Now, here’s today’s article:

“C” wrote this week:

A friend (in Sweden of course!) recommended you and I became a fan 😉

The short version of the story is that I went to a delicious free dinner sponsored by a financial investment company that would like to convert my traditional IRA to Roth through a Fixed Indexed Annuity.

They would pay a 17% bonus on my ~$580k traditional IRA + SEP + 401k and then, over the course of 10 years, switch to Roth, keeping income low enough not to stimulate the IRMAA increase (if that becomes an issue at 63 – I’m currently 60)

As I understand it, my only risk is the opportunity cost of not maximizing market profits.

Thanks for any insights you can/will give!

C, hello! Reading what you’ve outlined, my radar detector quickly comes to life and I prepare for a loud, red alarm!

Let’s first define this matte tool: What is a fixed indexed annuity??

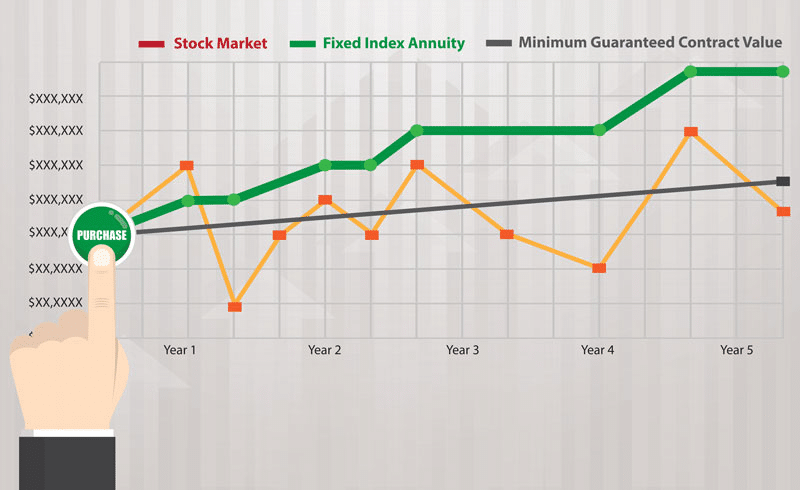

What is a fixed indexed annuity (FIA)?

A Fixed Indexed Annuity (FIA) is an insurance product that promises two things:

- Principal protection – your initial investment cannot lose value due to market declines.

- Some upside potential: Returns are linked to a market index (such as the S&P 500), but only partially.

This is how it usually works:

- The insurance company takes your premium and invests it conservatively (usually in bonds).

- They then use some of the interest earned to buy options on a market index.

- If the index rises, you get a share of the profit (via a ceiling or participation rate).

- If the index falls, you earn zero. But don’t lose money either.

It sounds nice. Not a downside, but an advantage. But I think there are MANY more reasons to hate FIAs.

1. High, opaque costs

The commissions paid to sellers are often 6 – 10% upfront, hidden from the investor. These costs are embedded in the product’s internal mechanisms, resulting in lower credit rates and slower growth for the customer.

For this FIA considering “C”, the principal amount of $580,000 would result in a commission of $30,000 – $60,000 to the seller. That alone should give us food for thought.

2. Complexity and confusion

The jargon behind annuities is complicated: cap rates, participation rates, spreads, reset periods and surrender charges.

The numbers and the way those numbers interact… usually more more complicated than the jargon! Each annuity uses its own verbiage in unique ways, combining confusing semantics with actuarial math.

It is almost impossible for a layman to fully understand what he is getting. Complexity hides costs and limits.

I’ve had to work with people who wanted to “unwind” these annuities. I despise how complex they are.

3. Limited benefit

The fact that an FIA is “market-linked” is a misleading promise.

If the market is growing at 15% and your FIA has a cap of 6%, you will only see that 6%.

They are sold as “market tied” to trick you into thinking you are really getting a shock from market growth. But over time, these products lag behind market growth by a significant margin.

4. Liquidity traps

Most FIAs will hold your money for seven to ten years. If you want to leave early, you risk heavy surrender fines. This inflexibility goes against sound, investor-oriented financial planning.

5. Misaligned stimuli

Annuities are often sold, not bought or advised.

Because of the large commissions, many non-fiduciary salespeople aggressively pitch them to safety-seeking retirees, sometimes exaggerating the returns or underestimating the downsides.

Quick side note…Mine free weekly newsletter helps busy professionals And retirees avoid costly mistakes and grow lasting wealth through retirement. Join over 3900 subscribers for free.

What about “Annuity + Roth Conversion?”

So looking at the FIA offering of “C” in particular, and the idea of using it as a vehicle for a Roth conversion….

I’m reaching my boiling point here…

Point 1: The “bonus” is not free money.

“C” was promised a 17% bonus. It sounds great. It’s the headline they use to hook people.

A real bonus of 17% would result in actual money in your account.

But this bonus is not cash in your account. It’s a contract value credit that only applies to income calculations after the ten-year period, not the actual bill you can walk away with.

The “17% bonus” is compensated by:

- Lower return limits (your ‘indexed’ growth potential is limited), and/or

- Longer redemption periods (more than 10 years is common), and/or

- Reduced liquidity (you cannot easily access your money without penalties).

The bonus is the marketing of sugar, not the actual juice.

Point 2: The “10-year Roth conversion plan” sounds smart, but it is structured in a way that benefits the annuity company, not You.

A gradual Roth conversion can be smart and spread tax payments over time to avoid jumping tax brackets or triggering IRMAA. But an FIA is not necessary for that.

You can keep your investments in a simple, low-cost IRA and still set the pace for Roth conversions each year.

What the company is really doing is locking down your money into their product. THAT’S WHY THEY PROPOSED THE 10-YEAR TIMELINE!

It’s a trap! Which…

- Pays the agent a very high commission, and

- Prevents you from easily changing course once you realize how limited the contract is.

Point 3: “Only risks are opportunity costs”…

“The only risk is opportunity cost…”

That’s the sales line. But it is misleading. Your real risks include:

- Liquidity risk: You cannot freely access your money.

- Complexity risk: You may not understand how the product (e.g. index credit) works until it’s too late.

- Return risk: FIA returns often lag simple portfolios (e.g. 60/40 indexing) by several percentage points per year.

- Inflation risk: Returns may not keep pace with rising costs of living.

Point 4: The Roth angle is a smokescreen.

The sales pitch uses “Roth conversions” to sound like they are doing careful tax planning. But the FIA company does not optimize your taxes. They sell a contract.

A real tax planner can help you make the same Roth conversions without all the extra costs or restrictions.

In short

You can absolutely follow a 10-year Roth conversion strategy. You just don’t need a fixed indexed annuity for this, and adding one often makes things worse, not better.

Annuities are sold. They are not bought.

For some people, that dinner you attended might have been the most expensive free dinner of their lives.

I know this sounds like scary fear mongering, and for that I apologize.

But it would be scarier if you said yes.

Thanks for reading! Here are three quick notes for you:

First – If you enjoyed this article, please join the thousands of subscribers who read Jesse’s free weekly email, where he sends you links to the smartest financial content I find online every week. 100% free, you can unsubscribe at any time.

Second – Jesse’s Podcast “Personal finance for long-term investors” has grown ~10x in recent years and now helps ~10,000 people per month. Tune in and check it out.

Last – Jesse works full time for a fiduciary asset management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free consultation with Jesse to see if you are a good fit for his practice.

We’ll talk to you soon!

#free #steak #dinner.. #interest