Cracks in the foundation – the growing home crisis of Australia

Last week I lived an Australian housing market update at Van Eliza Owen, head of research at Cotality (formerly Core Logic). Below are some important insights that I thought was worth emphasizing.

High real estate values but in -depth mortgage pressure

Australia’s residential real estate is currently appreciated at around $ 11.5 trillion. There are 11.3 million homes, with an average value of just over $ 1.0 million each. Outstanding mortgage debt is a $ 2.4 trillion, a debt / value sector of only 21 percent. However, since the Australian household debt has been increased, there are many individual mortgage holders who are struggling.

Real estate towering about SuperAnnuation and shares

The current value of the Residential Real Estste of Australia (a $ 11.5 trillion) is 2.8x the Australian Superannuation Pool (of a $ 4.1 trillion) and 3.4x the value of Australian listed companies (of a $ 3.4 billion prizes) – that is the obsession of Australia.

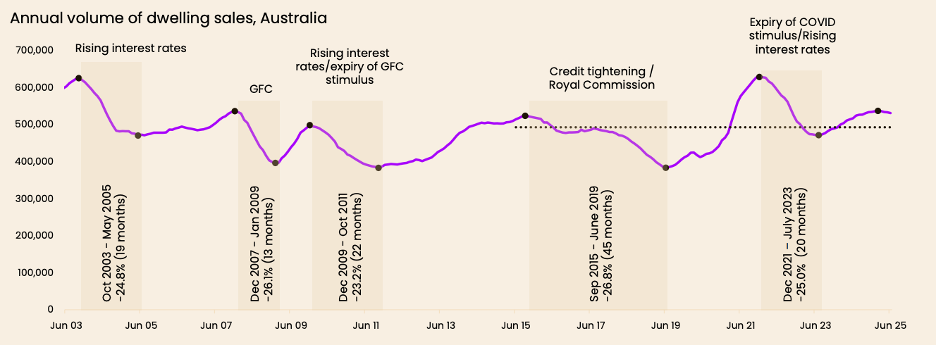

Sales volatility and the impact of interest rates

The total home sales are approximately an annual 530,000, or 4.7 percent of the stock of residential properties. There have been five periods of peak to fall the sales volume of the sales volume of approximately 25 percent in the past 25 years. Apart from the Global Financial Crisis (GFC) 2007-2009 and the Credit Confirming period 2015-2019 at the back of the Hayne Royal Commission, the volume usually coincides with solid rising interest rates.

Graph 1. Annual Volume Housing Sales, Australia

Source: Coality

Vacancies becoming tighter, the rental growth slows down

The vacancy rates in the capital cities of Australia with 1.5 percent are comparable to the average of 10 years of 2.6 percent, and the enormous rental growth of approximately 8-10 percent per year from 2020-2024 is now starting to slow up to 3-4 percent per year. This coincides with net immigration to Australia that a little relaxes.

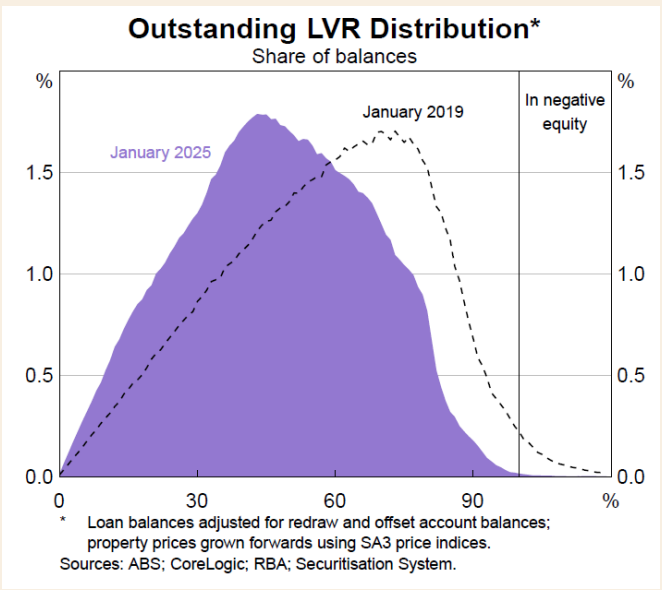

A look at mortgage arrears and negative share positions

The mortgage arrears are low with 1.7 percent of the loans, either non -performance (1.1 percent) or 30+days beyond (0.7 percent). Currently, less than one percent of households are a negative share position, whereby their loans exceed the value of their stay. In 2019 this figure was more than 6 percent, and this shift largely reflects the solid rising values of homes and relatively low unemployment rate.

Graph 2: Only a small percentage of loans is in a negative equity

Source: Cotality, RBA Financial Stability Review

Assess cutbacks to relieve affordability pressure

With the Kastarief of the Reserve Bank of Australia (RBA) is expected to be 1.25 percent to 3.1 percent during the year to February 2026 (0.25 percent in each of February and May 2025, and the forecast of 0.25 percent will be paid in each August 2025, November 2025 and February 2026).

Auction audience rates are rising, but affordability is still a challenge

Auction declaration percentages are collected after the acceleration of May 2025 (0.25 percent to 3.85 percent) and with around 70 percent it now follows above the average of ten years of 64 percent. Unfortunately, the exceptionally high prices compared to income means that housing remains unaffordable for many.

Last thoughts

The housing market of Australia remains a pillar of national wealth, but the base is bursting. Unless deeper structural problems are tackled, the gap between wealth and accessibility will aggravate.

Chief Executive Officer of Montgomery Investment Management, David Buckland has more than 30 years of experience in the industry.

David is a very well -informed and very experienced executive for financial services. Before he came to Montgomery in 2012, David was CEO and executive director of Hunter Hall for 11 years, as well as director at JP Morgan in Sydney and London for eight years.

This message was contributed by a representative of Montgomery Investment Management PTY Limited (AFL No. 354564). The main purpose of this message is to provide factual information and not to provide financial product advice. Moreover, the information provided is not intended to give a recommendation or opinion about a financial product. However, each comments and opinion of opinion can only contain general advice that has been drawn up without taking into account your personal objectives, financial circumstances or needs. Therefore, before acting on the basis of one of the information provided, you must consider the suitability in the light of your personal objectives, financial circumstances and needs and you must consider requesting independent advice from a financial adviser if necessary before you make decisions. This message excludes specific personal advice.

#Cracks #foundation #growing #home #crisis #Australia