Are small-cap shares ready for a comeback?

The Equity Bull Market has been difficult for shares of small companies and their investors. The current decade started with promise. After the short, Sharp Pandemic Bear Market in 2020, Small Cap shares surpassed the technically driven S&P 500 index considerably during the post-Pandemic Bull Market that ended in December 2021. This was partly because the artificial intelligence (AI) needed the Momenters and Euphoria did not need the Media-Retaking and the Euphoria Media stories that were produced.

But that was the last time that small CAP shares defeated large caps in terms of capital valuation.

However, Small-Cap shares in the US now seem to be one of the more intriguing opportunities in the current market. Small Caps are often overshadowed by their larger counterparts-especially in this AI-driven Boom-but smaller companies look like they are undervalued, undervalued and ready for potential outperformance.

I mention fascinating valuations and improving market dynamics as only two of the reasons for small caps to at least exceed relatively.

A appreciation Sweet Spot?

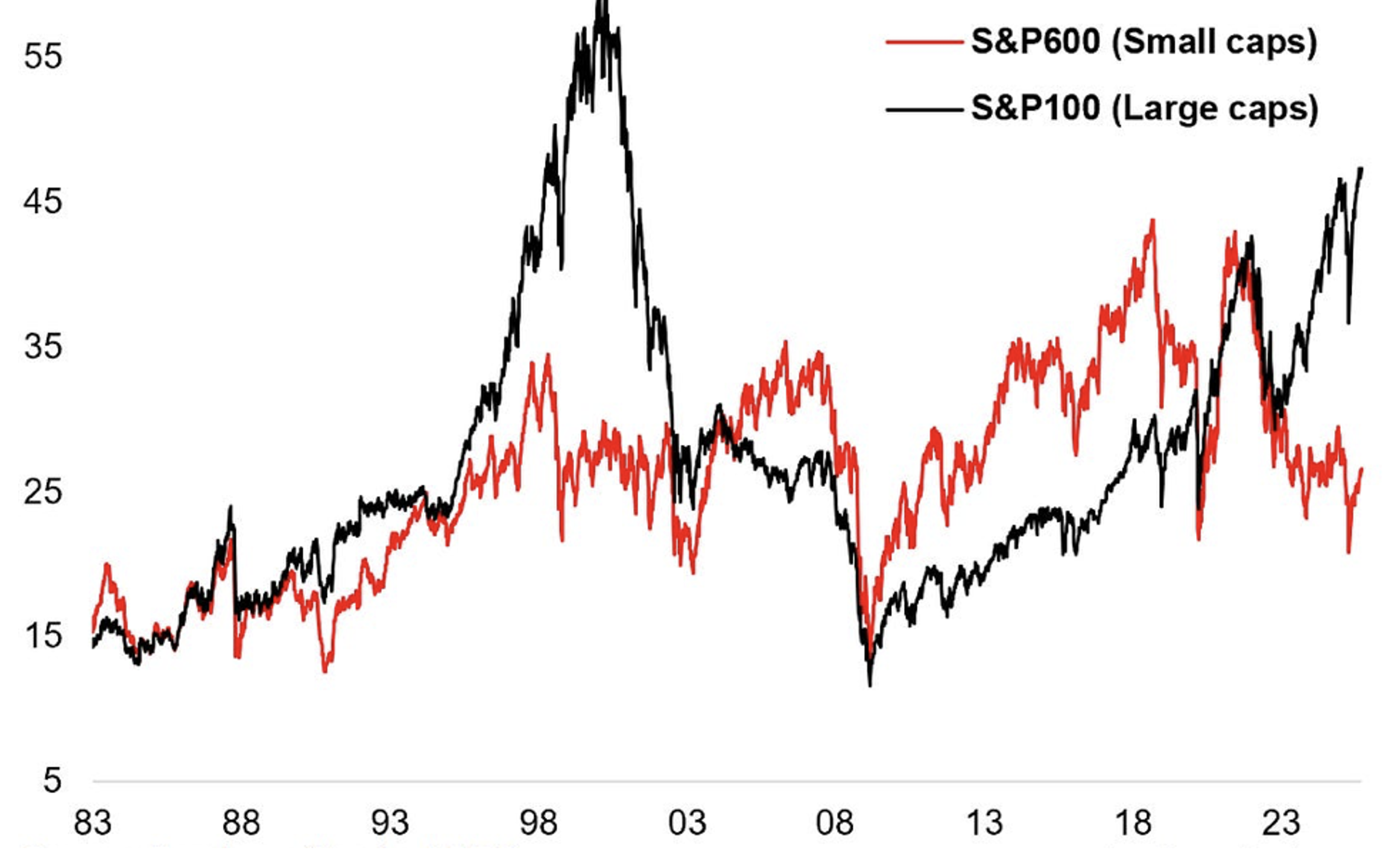

Figure 1. PE Small Caps versus large caps (Average income of the price/10 years)

Source: London Stock Exchange Group, Topdown Carts

Source: London Stock Exchange Group, Topdown Carts

In comparison with large caps, small companies have been acting with a considerable discount for a long time, with price -win (PE) ratios that are reminiscent of the lows during the Covid Market Trog. Small caps also look relatively cheap compared to their historical averages in the long term. And compared to bonds, American small caps still offer a risk premium for healthy shares, making them a relatively compelling choice for value -conscious investors.

Sentiment: A Contrarian’s Dream

Investor sentiment against small caps has been cold, but that is precisely why they are worth investigating.

This year, Small-Cap stock funds have seen enormous outflows, with allocations that affect historic lows. In the meantime, Futures markets show nearly record short positioning, making it a theater for a potential short squeeze as sentiment shifts.

Remembering the adage to ‘be greedy if others are anxious’, it may be that there is sufficiently relatively negative sentiment (or just too much enthusiasm for megapaps) that the stage is set for small caps to perform better.

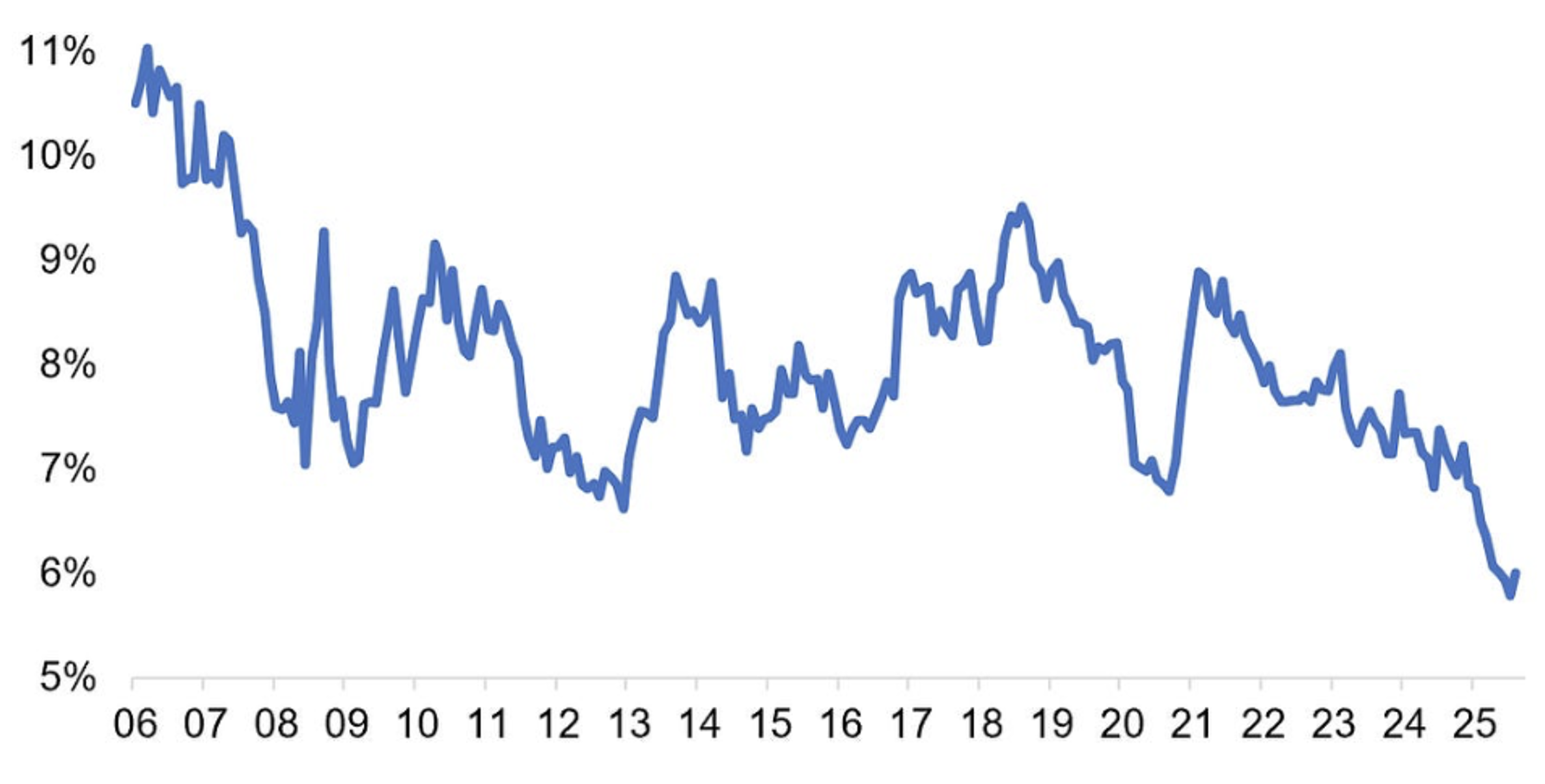

Figure 2. ETF market share: American small caps

Source: London Stock Exchange Group, Investment Company Institute, TopDown Carts

Source: London Stock Exchange Group, Investment Company Institute, TopDown Carts

Figure 2., shows assets in control in small CAP exchange-built funds (ETFs) as a percentage of all American ETFs for domestic shares. Although the low level is a function, not only of flows in ETFs with large caps, but also of the price performance of large CAPS conducted by Nvidia and his colleagues figure 2., that small caps will nevertheless be ignored relatively.

One reason could be that in a world of winner-all monopolistic mega haps, it is unlikely that small companies will win in business. However, this thinking is overlooking the potential pace of profit growth for individual small companies that expand from a small basis. And when it comes to large caps, let’s not forget the law of large numbers; Mega caps cannot continue to grow with double digits for an indefinite period of time, otherwise they become … well … the earth.

And here is another observation: sentiment starts to thaw. Recent data show a slight increase in ETF tutings in small caps. When a power class falls out of favor for a longer period and then starts to see renewed interest, it can be a trend change and in this case a shift in sentiment to small companies (and perhaps away from megapaps).

Macro -tail wind on the horizon

The macro -economic environment also seems to be in accordance with small caps. Now that the Federal Reserve is ready to launch a new round of interest rates, small caps – often more sensitive to loan costs – can be ideal for taking advantage. Lower interest rates can facilitate financial pressure on some of these companies, many of which depend on debts to stimulate growth.

Interestingly, small caps can also thrive in a scenario where global growth is picking up. In contrast to indices with large caps, which are strongly weighed in the direction of technology, small CAP indices are also full of traditional cyclical sectors such as industries and consumer goods. These sectors usually perform better when economic growth accelerates.

Risks

Risk inherent in all investment cases and small caps are no exception. An American recession remains a threat. A deep decline can drag absolute return lower across the board, including small caps. Even in a bearish scenario, small caps can stand better than large caps. Why? Large caps, especially in technical and AI-driven sectors, struggle with stretched ratings, speculative foam and even possible irrational exuberance. In a market correction, the AI high flyers could fall faster, which may result in small caps that perform better than on a relative basis.

On the other hand, a short and shallow recession with aggressive speed reductions and fiscal stimulus can actually be a net positive for small caps, which stimulates their attraction further.

Small Cap shares are located at an intriguing bending point. They are cheap compared to history, large caps and bonds. They are under his own, with the investor sentiment that is just starting to shift. Macro -economic factors are coordinated and Winstrevisions seem to appear.

For investors who are willing to look beyond the hype of large CAP technology and AI, small caps offer a compelling mix of value and contrary attraction.

Roger Montgomery is the founder and chairman of Montgomery Investment Management. Roger has more than three decades of experience in fund management and related activities, including stock analysis, stock and derivative strategy, trade and effects. Prior to the establishment of Montgomery, Roger positions in Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also the author of the best -selling investment guide for the stock market, value. Aabel-Hoe to appreciate the best shares and buy them for less than they are worth.

Roger regularly appears on television and radio, and in the press, including ABC Radio and TV, the Australian and Ausbiz. View upcoming media performances.

This message was contributed by a representative of Montgomery Investment Management PTY Limited (AFL No. 354564). The main purpose of this message is to provide factual information and not to provide financial product advice. Moreover, the information provided is not intended to give a recommendation or opinion about a financial product. However, each comments and opinion of opinion can only contain general advice that has been drawn up without taking into account your personal objectives, financial circumstances or needs. Therefore, before acting on the basis of one of the information provided, you must consider the suitability in the light of your personal objectives, financial circumstances and needs and you must consider requesting independent advice from a financial adviser if necessary before you make decisions. This message excludes specific personal advice.

#smallcap #shares #ready #comeback