White jacket")

One of the most important concepts for an investor to understand is that of expected returns. The expected returns are of course not guaranteed returns, but an investor who has no idea of the reach of possible future returns will probably make significant mistakes in investing.

A common mistake is to save too little. For example, an investor who expects that an investment will return 15% if it only returns 5% will save far too little to achieve their goals. Another common mistake is to buy high and sell low. This happens when an investor does not realize that a risky activa class can fall 40%, 50%or even more for a relatively short period. The investor panic and sells his investment to a more patient investor with a more realistic view of expected returns.

How to estimate the investment return

How estimate future returns? Probably the best place to start in the past is. If you expect an investment to return 20% per year, but the long -term return has only been 10% per year, you are probably disappointment. The general US stock market, the most successful in the world in the past century, has had A return in the past 100 years of 10.46%, approximately 6.51% in price rating and 3.95% in dividends. That number is prior to inflation, taxes and investment costs. Only inflation was 3.18% per year from 1925-2025, so the “real” (post-inflation) return was 7.28%. You can deduct taxes and expenses from there. You can quickly see that every consultant you suggest on “10% investment returns” to achieve your goals already enables you to fail.

Although that is common, some would make you believe that even higher returns are possible. Dave RamseyFor example, does fantastic work to help people get out of debts. Unfortunately, as soon as they have no debts, he has recommended that they will come in ‘good growth shares of investment funds’, which will then return them ‘12% per year’. About ten years ago there was a bust of a Ponzi schedule in my area where the investors were sucked in by promises of returns of 18% per year. If an investment promises three times the long -term efficiency of the stock market (which at some point lost 90% of its value), you can bet that it will be at least three times as risky.

Where do investment returns come from?

To make matters worse, many investment gurus people have warned people that the future expected return of the US stock market is much lower than the earlier return. To understand why, you must understand where the return comes from. John Bogle, in his investment classic Common sense of investment fundsTeaches that return comes from three components: the dividend yield, the profit growth of the underlying companies and the speculative return. In the long term, the speculative return will be a non-factor. Sometimes people are far too optimistic about the stock market, such as in 1999, and they offer shares for ridiculous prices. At other times, such as the end of 2008, people are far too pessimistic and sell shares with a discount. But in the long term, these excesses cancel each other.

So, long -term returns really only come from the dividend yield and the growth of income. Remember that from 1925-2025 about 40% of the return came from dividends (3.95%). Consider now the current dividend yield of the US stock market, 1.2%. Based on the profit growth of the companies that form the US stock market, in the future will remain about the same as in the past, long -term returns in the future seem to be about 2.8% lower than in the past. Is that assumption reasonable?

Well, US economic predictions for the coming years require a growth of 1.5% -2.7% per year. Fortunately that is a post-inflation number. If the current dividend yield is 1.2% and the expected growth is 2.5%, a fairly long -term expects to real return on the total US stock market in the future would be 3.7%.

In the meantime, the current yield of the American bond market is 3.8%. Unfortunately, that is a nominal pre-inflation number. If you deduct an expected 2.4% for inflation, you are lagging a real return of 1.4%. So a portfolio that partly consists of shares and partly of bonds probably has an even lower return than the aforementioned 3.7%.

More information here:

Some surprising things I learned to invest in 20 years

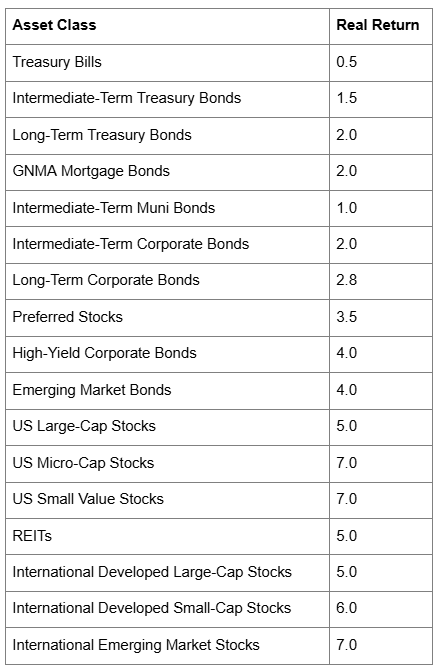

Expect return on investment per activa class

What should an investor do? There are actually only a few choices. First you can save more and longer. This is probably the safest of the options. As discussed on the future value function, we see that if you lower the return, you must increase the amount that is added to the portfolio each year or the number of years that the portfolio must worsen if you want to get to the same place. Secondly, you can take more investment risk. There are riskier asset classes than the total US stock market. In general with investing brings a higher risk the possibility of a higher return. Active classes such as small shares, value shares and the emerging market shares have a higher expected return than the total market.

Rick Ferri, in his excellent book, Everything about ActiveSpreading (2006), provides an overview of the following expected returns for different activa classes:

Although many would bicker about the actual values in this graph and the wisdom to invest in many of the aforementioned asset classes, the point is clear. If you have a portfolio with a large number of small shares, value shares and riskier international shares, your expected return (and the risk of temporary and permanent loss) is higher than that of someone who only has an American total stock market fund. Also, the lower the percentage of bonds that you own in the portfolio, the higher the expected return.

Of course, a portfolio that consists entirely of emerging market shares brings its own problems, and it is not recommended. Finally, an investor can hope that “Alpha” can be added to their returns. This is the extra return that is possible from superior security selection and market timing. The number can be positive or negative, depending on the skill of the manager, and for all investors as a whole it is zero before costs (and far below zero afterwards). Unfortunately, the data shows that this skill is quite rare and that it probably should not be calculated in order to add back to returns.

More information here:

Best investment portfolios – 150 portfolios better than yours

The 1 portfolio better than yours

The Bottom Line

For many of you, the expected returns that I have discussed above seem fairly low. I know how disappointing that can be. But Hope is not really an investment strategy. In view of how low future expected returns could be, it is the more important that the wise investor reduces the bite of taxes and investment costs on the portfolio pay.

The Bottom Line? Have a realistic view of what you can expect from investing in the long term. If you don’t, your investment plan will probably lead to failure because of your own behavior. Although 2023 and 2024 have returned more than 20%of the stock market, you must bear in mind that when estimating the future return for your portfolio, after inflation, after taxes, returns after the spending that are realistically, as 2%-6%.

How do you expect the stock market to perform in the coming years? Are you more optimistic than the figures in this post show? How will it influence your investment plan?

[This updated post was originally published in 2011.]

#Average #Investment #return #ROI #White #jacket