Read quickly

- FHA will increase lending limits by 3.26 percent through 2026, allowing homebuyers to borrow up to $541,287 in low-cost markets and $1.249 million in high-cost markets such as New York and San Francisco.

- In Alaska, Hawaii, Guam and the U.S. Virgin Islands, FHA loan caps will increase to $1.873 million for single-family homes, reflecting higher construction costs in those regions.

- FHA loan limits are typically equal to 115 percent of a market’s median home price, with a national minimum and high cost caps to balance affordability and risk for first-time buyers.

- FHA delinquencies are rising, with nearly 12 percent of borrowers behind on payments in October, more than five times higher than for Fannie Mae- and Freddie Mac-backed loans, according to data from ICE Mortgage Technology.

An AI tool created this summary, based on the text of the article and checked by an editor.

FHA loans are popular among first-time homebuyers and have higher delinquencies, and borrowers are more likely to become underwater or declare bankruptcy when home prices fall.

Homebuyers who put down just 3.5 percent will be able to borrow at least $541,287 in low-cost markets next year, and as much as $1.249 million in high-end markets like New York, San Francisco and Washington, D.C., after a 3.26 percent increase. 2026 FHA Loan Limits announced on Thursday will come into effect on January 1.

The cap for single-family homes in Alaska and Hawaii will increase to more than $1.87 million in recognition of higher construction costs in those states.

The higher loan limits for mortgages backed by the Federal Housing Administration (FHA) follow similar increases for conforming loans eligible for purchase by Fannie Mae and Freddie Mac.

Fannie and Freddie’s 2026 conforming loan limit for single-family homes will be $832,750 in most markets and up to $1,249,125 in high-end markets, the Federal Housing Finance Agency (FHFA) announced Nov. 25.

FHA loan limits vary by county or Metropolitan Statistical Area (MSA) and are typically equal to 115 percent of the median home price for that market.

A minimum national loan limit allows buyers in low-cost markets to qualify for loans higher than 115 percent of the median home price, while caps in high-cost markets prevent the FHA from having to insure homes that are considered out of reach for most first-time homebuyers.

2026 FHA Loan Floors and Ceilings

Source: Department of Housing and Urban Development.

FHA’s 2026 minimum national loan limit for single-unit properties is $541,287, which is 65 percent of Fannie and Freddie’s conforming loan limit. That’s $17,062 more than the $524,225 in 2025.

The maximum loan limit ceiling in most highest-cost areas is 150 percent of the conforming limit, or $1,249,125 for single-unit properties, an increase of $39,375 from 2024.

To account for higher construction costs in Alaska, Hawaii, Guam and the U.S. Virgin Islands, the new FHA cap in those markets is $1,873,625, an increase of $59,000 from $1,814,625 in 2024. The 2025 cap for four-unit properties in those markets is $3,603,925.

Thanks to their low down payment and credit score requirements, the vast majority of FHA-backed purchase mortgages (more than 80 percent) are made by first-time homebuyers.

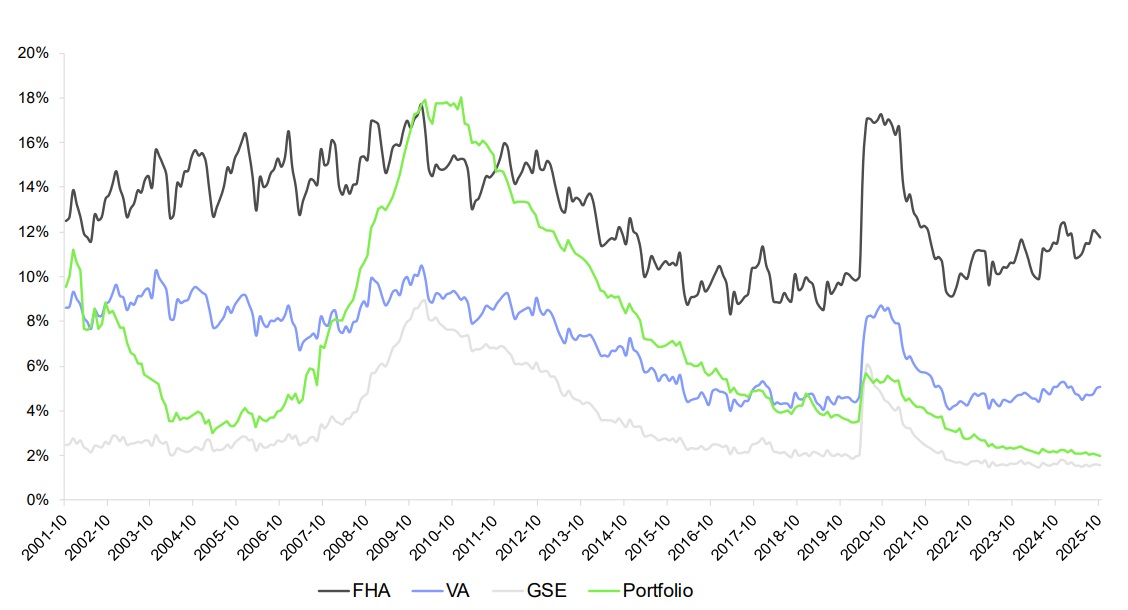

FHA delinquencies are increasing

Mortgage arrears by loan type. Source: ICE Mortgage MonitorDecember 2025.

But delinquencies on FHA loans are increasing and are currently more than five times that of loans backed by Fannie Mae and Freddie Mac (the government-sponsored entities, or “GSEs”).

Nearly 12 percent of FHA borrowers were delinquent in October, compared with the average of 3.34 percent for all mortgage holders and less than 2 percent for loans backed by Fannie and Freddie, according to data tracked by ICE mortgage technology.

Because they start out with less equity in their homes, ICE data shows that FHA buyers are also more likely to end up underwater or declare bankruptcy when home prices fall.

Private mortgage insurers compete with FHA and VA loan programs to serve homebuyers who cannot afford to make a large down payment. Fannie Mae and Freddie Mac require private mortgage insurance when homebuyers put down less than 20 percent.

FHA premium reductions in 2015 and 2023 have made FHA loans more attractive than conforming mortgages with private mortgage insurance, for many borrowers with a loss of less than 5 percent, according to a analysis from the Urban Institute.

But borrowers with a FICO score of 700 or higher can often get a better deal by getting a conforming loan backed by Fannie or Freddie with private mortgage insurance, the analysis found.

Receive Inman’s mortgage newsletter straight to your inbox. A weekly roundup of all the world’s biggest mortgage and closing news, delivered every Wednesday. Click here to subscribe.

Email Matt Carter

#FHA #wanted #support #loans #million #highcost #markets