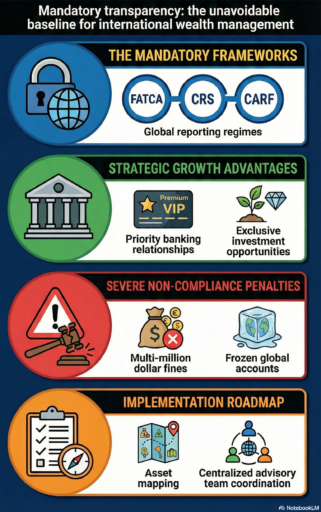

Cross-border asset management has entered a new era where optional compliance no longer exists. CRS, FATCA and CARF make transparency mandatory for wealthy individuals.

In addition to avoiding fines, proactive compliance strengthens credibility, opens doors to international banking and investing, and positions investors to navigate complex legal areas with confidence.

Ignoring these requirements exposes investors to serious financial, legal and reputational consequences.

Key Takeaways:

- Compliance with CRS, FATCA and CARF is mandatory and enforceable worldwide.

- Strategic compliance can unlock access to banks, investments and credibility.

- Non-reporting jurisdictions are additional and not exempt.

- Coordinated advisory teams and monitoring reduce risks.

My contact details are hello@adamfayed.com and WhatsApp +44-7393-450-837 if you have any questions.

The information in this article is intended as general guidance only. It does not constitute financial, legal or tax advice, and is not a recommendation or invitation to invest. Some facts may have changed since the time of writing.

Why cross-border compliance is inevitable

Global reporting regimes such as CRS, FATCA and CARF have transformed the international financial world. Investors and financial institutions can no longer view reporting as optional.

- FATCA: US citizens and residents must report foreign accounts; Foreign banks report to the IRS.

- CRS: More than 100 jurisdictions automatically share account information with tax authorities.

- CARF: Expanding reporting to crypto assets worldwide.

High net worth investors should consider these regimes in every aspect of planning, as fines, frozen accounts and audits can result from non-compliance in any participating jurisdiction.

What was once optional is now a basic expectation.

Why ignoring compliance is riskier than ever

Non-compliance now exposes investors to multi-jurisdictional fines, reputational risks and potential criminal liability.

- Financial penalties: Both investors and institutions could face fines ranging from several thousand to millions of dollars.

- Access restrictions: Banks in compliant jurisdictions may refuse to open or maintain accounts for non-compliant customers.

- Reputational exposure: Asset tracking and media reporting make privacy violations more visible.

- Increasing risks between regimes: Failure in one jurisdiction can trigger reporting and enforcement in others, further exacerbating the consequences.

What benefits come from strategic reporting?

Compliance with CRS, FATCA and CARF can be used to strengthen asset strategy and unlock opportunities.

- Improved banking relationships: Banks prefer fully compliant customers for quality services.

- Access to investment opportunities: Structured products and cross-border credits often require transparency.

- Legal flexibility: Compliance creates a basis for safe use of non-CRS or non-CARF jurisdictions.

Transparency is increasingly a currency in international wealth planning. Compliance can improve reputation, market access and even bargaining power with financial institutions.

Who benefits most from strategic compliance?

High net worth, multi-jurisdictional investors with exposure to cryptocurrencies stand to benefit the most from proactive compliance with CRS, FATCA and CARF, unlocking access, credibility and risk management benefits across borders.

- Families with international wealth structures: Compliance protects generational assets.

- Entrepreneurs with complex global revenue streams: Reduces exposure to multiple tax regimes.

- Investors who own crypto or alternative assets: Ensures that digital holding companies comply with reporting obligations.

How compliance can be used strategically

Proactive compliance improves tax efficiency, access and risk mitigation across all jurisdictions.

By planning around CRS, FATCA and CARF, you can turn mandatory reporting into a strategic advantage.

- Proactive reporting reduces enforcement risk.

- Jurisdiction selection matches compliant countries to their planning objectives.

- CARF compliance ensures that digital assets are managed legally.

- Integrated advisory teams maximize strategy effectiveness.

Investors who integrate compliance into their planning don’t just avoid fines. They unlock growth, diversification and credibility that isolated or reactive approaches cannot provide.

Compliance overview

| Regime / Jurisdiction | Domain | Reporting requirement | Type of assets | Strategic implication |

| FATCA | American persons worldwide | Mandatory reporting of foreign accounts to the IRS | Bank accounts, securities | Access US-friendly institutions, avoid fines |

| CRS | 100+ jurisdictions | Automatic exchange of tax information | Bank accounts, investments | Ensures transparency; non-participation limited |

| CARF | Global crypto ownership | Digital asset reporting | Crypto, tokens, stablecoins | Compliance ensures legal use of crypto abroad |

| Non-CRS/non-CARF | Select jurisdictions | No automatic reporting | Bank accounts, alternative investments | Can be used for privacy/diversification, but home country compliance still dominates |

How to structure compatible global prosperity strategies

Compliance must be integrated into every aspect of planning, from account location to asset type and reporting structure.

Proactive structuring ensures that regulations become instruments instead of obstacles.

Practical steps to implement strategic compliance

Monitor assets, centralize advisors, integrate reporting and align compliance with asset strategy.

- Map all assets: Includes traditional and digital holdings.

- Consolidate advisory teams: Tax, legal and investment experts centrally coordinated.

- Use compliance proactively: Provide credibility and gain access to preferred services.

- Monitor evolving regimes: CRS, FATCA and CARF rules change regularly; stay ahead.

By treating compliance as a strategic asset rather than a burden, investors can project credibility, gain access to preferred financial services and unlock opportunities that reactive approaches would miss.

Who Still Benefits from Non-CRS, Non-CARF Jurisdictions?

Investors seeking additional privacy, diversification, or estate planning options may find non-CRS and non-CARF jurisdictions useful.

Non-participating countries may offer some privacy benefits, but strategic compliance is still required.

- Selective planning: Investors can use non-CARF or non-CRS countries for diversification, asset structuring or privacy, but must remain transparent in their home jurisdiction.

- Crypto and digital assets: Non-CARF jurisdictions sometimes provide temporary gaps in reporting, useful for planning, but risky if misunderstood.

- Legal guidance is mandatory: Expertise ensures that temporary benefits do not become obligations.

Even in non-reporting jurisdictions, the legal obligation in the investor’s country of tax residence always dominates, making compliance proactive and not optional.

How consulting practices are changing

Advanced compliance tools and automated reporting transform the way investors and advisors manage international obligations.

Real-time software can flag potential reporting triggers across jurisdictions, allowing teams to take action before small issues escalate into major compliance issues.

Integrated consulting practices are also becoming the norm.

Centrally coordinating tax, legal and investment advice ensures that every decision is aligned with global reporting requirements, reducing gaps and avoiding conflicting guidelines.

Data-driven reporting has further streamlined obligations under FATCA, CRS and CARF.

By automating routine tasks, advisors minimize human error and reduce operational exposure, freeing up time to focus on strategic planning rather than just regulatory maintenance.

As a result, compliance is no longer just a regulatory burden, but is evolving into a strategic advantage.

Investors who leverage these modern practices can improve efficiency, proactively manage risk and maintain credibility across all jurisdictions.

Frequently asked questions

What is the difference between CRS, FATCA and CARF?

CRS, FATCA, and CARF are global tax reporting rules: CRS is for the automatic exchange of financial information between countries, FATCA focuses on offshore accounts of US taxpayers, and CARF requires reporting of cross-border crypto assets.

Can investors still use non-CRS or non-CARF countries?

Yes, but only as part of a fully compliant strategy.

Non-reporting jurisdictions may support diversification, estate planning or privacy, but home country obligations always take precedence. Getting this wrong can pose serious legal and financial risks.

What are the sanctions for non-compliance?

Penalties can include financial fines ranging from thousands to millions of dollars, frozen accounts, reputational damage, and in some cases criminal exposure.

Non-compliance in one jurisdiction may also trigger reporting or enforcement action in other jurisdictions.

Does compliance limit privacy?

Yes, transparency is required, but carefully structured strategies can balance legal reporting with confidentiality.

Investors can maintain their privacy while fully adhering to CRS, FATCA and CARF regulations.

How often should compliance strategies be reviewed?

Compliance strategies should be reviewed at least annually, or whenever new assets, jurisdictions or digital currencies are added.

Laws and reporting requirements are evolving rapidly, and regular reviews ensure continued compliance and strategic advantage.

Tormented by financial indecision?

Adam is an internationally recognized financial author with over 830 million answer views on Quora, a best-selling book on Amazon, and a contributor to Forbes.

#CRS #FATCA #CARF #compliance #optional