Source: Testfolio.io

In the following paragraphs, I will discuss two ETF approaches that retail investors can access, highlighting Canadian-listed options where available. It’s worth noting up front that the Canadian market is much more limited than the US in this area, but you still have a few options.

And while these strategies can provide protection in specific scenarios, there is no free lunch. As you will see, the cost, complexity, and implementation challenges often make crash-hedging ETFs difficult to use effectively, even for experienced investors.

Option 1: Inverse ETFs

Inverse ETFs are designed as short-term trading instruments that aim to achieve the opposite return of a benchmark in a single trading day. Most track broad market indexes, although some focus on specific sectors or even individual stocks. The key point is that their objective is reset daily. They are not built to provide long lasting protection.

A well-known American example is the ProShares Short S&P 500 ETF (NYSEArca:SH). On each trading day, SH seeks a return equal to negative one times the daily price return of the S&P 500. If the index rises 1%, SH should fall approximately 1%. If the index falls 1%, SH should rise about 1%. In practice, it is quite successful in achieving that daily reverse exposure.

For investors looking for stronger downside protection, leveraged inverse ETFs are also available. These apply leverage to increase the inverse relationship. An example is Direxion Daily S&P 500 Bear 3X Stock (NYSEArca:SPXS)that targets a negative return of three times the daily return of the S&P 500. If the index falls 1% in a day, SPXS aims to rise about 3%. If the index rises 1%, SPXS should fall about 3%.

Canadian investors now have access to similar products. Instead of using US-listed ETFs, investors can look at options like the BetaPro -3x S&P 500 Daily Leveraged Bear Alternative ETF (TSX:SSPX).

Article continues below advertisement

X

During sharp sell-offs, these ETFs can do exactly what they were designed to do. During the COVID-related market panic of March 2020, when the S&P 500 plummeted, inverse ETFs like SH and leveraged versions like SPXS rose sharply, with leveraged funds seeing a much bigger move.

Source: Testfolio.io

As the chart above shows, the problem with these ETFs emerges once the panic subsides. As markets recovered after March 2020, both unlevered and leveraged inverse ETFs began to steadily decline. This highlights the core limitation of these products: you cannot buy and hold inverse ETFs if you accept that stock markets tend to rise over time. A permanent short position against the broad US stock market is structurally a losing bet. Therefore, issuers are careful to emphasize that these products are intended for day trading only.

That creates a new challenge. Using inverse ETFs effectively requires anticipating the crash and positioning just before it happens, then getting out before the recovery begins. That’s market timing, and it’s not just an active strategy; it requires being right twice. Even professional investors have to deal with this consistently, and retail investors tend to fare worse.

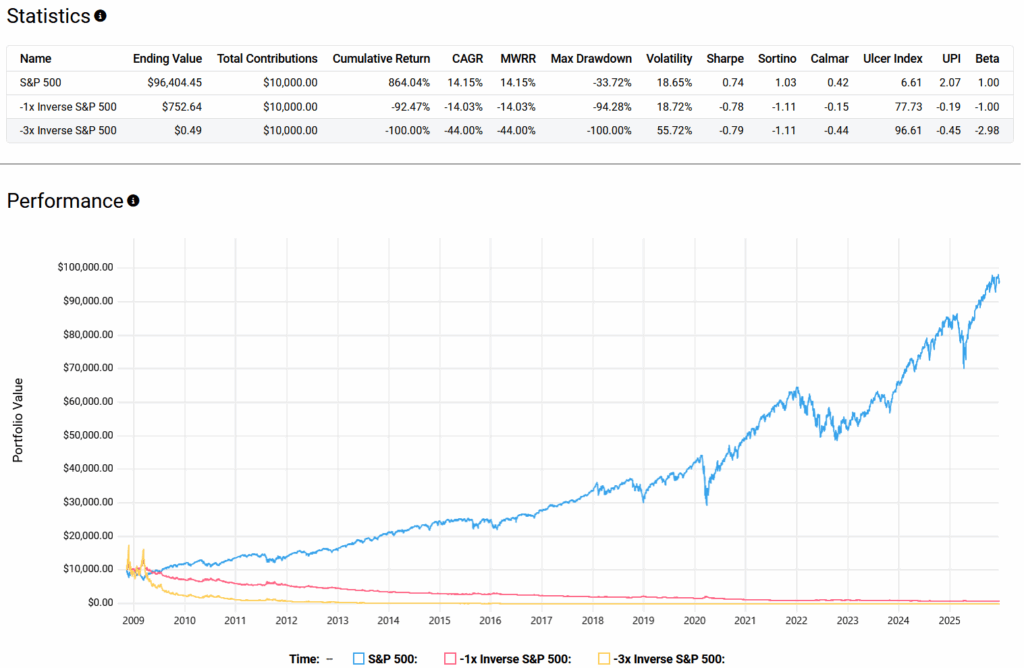

The long-term results reflect these headwinds. Over a period of roughly 17.1 years, from November 5, 2008 to December 18, 2025, a buy-and-hold investment in inverse ETFs like SH and SPXS would have essentially gone to zero after many reverse splits.

Source: Testfolio.io

That result is determined by various factors. First, the underlying benchmark generally shows an upward trend over long periods of time. Second, inverse ETFs come with relatively high fees, with expense ratios of 0.89% for SH and 1.02% for SPXS. Third, daily composition works against investors in volatile markets. When prices fluctuate up and down, the daily reset causes losses to increase faster than gains, curbing volatility.

In short, inverse ETFs can provide short-term protection during sudden market downturns, but using them as crash insurance requires precise timing. That makes them difficult to implement effectively and risky to keep them for more than a few days.

#hedge #market #crash #ETFs #Money #sense