If you are like most investors, you ask the wrong questions.

I was chatting about ten years ago with a group of advisers in La Jolla and a question rice. I will paraphrase:

“Meb, thanks for the conversation. We get a steady stream of sellers and consultants here who have their different models for activity location at the port. To be honest it can be overwhelming. Some send us a report of 50 pages, all to explain a strategic shift from 50% shares to 40%.

The adviser followed by sending an e -mail to this summary of all institutional Asset -Allowance models By the Goldmans, Morgan Stanleys and Deutsche Banks of the World. And as you will see, they are very different. Morgan Stanley said only 25% in US shares, while Silvercrest said 54%! Brown Advisory said that 10% in emerging markets and JPMorgan 0%.

So what is a consultant to do? What is the most effective model for asset distribution?

It is actually, that is, that is the wrong question.

The right starting question is: “Are there any differences of assets allocations even matter?”

In the summary article that the advisor sent me, there is a link to one Data table that displays the assets assignments from 40 of the leading asset management groups in the country. I teased all the information from the table to investigate three allocations:

The allocation with the most amount in shares (Deutsche Bank at 74%).

The average of all 40.

The allocation with the least amount in shares (Northern Trust at 35%).

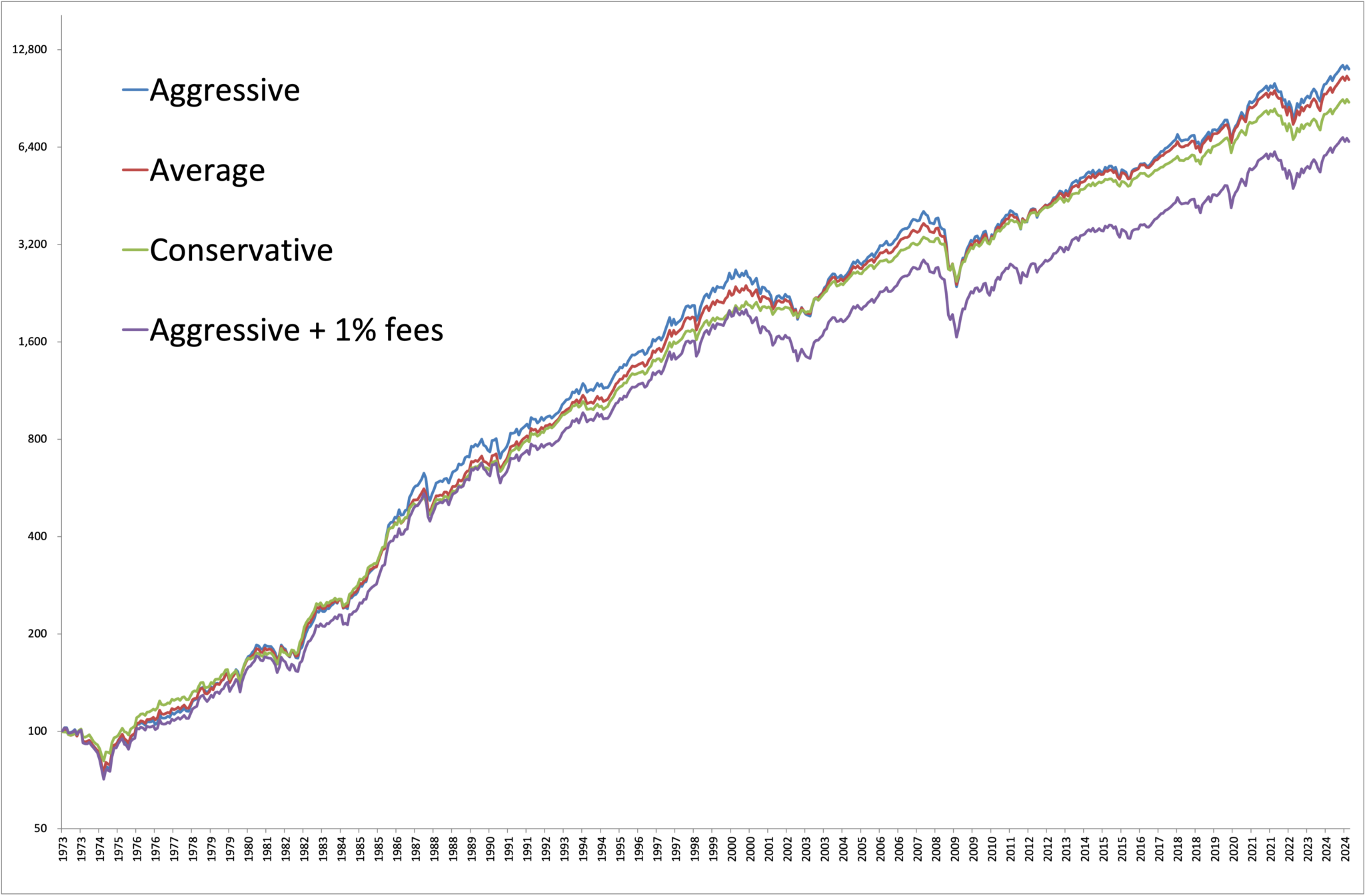

We used equal militas for private strategies on public market. Below is the stock curve for each. Unless you have a hawk -like vision, you will probably have a hard time distinguishing between the curves, and this is for the most different ones. The other 40+ companies live somewhere in the middle !!

Below are the returns for each allocation during the entire period of 1973-2024.

Most aggressive (DB): update of 9.48%

Average: 9.32%

Least aggressive (at): 8.98%

There you have it – the difference between the most and least aggressive portfolios is no less than 0.50% A year. How much do you think that all these settings will charge for their services? How many millions and billions in consultancy costs are wasted on ferrets of models for Activallocation?

Let’s try another experiment …

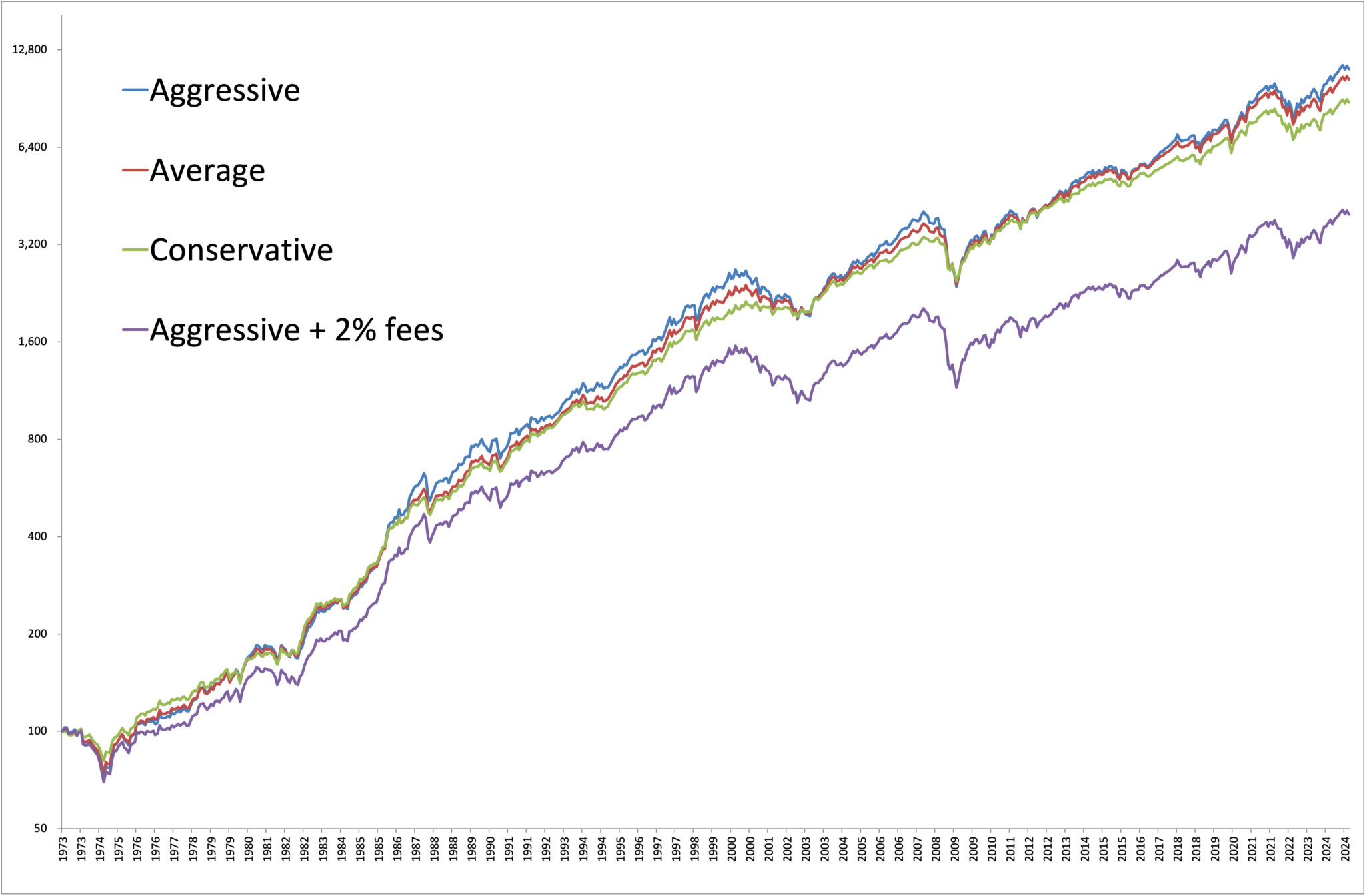

Overlay A simple 1% management costs on the most aggressive portfolio and look again at the return. Simply by paying this mild reimbursement (that is lower than the average investment fund, by the way), you have converted the highest recurring allocation into the lowest recurring allocation – which means that the full decision of the assets is completely irrelevant.

And if you assign to the average adviser with an average reimbursement (1%) that invests in the average investment fund, well, you know the conclusion.

So all those questions that emphasize …

“Is it a good time for gold?”

“What about the next Fed Move – do I have to illuminate my share positions in advance?”

“Are the UK going to leave the EU, and what should that mean for my allocation to foreign investments?”

Let them go.

If you had billions of dollars under management and access to the best investors in the world, you would think that you could beat a base 60/40 index. It appears that most settings cannot.

If you are a professional money manager, you spend your time on activities with added value, such as estate planning, insurance, tax harvest, prospecting, general time with your customers or family, or even golf.

#activa #spread #doesnt #matter #main #ingredients #matters #Meb #Faber #Research #Btall #Market #Investing #Blog