money?

- How much are the investment costs?

- Will I receive a debit card or do I have to provide receipts for reimbursement?

As a sole proprietorship, you do not have an employer who contributes on your behalf or covers administration costs. Do your research and ask the right questions to ensure the HSA meets your needs. That’s possible compare HSA providers online to help you make the best decision.

Sole proprietors versus traditional employees

The HSA qualifications for a traditional employee and a sole proprietor are the same. But there may be a difference in making contributions to the account.

Traditionally, an employee tells their employer how much they want to contribute to their HSA. An employer can also contribute money to improve the working conditions for employees. The amount contributed by employer and employee may not exceed the annual limits. Payroll will deduct money from your paycheck to fund the HSA. This is called an input tax contribution. Employees can contribute money to their HSA before their income is taxed. This can reduce your taxable income and save you money during tax season.

Being an entrepreneur can offer more freedom, but it also comes with more responsibility. A sole proprietor must set up their own HSA contributions. You can transfer money from your checking account to your HSA whenever you want. Many self-employed people make after-tax contributions to fund their HSA. This offers the opportunity to claim a deduction when you file your tax return.

How much can I contribute to my HSA?

Your HSA contribution limits depend on whether your health plan has individual or family coverage. Other variables that influence how much you can contribute Are:

- Your age. If you are 55 years or older, you can deposit an additional €1,000 into your account.

- The date you become an eligible individual. If you are eligible to make HSA contributions before December 1, you may be eligible to contribute the maximum amount based on the last-month rule.

- The date on which you are no longer eligible. You cannot make deductible contributions for months in which you did not meet HSA requirements.

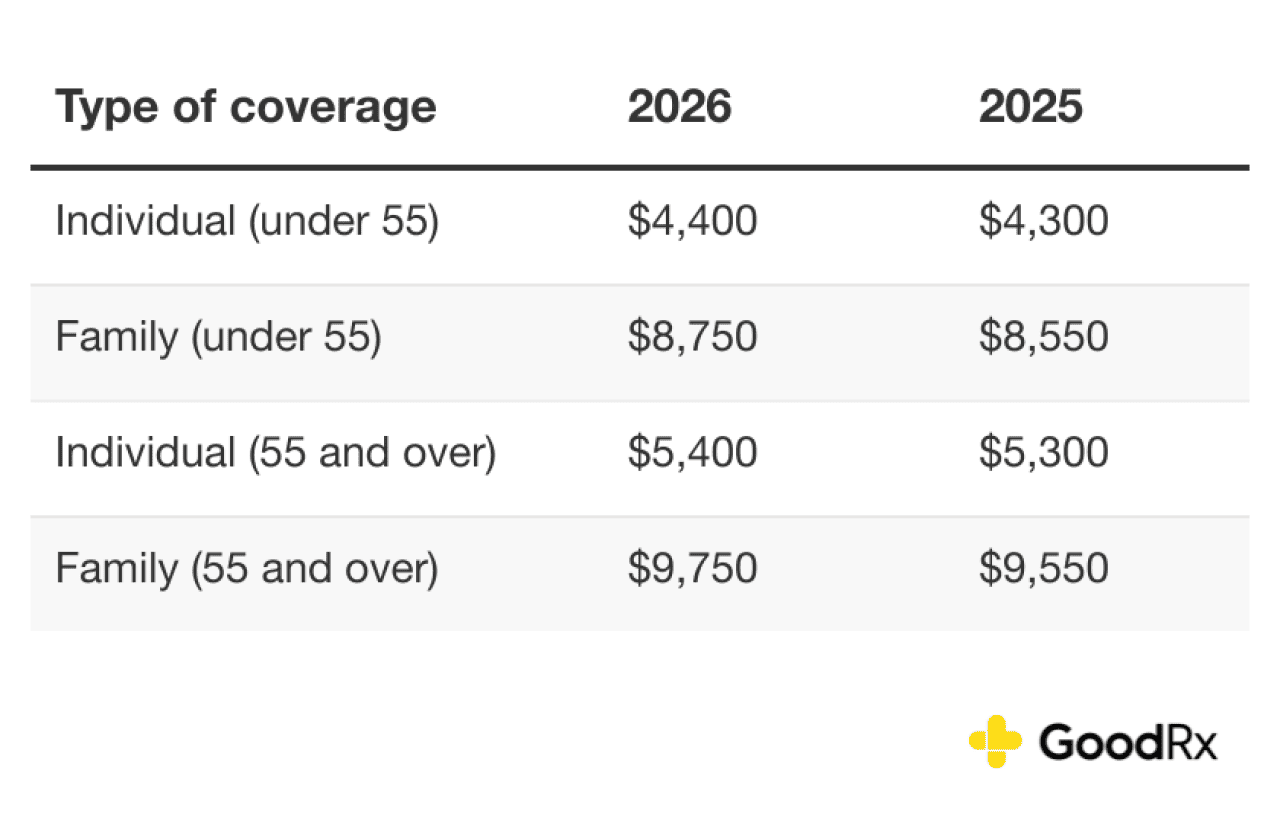

The premium limits for 2025 are $4,300 for individual HSA plans and $8,550 for a family plan. If you are 55 years or older at the end of the tax year, you are eligible for a catch-up contribution of € 1,000. You have until the following year’s tax deadline to make your contribution. That means you can contribute to a 2025 HSA until April 15, 2026, unless the tax filing deadline changes.

Here are the maximum HSA contribution limits for 2025 and 2026:

What are the advantages of a health savings account if you are self-employed?

An HSA is a financial instrument that you own that saves and provides you with money tax incentives. Here are some additional benefits that may come in handy for the self-employed:

- The contributions remain in your account until you use them.

- You do not have to contribute a minimum amount.

- You can invest the money.

- You can use funds for qualified medical expenses.

Unlike a flexible spending accountrequiring you to use or lose the money you’ve saved, your HSA dollars roll over each year until you use them. You will not be penalized if you do not contribute to your account. There is no minimum contribution per year, but there is one a maximum on the amount you can contribute. You can make the most of your HSA contributions by investing your money. As your money grows, you will have more money available to finance future medical expenses.

An HSA pairs well with HDHP coverage because it covers qualified expenses you incur before meeting your deductible. This includes but is not limited to:

For a complete list of qualified expenses, visit IRS Publication 502. The CARES Act added over-the-counter medications And menstrual products to the list.

What are the disadvantages of an HSA?

HSA benefits only go so far if you don’t know how to take full advantage of them. Here are some potential drawbacks to consider, including:

- Insurance plan requirements: Only individuals enrolled in a qualified HDHP can contribute to an HSA. With this type of plan, you must pay your healthcare costs out of pocket until you meet your deductible, which can be thousands of dollars.

- Annual contribution limits: There is a limit on the amount you can contribute annually to an HSA. If you contribute outside the limits, you could face a 6% penalty for over-contributions.

- Spending restrictions: Your HSA is used to pay for qualified medical expenses. If you spend your HSA dollars on non-qualified expenses, you will owe income taxes on the distribution. You will also receive a fine if you are younger than 65.

- Investment risks: If you invest the money in your HSA, your investment may lose value if market conditions are not favorable.

- Account fees: Depending on your HSA provider, you may have to pay fees for services such as account maintenance, investments, transactions, and paper statements.

- Ineligibility for Medicare: You cannot contribute to an HSA after you retire enroll in Medicare. But you can still use the money in your account to pay for qualified medical expenses.

The bottom line

Self-employed people can contribute money to an HSA and use the money to pay for qualified medical expenses. If you want to open an account, make sure you have a qualifying health plan and understand the HSA rules. Also inquire about account requirements so that you are not confronted with unexpected costs. An HSA can be very useful for self-employed individuals, but it is important to do your research to determine if it is the best account for your needs.

This story was produced by GoodRx and reviewed and distributed by Stacker.

RELATED CONTENT: Venus Williams wins on behalf of health insurance

#open #health #savings #account #selfemployed