2026 is already proving to be a busy news year for the housing market, starting with our first figure:

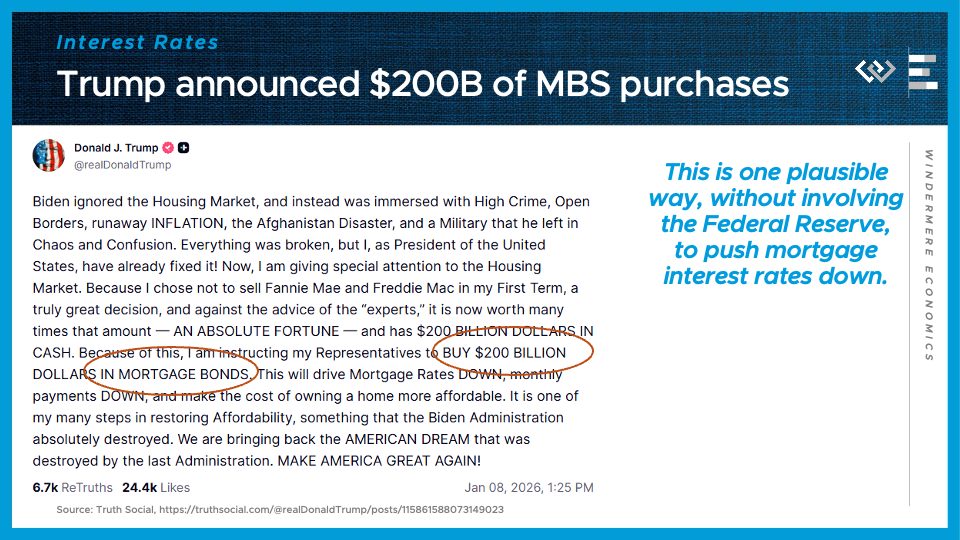

$200 billion

That’s the total value of mortgage-backed securities that President Trump announced on January 8e he has instructed “his representatives” to buy, with the aim of lowering mortgage rates. A large new buyer of mortgages will tend to raise prices, which – for bonds – means interest rates will go down.

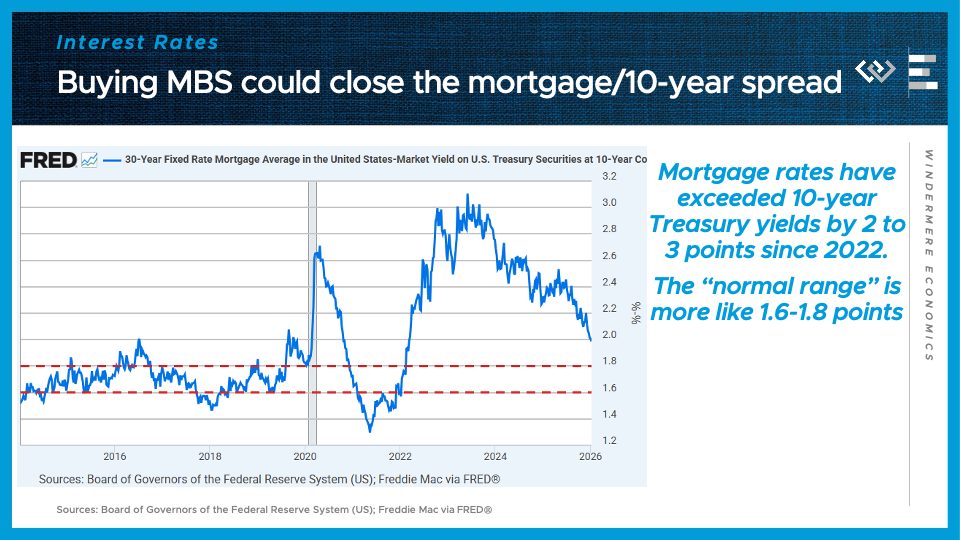

Over the past three years, mortgage rates have been unusually high relative to the 10-year Treasury rate, which has gradually returned to a normal range, and this buying spree, apparently by Fannie Mae and Freddie Mac, should accelerate that process of narrowing the spread.

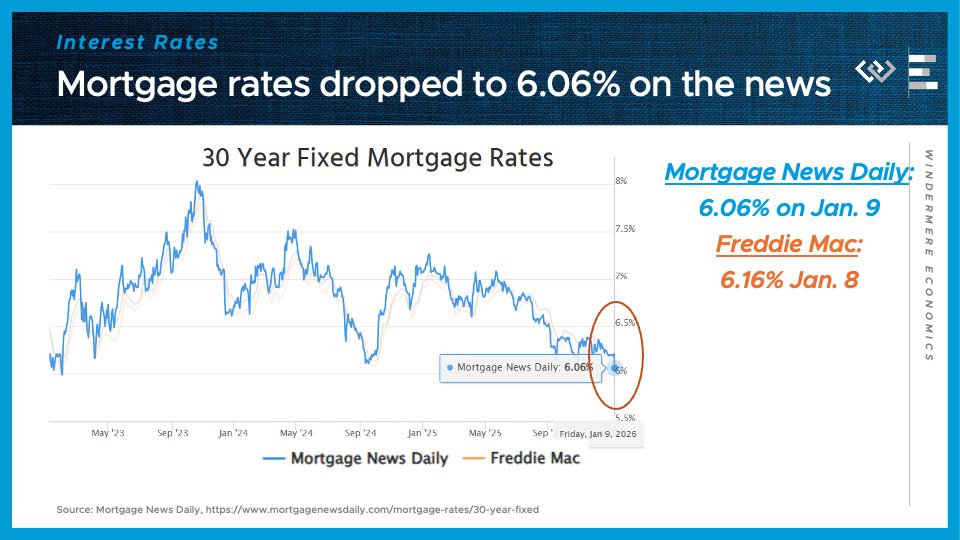

The markets took this announcement very seriously. On the first day of trading after Trump’s announcement, mortgage rates fell 15 basis points, which brings us to our second number we need to know now:

6.06%

That was the average 30-year mortgage rate from Mortgage News Daily on Friday, January 9eand that’s the lowest mortgage rate they’ve reported in almost three years. Now, trading has been extremely volatile, and there are still many unanswered questions about this new program, but there is no doubt that in the short term it has moved the markets, and I think SOME highly qualified buyers and sellers who start to see mortgage rates in the 5% range will be more motivated to transact this spring.

Another song you need to know now:

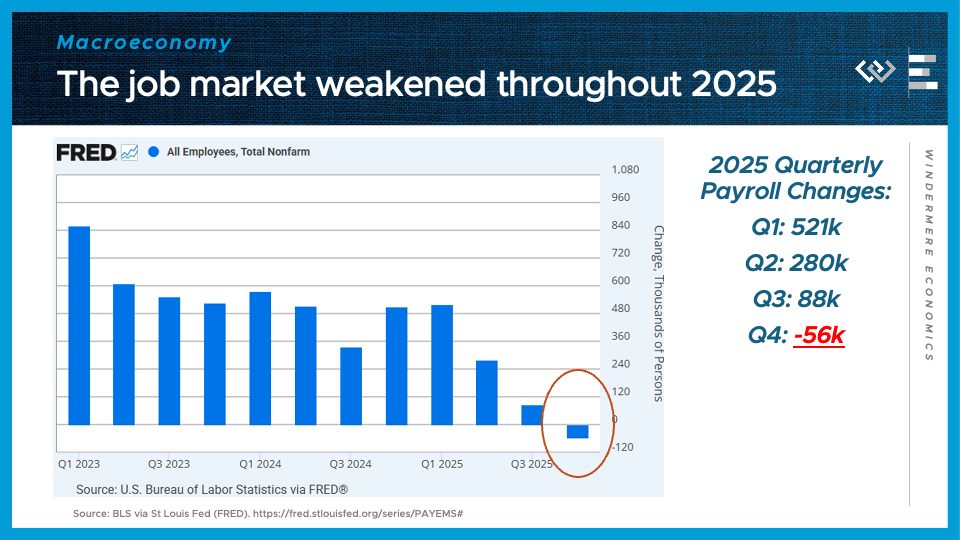

56,000

That’s the number of jobs lost net for the fourth quarter of 2025, capping off a year of slowing and ultimately contracting labor costs in the U.S. economy. Other data show that economic activity remained at a good level in the fourth quarter. So this is not the start of a recession, but slowing job growth could help explain why home purchases were disappointing in the fourth quarter, despite lower mortgage rates than at the end of 2024.

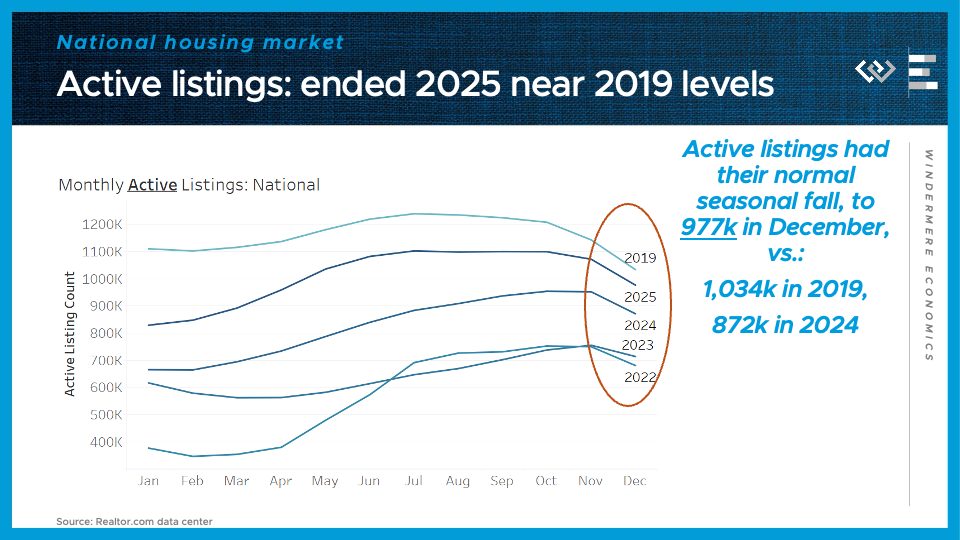

Speaking of homes, 2025 ended with the housing market still just shy of a key benchmark I’ve been watching: the point at which active inventory recovers to pre-pandemic levels, 2019. The year ended with just under a million active listings, up from just over a million six years ago, on the eve of the Covid pandemic.

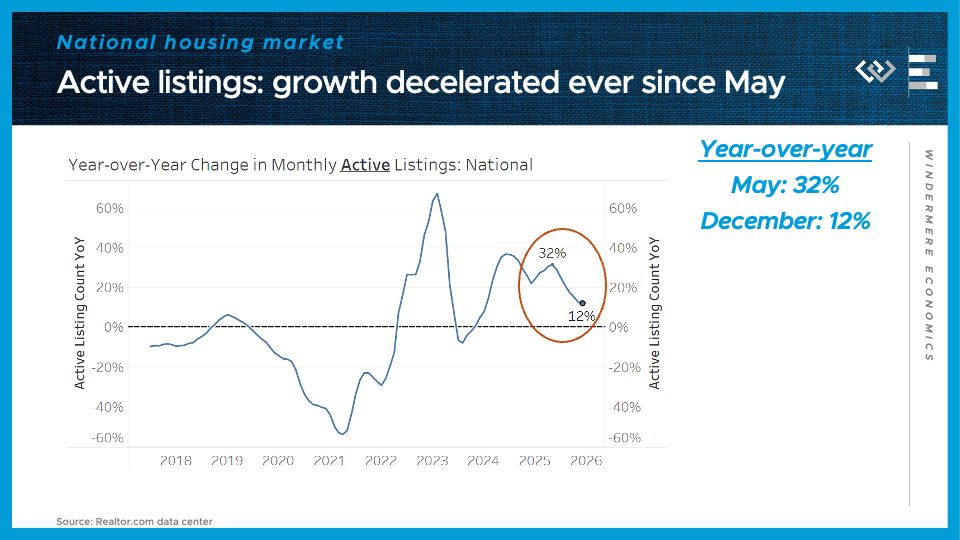

That’s still substantial compared to this time last year, but the trend of year-on-year listing growth has clearly slowed through 2025. That partly explains why 2025 went down as the year of cooling down and normalization, but NOT something like a fire sale or an abundance of unsold houses. Rather, it is a market that has made a lot of progress towards normality, which portends a healthy, balanced market for the year ahead.

#Figures #mortgage #rates #moving