Through BLACK ENTERPRISE editors

October 24, 2025

One of the many benefits of living in the 21st century is that average life expectancy is higher than ever before. People who reach retirement age can expect to enjoy many more years of health and happiness than their parents and grandparents.

One of the many benefits of living in the 21st century is that average life expectancy and longevity are higher than ever before, and people who reach retirement age can expect to enjoy many more years of health and happiness than their parents and grandparents.

This creates concerns at the state and national level as the aging population puts pressure on several systems that were designed and implemented long before current longevity trends occurred. It also poses potential problems for individuals, as the issue of financial security in retirement becomes more pressing when people can reasonably expect to live longer while relying on the retirement provisions they have made.

So is there a real crisis, or can we expect rising life expectancy to be manageable with the right planning? The team of Abacus Global Management, Inc. wanted to answer this question by letting the data speak for itself.

The growth of Golden Years Living

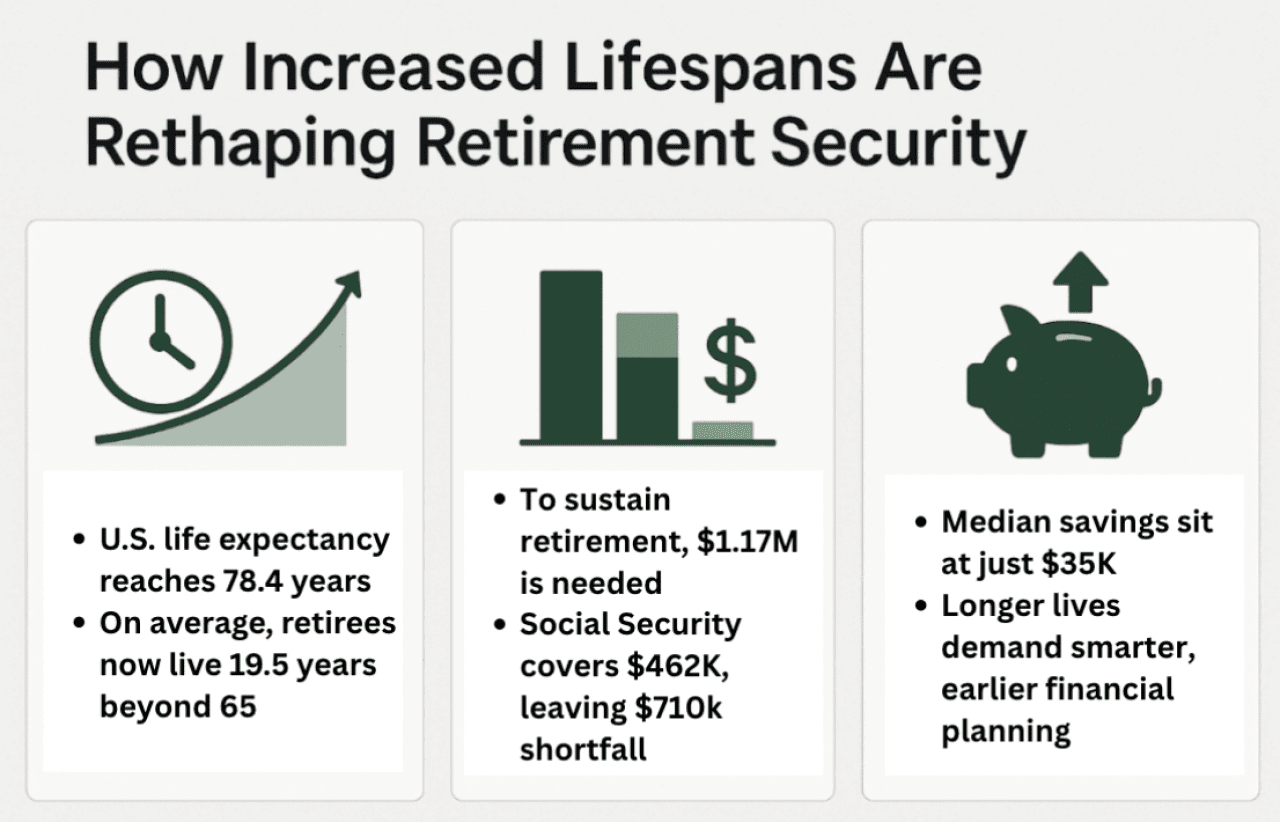

The newest statistics from the CDCpublished before 2023, indicate an average life expectancy of 78.4 years. This represents an increase of almost a year compared to 2022 data, showing how quickly lifespan is increasing year on year.

What is more relevant to our discussion is the life expectancy for someone who reaches 65. This is an average of 19.5 years, meaning that someone who chooses to end their career at this point has almost twenty years ahead of them.

There is a gender gap here: women who reach 65 will live another 20.7 years, while men can expect to live another 18.2 years if they survive to this point.

The retirement savings conundrum

Interpreting the data on retirement security is relatively difficult because there is a significant gap between those who have socked away significant sums and those with more modest pots. This makes averages less useful without further research.

Vanguards latest report on savings habits is an example of this. The reported average account balance for 2023 was $35,286. This represents the exact center point of each account in this specific provider’s customer base.

However, the average holdings for the year were $134,128, with this figure rising well above the median due to a smaller number of people putting away significantly more money than normal. In fact, only 15% of customers had saved more than $250,000, while 53% had less than $40,000.

Figures from Fidelity provide a little more clarity. Here, data on 401(k) and IRA balances breaks down across generations. Baby Boomers lead the pack with $249,300, while Generation X is close behind with $192,300. Millennials have an average of $67,300, while Gen Z brings in $13,500, which is understandable considering that many members of this group are just entering the workforce or still pursuing full-time education.

It’s also worth checking out the data from the Consumer finance researchthat paints its own picture of the current state of affairs in the field of pension savings. The most recent survey, conducted in 2022, shows that family retirement accounts average $87,000. That’s up from $75,350 in 2019.

The growing gap

People are therefore living longer and getting older, and average pension pots are increasing, albeit modestly. What really matters is the affordability of the pension. Inflation remains a problem, and people on a fixed income in retirement need to take this into account if they want to maintain their quality of life.

Facts from the Federal Reserve Bank of St. Louis shows that the average annual expenditure for those over 65 is $60,087. The math is simple: you need $5,000 a month to keep up with the cost of modern living, or $1,171,696 over 19.5 years.

Social Security retirement benefits may account for some of this, although it is well below the $5,000 limit. Receivers for example were paid $1,976 before January 2025, meaning they’ll need more than $3,000 from their personal retirement assets to close the gap.

The pension deficit

While $1.17 million is a daunting amount, retirees don’t have to fund it all from their personal savings. Social security provides a crucial income stream. With an average monthly benefit of $1,976 ($23,712 per year), the average retiree can expect to receive about $462,000 from Social Security over the 19.5 years of retirement.

This leaves a gap of roughly $710,000 that will need to be covered by personal savings, pensions and investments.

When this required savings figure is compared with reality, the true scale of the problem emerges. According to Vanguard’s 2023 “How America Saves” report, the average retirement account balance was just $35,286. Even the average balance, skewed by high-net-worth individuals, was only $134,128. This shows a staggering shortfall of nearly $700,000 for the typical American retiree.

The bottom line

There are variations in lifespan based on age, gender, socioeconomic status, race, and many other factors. These same variables influence average incomes, savings and other assets. It is therefore not possible to draw conclusions about your own circumstances based on data at the highest level.

What is clear is that if you continue to work now, you will live longer than if you had been born in an earlier generation. Therefore, preparing for life after work sooner or later requires more thought and a stronger commitment.

The pension gap is real and the cost of living will only increase as time goes by. Saving early and investing wisely will stand you in good stead for a future where the only certainty is that you need a solid financial foundation to enjoy your retirement, rather than living solely on government benefits.

This story was produced by Abacus Global Management and reviewed and distributed by Stacker.

RELATED CONTENT: Ndamukong Suh is retiring from the NFL and tackling wealth building with a new financial podcast

#Longevity #Changing #Retirement #Security