The 50/30/20 asset allocation rule provides better diversification, downside protection, and risk-adjusted returns than a traditional 60/40 portfolio.

By slightly reducing equity holdings, maintaining a solid base in fixed income and adding alternatives such as structured bonds, real estate or private credit, this strategy balances growth and defense.

The way you segment your portfolio can have a significant impact on returns, risk, and your ability to stay invested despite market fluctuations.

This article covers:

- What is the 50/30/20 investment strategy?

- Is the 50/30/20 rule actually good?

- What is a 60/40 portfolio?

- Is 60-40 investing still good?

Key Takeaways:

- A 50-30-20 portfolio balances growth and risk better than 60/40.

- Reducing bonds to 30% and adding alternatives increases risk-adjusted returns.

- 60/40 is weaker today because stocks and bonds often fall together.

- Alternatives are not automatically risky; they diversify and smooth portfolio fluctuations.

What is a 50/30/20 investment allocation?

The 50/30/20 asset allocation is a simple portfolio strategy that invests 50% in stocks, 30% in bonds and 20% in alternative assets to balance growth, stability and diversification.

50% shares

- Provides growth and capital growth.

- Should include a mix of domestic and international equities, large and small caps and, where possible, emerging markets.

- This segment drives the long-term return of the portfolio and benefits from compounding.

30% fixed income securities

- Provides income, stability and lower volatility.

- These can be government and corporate bonds, but also short and medium maturities.

- Reduces the impact of market downturns and helps smooth portfolio swings.

20% alternatives

- Diversifies risk away from traditional stocks and bonds.

- Examples include real estate (REITs), commodities, private credit, and hedge fund strategies.

- Alternatives help protect against inflation, provide income and can improve risk-adjusted returns.

Alternatives do not automatically entail high risk; the 20% allocation simply reflects their unique behavior, lower liquidity and diversification role.

Why is the 50/30/20 rule good?

The 50-30-20 asset allocation strategy gives you strong growth potential, built-in risk management and better diversification than a traditional 60/40 portfolio.

- Better diversification – The portfolio spreads the risk across multiple asset classes.

- Reduced volatility – Adding alternatives reduces sharp fluctuations in the value of the portfolio.

- Balanced growth and security – Shares stimulate growth, bonds provide stability, alternatives act as a buffer.

- Flexibility for different investors – Suitable for both people nearing retirement and long-term asset builders.

But these aren’t just intuitive benefits. Major institutions like BlackRock and JP Morgan Private Bank also support this shift, citing structural changes in the markets and macro risks.

50/30/20 budget versus investment rule

The 50/30/20 budget rule divides your monthly income into needs (50%), wants (30%), and savings or debt (20%).

The 50-30-20 rule of investing, on the other hand, divides your portfolio into low-risk assets (50%), medium-risk assets (30%), and high-risk assets (20%).

One determines how you spend. The other guides how to invest. They are not interchangeable, but work well together for disciplined financial planning.

What is a 60/40 asset allocation?

The 60/40 rule for investing follows a traditional model: 60% stocks, 40% bonds.

Historically based on the assumption that when stocks fall, bonds will rise – providing a natural hedge.

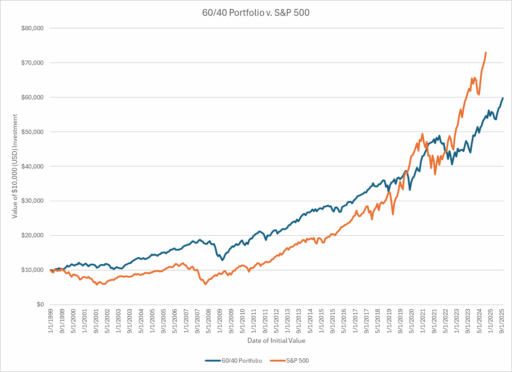

60/40 Portfolio vs. S&P 500

The 60% equity/40% bond allocation mix is designed to balance growth and stability.

Historically, it delivers solid long-term returns while reducing volatility compared to an all-equity portfolio.

The S&P 500, on the other hand, consists of 100% stocks. Historically it has delivered a portfolio of more than 60/40, but with higher volatility.

While it offers more upside potential during bull markets, it also exposes investors to bigger downsides during crashes.

But for long-term investors, even such crises are often weathered because continuing to invest gives time for recovery and deterioration to smooth out losses.

Why is a 60/40 portfolio no longer good enough?

The classic 60/40 model worked well for decades because stocks and bonds typically moved in opposite directions. But the current market environment has changed.

Here are the main reasons they highlight:

1. Stocks and bonds now coincide more often

Macro uncertainty, inflation and rapid interest rate changes have weakened the traditional hedge of stocks and bonds.

When both asset classes fall at the same time, the 40% bond portion no longer protects the portfolio.

2. Public markets are concentrated

A small group of mega-cap stocks drive most of the stock performance, reducing diversification within the 60% stock segment.

Meanwhile, much of today’s innovation (AI, deep tech, private infrastructure) takes place in private markets before companies list on stock exchanges, making alternatives essential for accessing early growth.

3. Private market activity and exits are increasing

JPMorgan notes that deal activity is improving, with more than 1,100 global IPOs and stronger returns in their US IPO index versus the S&P 500.

A healthier exit climate increases the attractiveness of private equity, private loans and venture capital.

4. Traditional bonds offer weaker protection

BlackRock emphasizes that long-term bonds no longer hedge portfolios as effectively due to inflation and fiscal pressures.

They encourage diversification into strategies that are less dependent on the direction of the market, such as long/short equity and multi-strategy hedge funds.

5. Alternatives increase returns and reduce volatility

Modern portfolio research, including insights from both JP and Blackrock, shows that adding alternatives can increase long-term returns, reduce volatility and improve Sharpe ratios compared to a regular 60/40.

Real assets, structured bonds, hedge funds, commodities and private credit offer return streams that behave differently from stocks and bonds.

60/40 versus 50/30/20: the end result

Compared to a 60/40, the 50/30/20 has historically performed better in periods of stress.

Backtests and institutional models show that portfolios with alternatives, such as a 50/30/20 split, have delivered better risk-adjusted returns in recent years.

The 50/30/20 strategy retains the growth potential with 50% in equities, but adds more downside protection and diversification by reducing exposure to bonds to 30% and introducing 20% in alternatives.

By tapping into multiple sources of return, investors build a portfolio that performs more consistently across different economic regimes.

It’s an attractive option if you’re concerned about risk and want a more modern, flexible portfolio.

Frequently asked questions

What is the rule of 72 in investing?

The Rule of 72 estimates how long it will take for an investment to double given a fixed annual return. Divide 72 by the interest rate (%) to get the estimated number of years.

What is Warren Buffett’s 70/30 rule?

A less formal guideline – sometimes attributed to him – of 70% in equities and 30% in short-term bonds, but it is not a central part of his well-known investment philosophy.

This strategy balances growth with stability.

What is Warren Buffett’s 90/10 rule?

The 90/10 rule is a more aggressive version: 90% in stocks (S&P 500) and 10% in bonds or cash, suitable for long-term investors with a higher risk tolerance.

What is Buffett’s golden investment rule?

Buffett’s golden rule is to never lose money and always understand what you are investing in. Focus on value, patience and long-term investments.

Tormented by financial indecision?

Adam is an internationally recognized financial author with over 830 million answer views on Quora, a best-selling book on Amazon, and a contributor to Forbes.

#asset #allocation #portfolio