We talk about what happened, why it happened, discuss the impact on client portfolios and share some graphs and data from our research team.

Our research team — Sean And Mat – did such a great job this quarter that I decided to share some of the charts.

Let’s see.

The bull market continued for another year, but so did the fundamentals:

The market is becoming increasingly concentrated. Companies are getting bigger and bigger. But that also applies to income. It was another good year for earnings growth, which nearly matched the S&P 500’s gains.

This is good news.

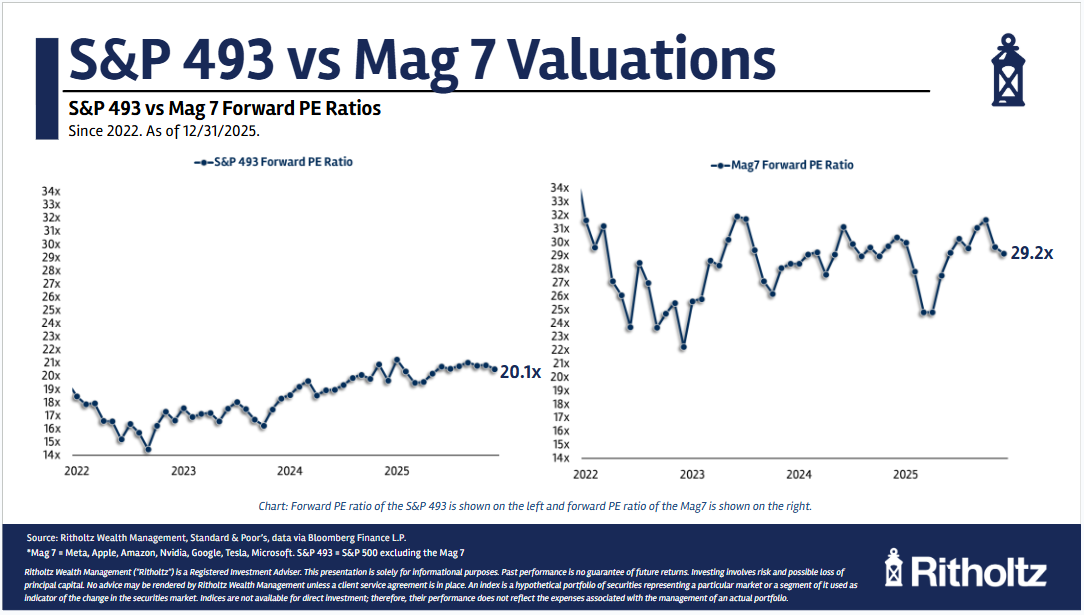

Speaking of fundamentals, take a look at the difference in price-to-earnings ratios between the Mag 7 and the rest of the S&P 500:

This is the hardest part of measuring the fundamentals of today’s stock market: Valuations are much higher for big tech stocks than for the rest of the market.

But these are also the largest and most profitable companies in history. They deserve a higher rating. So when does it become a concern?

It really depends on the embedded expectations and what happens to revenues from here. That sounds like a cop, but it’s the truth.

There is a much lower margin of safety with megacap technology than with anything else:

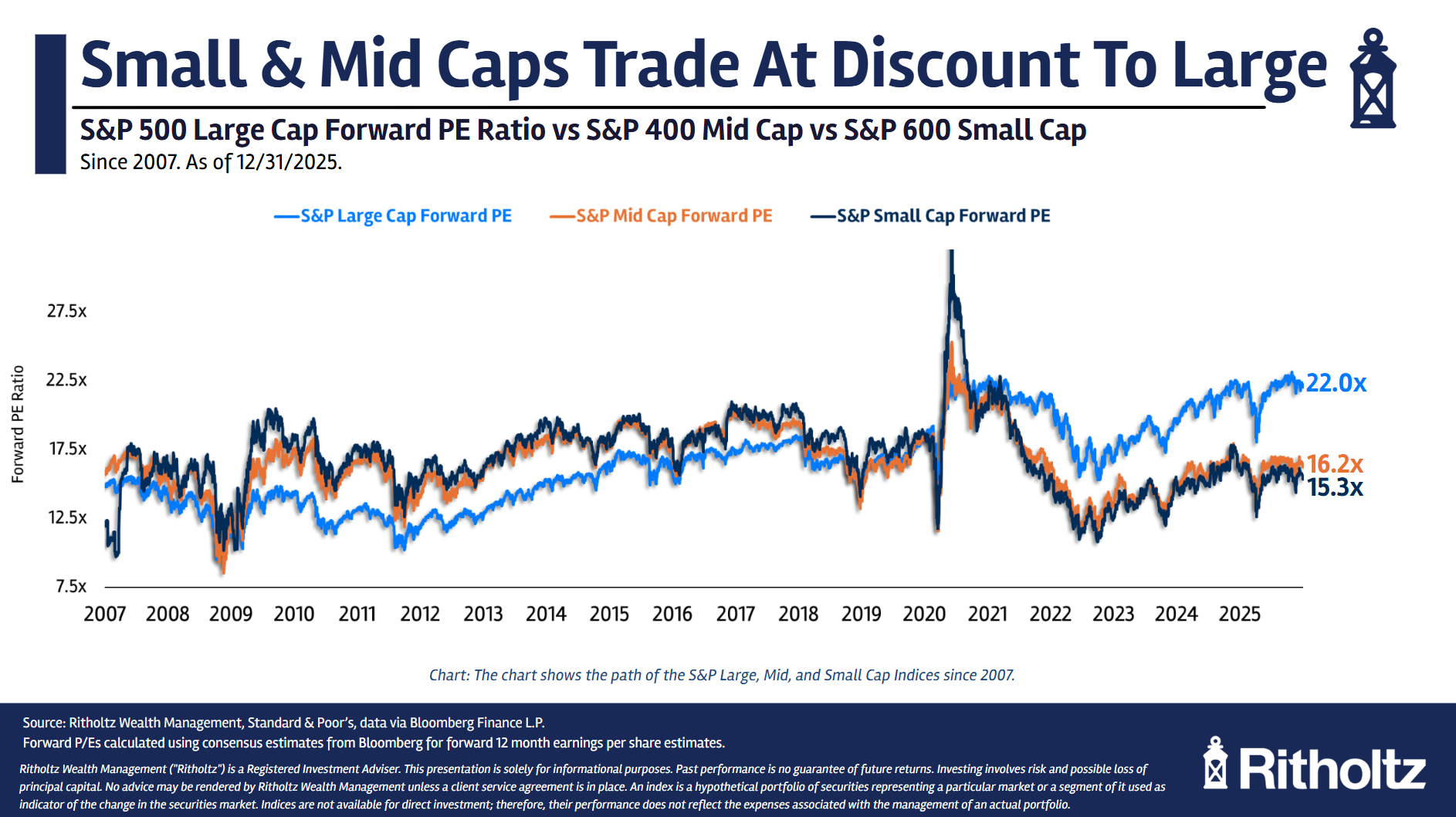

The biggest bull case for smaller stocks is the fact that valuations and therefore expectations are lower. It doesn’t take much good news for smaller companies to close this gap.

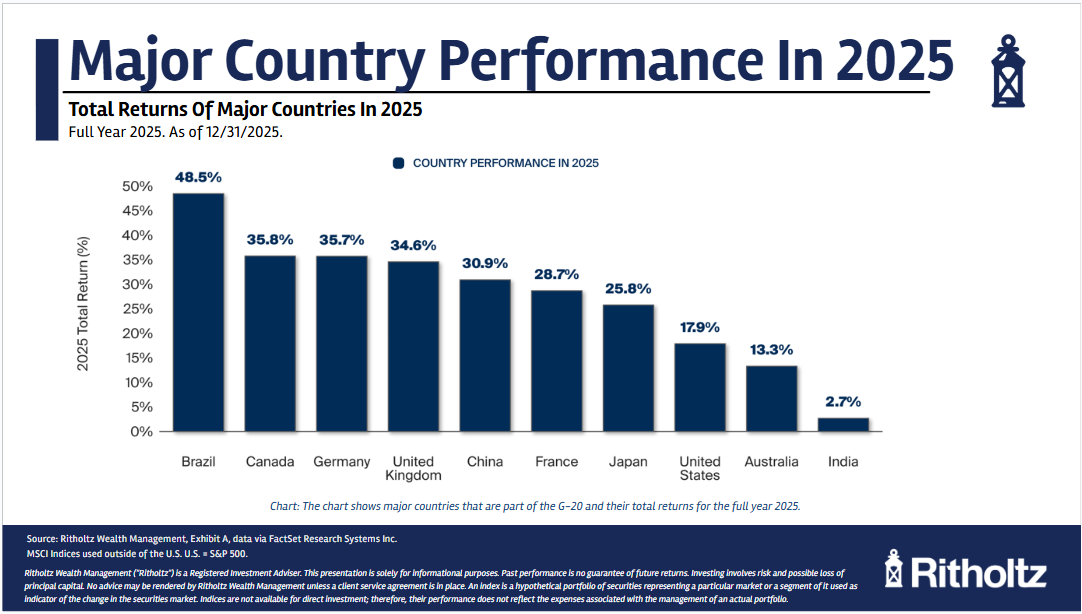

Perhaps small caps will become the international of 2025. The country’s performance figures last year were quite surprising:

The US stock market was near the bottom of the list. No one saw this coming last year.

Why did international stocks have such a good year? Here is the attribution broken down by fundamentals, currency movements and emotions:

The falling dollar was a tailwind for foreign stocks last year, but earnings growth was also good. Everything went well for foreign stocks last year.

Will it last? Don’t know.

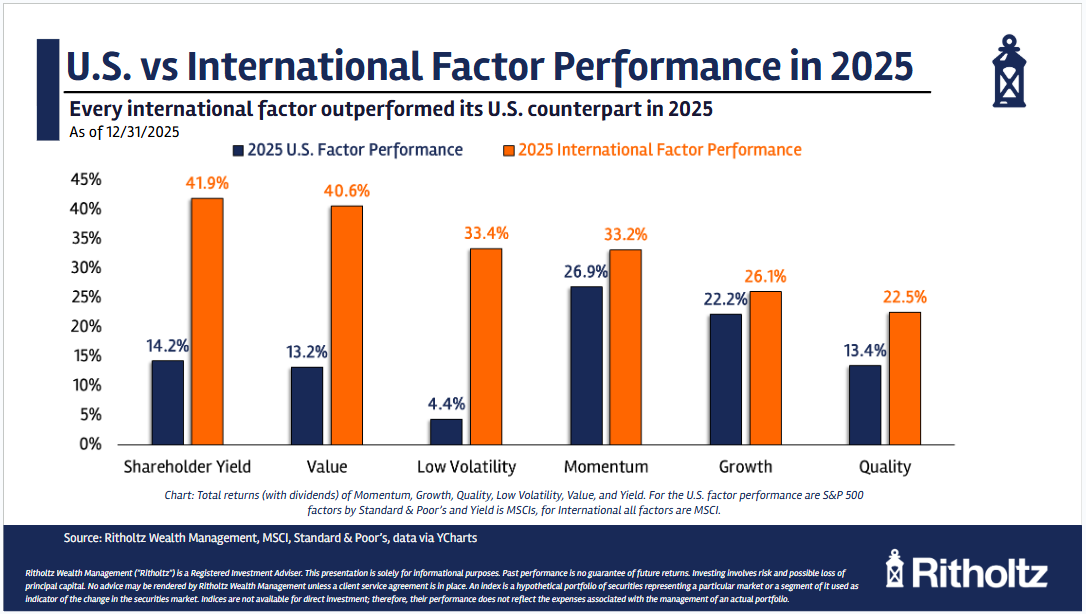

It is also interesting to look at the differences in factor performance between US and international markets:

Value stocks underperformed in US markets last year. But look at the value, shareholder returns, and low-volume stocks abroad: they’ve been crushed!

This is why diversification can be so maddening and eye-opening: you never know where the outperformance will come from.

Let’s end with the boring but necessary stuff.

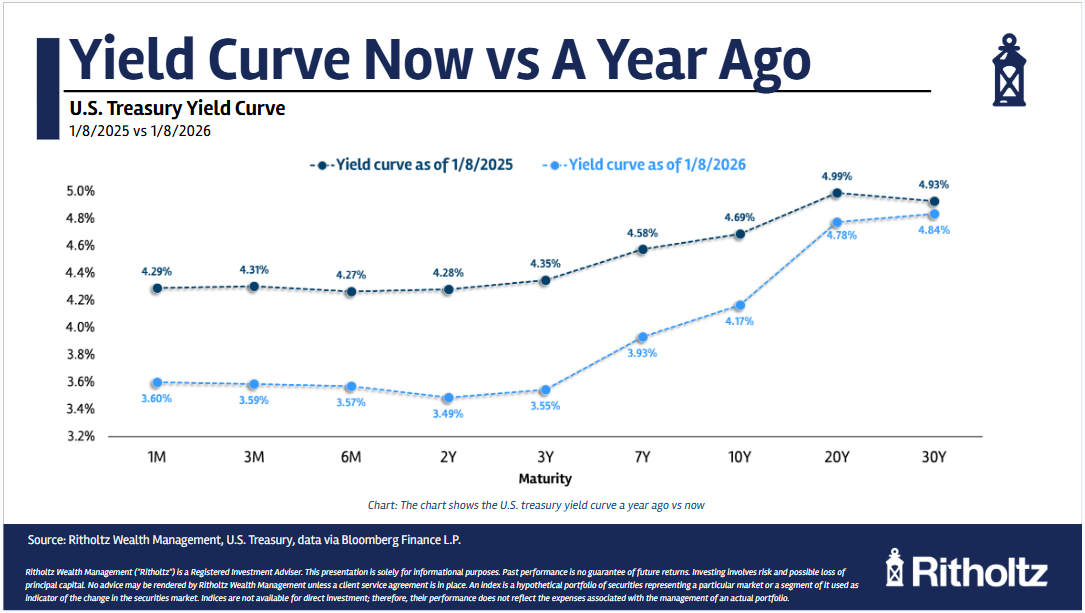

The bond market is healing:

In recent years, short-term returns have been higher or comparable to longer-term returns. That is not the normal state of the risk-reward relationship.

The yield curve is starting to look normal again.

It’s been a terrible decade for bonds, but yields are in a good place for fixed income investors right now.

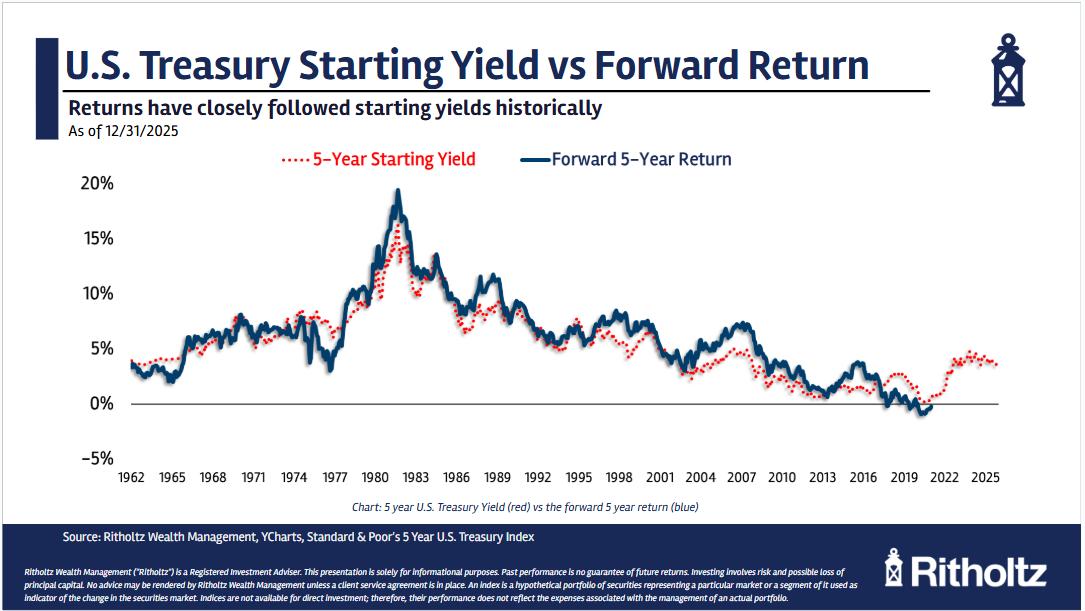

What does this mean?

Future returns for bond investors should be decent, as starting yields are the best predictor of future returns:

Bond yields are still pretty decent today.

The returns in the future should be the same.

If you would like to know more about what it is like to be a Ritholtz customer, please contact us here.

Further reading:

Historical returns for stocks, bonds, cash, housing and gold

The comments in this “post” (including any related blogs, podcasts, videos and social media) reflect the personal opinions, views and analyzes of the Ritholtz Wealth Management employees providing such comments and should not be construed as the views of Ritholtz Wealth Management LLC. or its respective subsidiaries or as a description of advisory services provided by Ritholtz Wealth Management or performance returns of a client of Ritholtz Wealth Management Investments.

References to any securities or digital assets, or performance data, are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. The charts and graphs contained herein are for informational purposes only and should not be relied upon in making any investment decision. Past performance is not an indication of future results. The content is only valid from the date indicated. Any projections, estimates, forecasts, objectives, prospects and/or opinions expressed in this material are subject to change without notice and may differ from or conflict with the opinions of others.

The Compound Media, Inc., a subsidiary of Ritholtz Wealth Management, receives payments from various entities for advertising in affiliated podcasts, blogs and emails. The inclusion of any such advertisements does not constitute or imply any endorsement, sponsorship or recommendation thereof, or any association therewith, by the Content Creator or by Ritholtz Wealth Management or any of its employees. Investing in securities involves the risk of loss. For additional advertising disclaimers see here: https://www.ritholtzwealth.com/advertising-disclaimers

See disclosures here.

#Charts #charts #charts #charts #charts #wealth #common #sense